Mortgage advice lenders don’t (usually) tell you

What You’ll Learn

Answers to the most common mortgage questions

What impacts the interest rates you’re offered, and how to choose the best rate for you

The refinance process and when refinancing will make sense for you

If you’re a first time homebuyer or experienced in buying, refinancing, and selling, you’re bound to have questions about the mortgage process, how it works, and most importantly what’s the best option for you right now. Which is not surprising given the real estate market is constantly changing and new lending products, innovations, and regulations are introduced on a regular basis.

Here we answer the most common questions for new home loans and refinancing. All of these questions are worthy of their own article, and in many cases, we link out to articles that really dig into each topic. Think of this as your jumping-off point for your next leg of the mortgage process.

Your top 15 mortgage questions, answered:

1. What’s the difference between a broker and a lender?

2. How long does it take to get a mortgage?

3. Do I have to do anything else to get pre-approved?

4. What documents do you need to get the mortgage approved?

5. How does your credit score affect your mortgage?

6. What mortgage advice would you give borrowers with poor credit, unstable employment history, or a small down payment?

7. What are closing costs?

8. What type of loan should I get?

9. How do I know what rate to choose?

9a. What rate/loan term would you recommend for me?

9b. How long is my rate locked in for? Can I cancel my rate lock if I change my mind?

10. My friend got this rate, why am I not getting the same rate?

11. Do I need an appraisal? If yes, what does the process look like?

12. What is escrow?

13. When are property taxes due?

14. How soon can I refinance my home after purchase?

14a. Does it make sense for me to refinance?

14b. Can I refinance after I just refinanced?

15. How much will it cost to refinance?

1. What’s the difference between a lender and a broker?

Lenders, like Better Mortgage for example, work directly with the borrower from application through funding of the mortgage. Working directly with the lender can make the loan process faster and more streamlined as it cuts out the middleman. Most lenders are paid through a variety of origination fees and charges which you can see on your Loan Estimate. Better Mortgage doesn’t charge lender fees and as an online lender, our site is available anytime, so you can get started whenever you’re ready.

Mortgage brokers do the shopping around for you and work with a variety of lenders to find loans for their clients. They’re paid on a fee-based schedule which is typically based on the total amount of the loan. Most brokers have a roster of lenders they prefer to work with so you’re unlikely to get access to all the loan types that are out there. If you have particularly unusual financial circumstances, they can save you time hunting for the specialized mortgage you may need.

2. How long does it take to get a mortgage?

It typically takes around 30 days to get a mortgage for a new home or to refinance an existing mortgage. When lots of people are looking to buy or refinance around the same time, it can take an average of 45–60 days depending on the lender. The average closing time with Better Mortgage is 10 days faster than the industry average.

A swift closing period relies on a number of factors, the two main ones being how quickly you can submit the required documents and the timing of third-party services such as appraisals and inspections. If the loan is more complicated—for example, if you’re refinancing and you have a second mortgage—it may take longer to close. In these circumstances, your loan officer will let you know when it’s time to lock your rate. Closing a mortgage is a team effort, so proactivity and communication is key.

3. Do I have to do anything else to get pre-approved?

If you speak to different lenders, you’ll soon notice there are some nuances in how they refer to the start of their mortgage approval process. Some lenders offer a pre-qualification, and others offer a pre-approval.

A pre-qualification can involve as little as a quick conversation with your lender about your income, assets, and down payment. A pre-approval can involve a soft credit check—which means the lender pulls your credit report to verify your credit score. In many cases, this is all you need to do to get pre-approved. However, it all depends on your unique situation.

4. What documents do you need to get the mortgage approved?

You may be surprised to learn that lenders need almost the same amount of documentation for a refinance as they do for a new home mortgage. That’s because when you’re refinancing, the home’s not new for you, but the mortgage is new for the lender.

To get a new mortgage or to refinance an existing mortgage, you’ll need to provide documents to verify your income and your assets. These can include paystubs, tax statements, tax returns, and bank statements. Your lender will do a hard credit pull to verify your credit score, any outstanding debts, payment history, and any derogatory credit events. At least 2 months of bank statements are needed to verify your current balances. Your lender may also need documentation for any large deposits or recurring payments to your account. If you’re planning to use funds from your retirement account, your lender will also need to confirm that you can withdraw from the account.

