What You’ll Learn

The difference between conforming and jumbo loans

Conforming loans vs. jumbo loans qualifying guidelines

How to determine if you’ll need a jumbo loan

Where there are million-dollar homes, there are buyers needing jumbo loans to finance them. If you’re looking to buy a home in San Francisco or Hawaii, there’s a good chance you’ll be offered a jumbo loan—even if the home you want isn’t jumbo-sized. You may still need a jumbo loan even if you’re not hoping to borrow a cool million. Whether you’ll need a jumbo loan or a conforming loan depends on the median price of homes in each county and the amount you need to borrow.

Understanding the difference between jumbo loans and conforming loans

When you boil it down, the key difference between jumbo loans and conforming loans is the dollar amount of the loan. There are set limits to the maximum amount you can borrow for a conforming loan in each county because the Federal Housing and Finance Agency (FHFA) uses conforming loan limits as a way to maintain the financial stability of the housing market. If a loan exceeds the conforming loan limit, the borrower will need a jumbo loan.

The lending guidelines for conforming loans are set by the Federal National Mortgage Association (Fannie Mae) and the Federal Home Loan Mortgage Corporation (Freddie Mac). These guidelines are designed to protect borrowers from predatory lending tactics by ensuring they aren’t biting off more than they can chew. While jumbo loans aren’t held to the same Fannie Mae and Freddie Mac guidelines, the specific eligibility requirements for jumbo loans tend to be more rigorous because these loans are for larger amounts.

What is a jumbo loan?

You already know the key trait of jumbo loans—that they’re for people who want to borrow more than the conforming loan limit—so let’s dig into what else makes them unique.

Jumbo loans aren’t held to the same eligibility guidelines as conforming loans because they’re not eligible to be purchased, guaranteed, or securitized by Fannie Mae or Freddie Mac (this is something that happens behind the scenes when you get a conforming loan). When a lender creates a jumbo loan for a borrower, the loan debt is either sold to investors or kept within the lender’s financial portfolio. However, the high dollar amounts we’re talking about with jumbo loans can make it more difficult to sell them as investments. When lenders have to keep a jumbo loan in their portfolio, the loan’s risk stays with the lender, and the lender may have to service the loan themselves—sometimes for the entire duration of the mortgage.

To offset this additional risk, lenders typically require more reassurance from borrowers that they will be able to pay back a jumbo loan. Simply put, this means jumbo loans come with stricter qualifying guidelines, like higher credit scores, larger down payments, more assets, and lower debt-to-income ratios, as well as higher interest rates.

What is a conforming loan?

Conforming loans are the most common type of mortgage loan in the country, probably due to the guidelines for conforming loans making them lower risk for everyone involved. We’ve already mentioned how the eligibility guidelines for these loans protect borrowers, but they also offer lenders more protections—which is great news if you’re a borrower.

You see, once you’ve used a conforming loan to buy or refinance a home, the loan debt is bought from your lender by Fannie Mae and Freddie Mac to provide liquidity to the mortgage market and make the mortgage market more affordable (and stable). Given that these government agencies purchase conforming loans, the eligibility guidelines are designed to reduce the risk of lenders approving loans for borrowers who, on paper, likely won’t be able to pay back their loans. Less risk for lenders typically means qualifying guidelines are easier for borrowers to meet. This means you can typically qualify for a conforming loan with a lower credit score, a lower down payment, and a higher debt-to-income ratio.