5. How does your credit score affect your mortgage?

Lenders look at your borrowing history to determine how likely you are to pay back your loans. A higher credit score suggests you’re better able to manage debt so lenders will be more comfortable offering you a loan for a larger amount. In this case lenders will be more likely to offer you a mortgage that will put you at a higher debt-to-income ratio (DTI). To calculate your DTI, lenders add your existing monthly debt payments to what your mortgage payments will be with the new loan, then divide it by your gross monthly income. Most lenders offer loans to creditworthy borrowers with DTIs below 43%. Better Mortgage offers loans to creditworthy borrowers with DTIs below 50%.

Your credit score can also impact the interest rate you’re charged for the loan, the amount lenders may need you to put toward the down payment, and for private mortgage insurance (PMI) if it’s required. Your down payment amount is important to lenders because it helps them understand how much risk they’ll be taking on with the mortgage.

Your credit score may also influence the amount you choose to put down on a home. If your down payment is less than 20% of the home’s purchase price you’ll be required to pay for private mortgage insurance (PMI). The lower your credit score, the higher the premium you’ll be charged for PMI.

6. What mortgage advice would you give borrowers with poor credit, unstable employment history, or a small down payment?

It’s always good to think like a lender if you’re worried your mortgage may not be approved. Learn the most common reasons a mortgage is denied and what you can do to address each issue. Improving your credit score and saving more money for a down payment can take some time, but government-backed loans (such as Federal Housing Administration loans) or adding a co-borrower may keep your mortgage plans right on track.

Stable employment will make it easier for you to make regular mortgage payments but this can sometimes be difficult to show when you’re self employed. There are a number of reasons why employment history can look unstable—some of them are simply due to the nature of the work. Two is the magic number when it comes to employment history: Lenders generally want to see documented income for a minimum of 2 years. This could mean submitting pay stubs if you’ve been with an employer, or at least within the same industry, for a minimum of 2 years. If you’re self-employed, this could mean submitting 2 years of tax returns plus additional business documentation. If the amount you earn doesn’t match the amount reflected on your tax returns, it could be an issue, so speak with a lender to see what you’ll need to qualify for the mortgage you want.

7. What are closing costs?

When you’re thinking about buying a home, it can feel like everything you read is about saving for the down payment—and given how long it can take many people to save, this isn’t surprising. However, it’s also wise to have a cash reserve set aside to cover closing costs. .

Closing costs are the fees and charges that need to be paid to successfully transfer ownership of home or refinance a mortgage. Some lender fees are avoidable, Better Mortgage doesn’t charge lender fees. Other charges include third-party fees (like notary fees), fees that you can shop around for (such as title costs), fees that can be waived in specific circumstances (appraisal fees for example), and taxes which can vary state by state.

If closing costs are something you hadn’t accounted for in your budget, it is possible to roll some or all of them into your mortgage. By “taking credits,” you accept a higher interest rate on your mortgage in exchange for the lender giving you a credit to offset your closing costs. Taking enough credits to offset all of your closing costs results in a “no-cost mortgage.” This is an option you can explore whether you’re purchasing a home or refinancing an existing mortgage.

8. What type of loan should I get?

Great question, and the type of loan that’s best for you really depends on your situation. The most common types of loans fall into 2 main categories: conventional mortgage loans and government-backed mortgage loans.

Conventional loans

| What it’s called | Its unique features | Is it right for you? |

|---|---|---|

| Fixed-rate mortgage | Consistent interest is charged for the full term of a fixed-rate loan. | It’s ideal if you want predictable monthly payments. |

| Adjustable-rate mortgage (ARMs) | Fixed interest rate for the first few years, then the interest rate adjusts based on market conditions. | It’s good if you only need the loan for a few years, but it may come with prepayment penalties which can make it difficult to refinance or sell the home. |

| Interest-only mortgage | Only interest needs to be paid for the first few years, then the monthly payments dramatically increase as you pay back the principal and remaining interest. | It can be useful if you have variable income. However, they’re difficult to qualify for and they lengthen the time it takes to pay back the loan. |

| Jumbo loan | Larger loans that exceed the dollar amount that Fannie Mae or Freddie Mac will buy or guarantee for mortgages in that location. | It may be necessary if you plan to purchase a home with a higher price tag or are refinancing a larger-balance mortgage. |

Government-backed loans

| What it’s called | Its unique features | Is it right for you? |

|---|---|---|

| FHA loan | Insured by the Federal Housing Administration (FHA), PMI may be mandatory for the life of the loan. | Yes, if you have less-than-ideal credit scores and savings. |

| USDA loan | Low-interest loan issued through the United States Department of Agriculture (USDA). | If you live in a rural area and meet the income requirements, this loan could be a great option. |

| VA loan | Loans for primary residences only, issued through the Department of Veterans Affairs. Most VA borrowers don’t need a down payment to secure financing and PMI is not required. | You can apply for these loans if you’re a U.S. veteran, eligible service member or the spouse of a service member who died in the line of duty, or have a service-related disability. |

Speak to a loan consultant to find out which type of loan would be best for your unique situation.

9. How do I know what rate to choose?

This is an extremely common question that comes with a couple of variants. Unless you work in the mortgage/lending industry, it’s only natural to want as much advice as you can before locking yourself into a mortgage. To answer this question and its variants, you’ll need to answer the following supplemental questions as well: How long do you think you’ll keep the loan? How much money will you have to use on closing costs? How much do you want your monthly payment to be? Do you want to pay a little more upfront to lower your monthly payment? Or do you want to roll your closing costs into the loan so you pay less upfront, but have a higher monthly payment?

If you’re buying your forever home and plan to keep the loan for a long time, it can be beneficial to pay for points. That means pre-paying some of the interest up front in return for lower monthly payments. If you know you’ll either sell or refinance in the next 5 years, choosing a rate with no points or taking a lender credit to cover some or all of your closing costs may save you money.

9a. What rate/loan term would you recommend for me?

The answer depends on your comfort level. When you’re pre-approved for a mortgage, it’s common that a lender will show you the maximum dollar amount they’d be prepared to offer you for a mortgage. Look at the monthly payments associated with that maximum dollar amount, then decide if you’re comfortable committing to that monthly payment amount.

In many cases, it’s better for you to choose a loan amount, rate, and loan term based on the monthly payments you’re comfortable making. After all, outside of your debts, the lender doesn’t know what your day-to-day living expenses are or if you have any big (and potentially costly) future plans. For example, if you’re planning to have children in the near future, you may be more comfortable choosing a lower monthly rate with a longer loan term.

Sometimes, people have an idea of how much they’re comfortable paying each month. If that’s you, then we’d recommend the rate/loan term that will help you achieve that goal. Everyone’s situation and future goals are different, so it’s always beneficial to talk through your options with a loan consultant to decide on the rate/loan term that’s best for you.

9b. How long is my rate locked in for? Can I cancel my rate lock if I change my mind?

If you’re buying a home, you typically lock your rate when the seller accepts your offer and you go under contract. If you’re refinancing, you’ll commonly be offered a rate lock when your loan is pre-approved. Usually, you can lock your rate for 45 days, but it could be 60 days if you’re refinancing with a second mortgage or a home equity line of credit (HELOC).

With Better Mortgage, you can cancel your rate lock and withdraw your application any time before your loan is funded, and there’s no fee for cancelling. However, if you choose to withdraw your application after the appraisal inspection, you will be responsible for the $550 appraisal fee. Once you’ve cancelled a rate lock and withdrawn an application, you’ll need to wait 30 days before locking another rate on the same property with us.

10. My friend got this rate, why am I not getting the same rate?

Each person’s financial situation is different—and so is each property. If you’re not being offered the same rate as someone you know, it’s likely because of differences in the type of property you’re purchasing and where it’s located—as well as your unique financial situation. Differences between your credit score and your friend’s can also come into play: People with good credit who want to borrow more money are often offered a lower interest rate by lenders. Lenders also take into account how likely and how soon borrowers are to refinance.

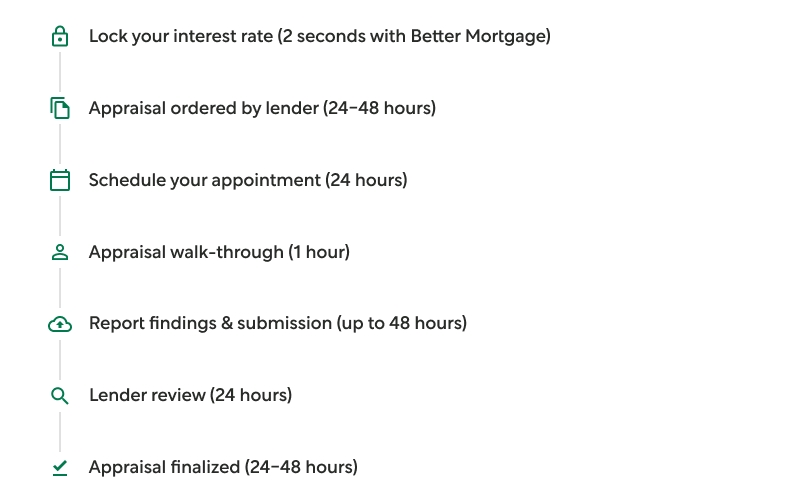

11. Do I need an appraisal? If yes, what does the process look like?

Whether you’re purchasing a home or refinancing an existing mortgage, your lender will typically order a home appraisal to make sure your loan amount doesn’t exceed the value of the home. If you’re refinancing, an appraisal is a great way to know if the value of your home has increased, especially since it will take into account any home improvements you’ve made.

Once you lock your interest rate, your lender will order an appraisal. Here’s the appraisal timeline at Better Mortgage:

In some cases, a home appraisal may be waived altogether. In these cases, lenders use existing data about the estimated value of a given property instead of relying on an appraisal report.

12. What is escrow?

Escrow accounts are financial accounts that are managed by a third party. They’re commonly used to hold the buyer’s deposit while their real estate transaction is being processed. Escrow accounts also hold money that’s collected as part of the monthly mortgage payment to cover property taxes and homeowners insurance. Your mortgage lender or servicer then uses money in escrow to ensure these bills are paid on time.

If you paid at least 20% down and you’re confident with budgeting, you can save a little money by choosing not to have an escrow account. For peace of mind, however, having an escrow account is an increasingly popular choice with borrowers.

13. When are property taxes due?

Property taxes are usually paid in advance, generally twice a year—on March 1 and September 1. Your lender can help you find out if the exact dates property taxes are due for your home.

When you’re buying a home, you’ll only be responsible for property taxes from the time you purchase the house. It’s likely that the previous owner has paid property taxes in advance that cover the time after you’ve closed on the home. In this case, you’ll reimburse the seller at closing for the prorated portion of the taxes they’ve already paid. This will be factored into your closing costs.

14. How soon can I refinance my home after purchase?

There’s no waiting period to refinance—unless you’re doing a cash out refinance, in which case you’ll have to wait 6 months. Your current lender might want to wait 6 months before refinancing, but there’s nothing stopping you from refinancing with another lender.

14a. Does it make sense for me to refinance?

It depends. There are a few reasons that could make refinancing worthwhile. Maybe your original loan has a high interest rate and interest rates have since dropped. You may need access to cash. Perhaps your credit score has improved or your income has increased. It could also be that the market changed, driving property values up. Keep in mind that you’ll have to pay closing costs with any new mortgage, so you’ll need to calculate your break-even point to determine how long until you start saving money. This refinance calculator will give you a good idea of whether refinancing is right for you and give you tips on how to maximize your total wealth.

14b. Can I refinance after I just refinanced?

Yes, if you have a conventional mortgage, and you’re not doing a cash out refinance, there’s no waiting period: You can refinance as many times as makes sense for you. That said, you should definitely weigh the pros and cons before committing yourself to another long term loan.

Some mortgages have prepayment penalties that you’ll be charged if you pay off your mortgage ahead of schedule. (When you refinance with another lender, the new lender pays off the old mortgage, which can trigger the prepayment penalty.)

A new refinance also means a hard credit check to verify your credit score. This can drop your credit score 5 to 10 points on average and may remain on your credit report for up to a year.

15. How much will it cost to refinance?

Every new mortgage comes with closing costs, which are usually around 2–5% of the loan balance. The easiest way to minimize upfront closing costs is by doing a no-cost refinance. There are 2 ways to do this: one way is to take lender credits to cover the closing costs in exchange for a higher interest rate, the other way is to roll the closing costs into the loan by borrowing a higher loan amount (which covers your closing costs).

If you choose to roll closing costs into the loan, you’ll likely receive a lower interest rate than if you took lender credits, but it will change your loan-to-value ratio (LTV). This is an important consideration because if your new loan amount is for more than 80% of your appraised home value, you may be required to pay private mortgage insurance (PMI), which will raise your monthly payment. When it comes to any refinance, you should always calculate your break-even point before you make any decisions.

Get tailored mortgage advice for your unique circumstances

Every person’s homeownership goals and financial situation are different, and to find out what’s best for you, it’s best to speak to a loan consultant. At Better Mortgage, you can get pre-approved for a loan in as little as 3 minutes—and our loan consultants are standing by ready to answer questions on your schedule.