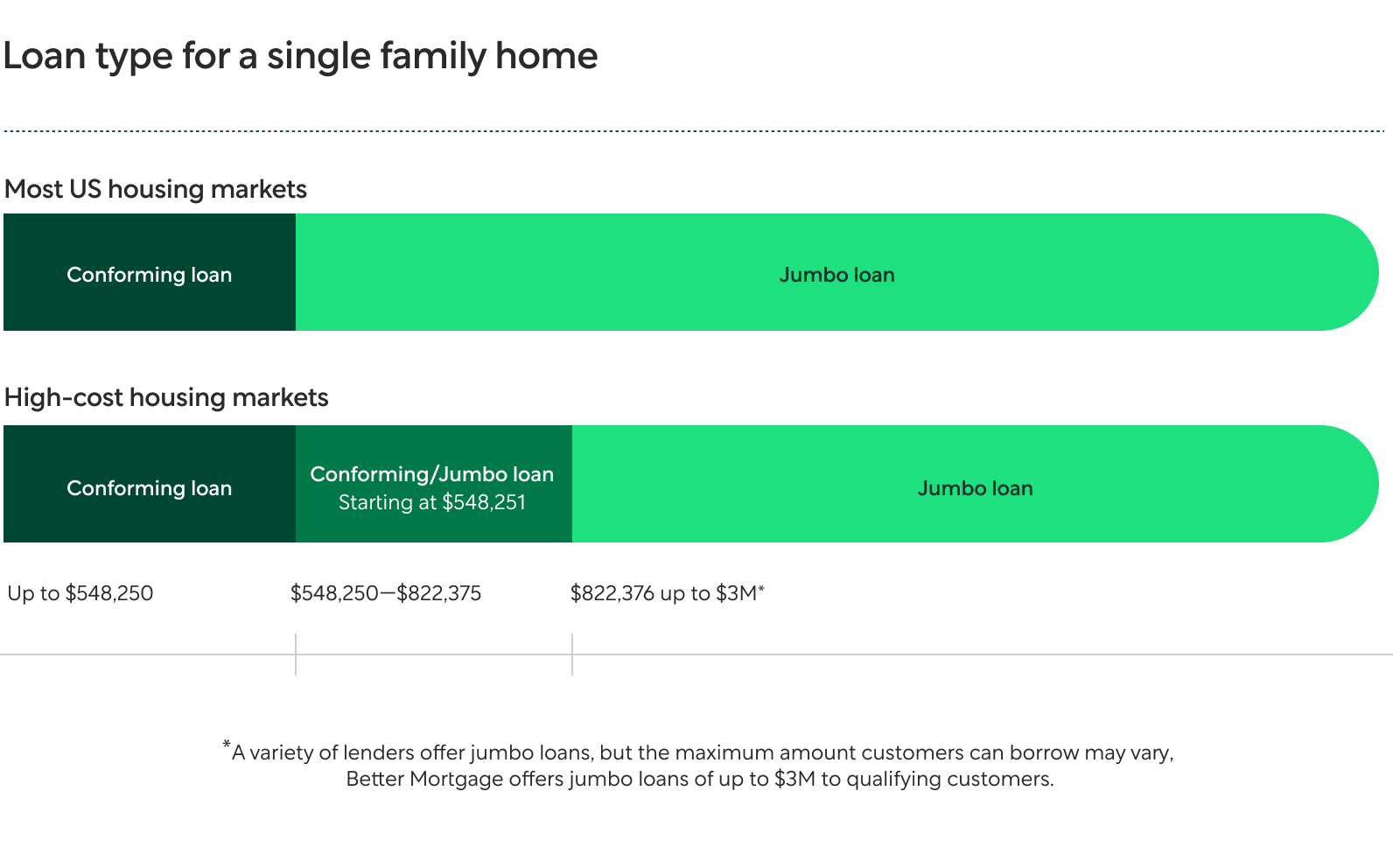

Conforming vs. jumbo loan limits

Most mortgage lenders prefer to work with conforming loans because they are highly liquid, easy to package and sell to investors, and quickly free up more cash to issue more loans.

As of January 2022, conforming loan amounts are capped at $647,200 for a single-unit home in most parts of the country. However, because the FHFA acknowledges prices can easily exceed this in higher-cost housing markets, like Hawaii, Washington D.C., San Francisco, or Los Angeles, maximum loan limits can reach as high as $822,375 in more expensive areas. But even in high-cost areas, it’s easy to exceed those limits, making jumbo loans a useful tool.

The Housing and Economic Recovery Act (HERA) requires an annual review of conforming loan limits to ensure they reflect changes in the average U.S. home price. Since 2008, according to the FHFA, various legislative acts have increased the loan limits in certain high-cost areas in the United States.

Qualifying guidelines for conforming and jumbo loans

Ultimately, it’s not the cost of the home; it’s the size of the loan you need that will determine whether you’re looking at a jumbo loan or a conforming loan.

If your home loan amount is less than the specified conforming loan limit for your county—then provided you meet the lending criteria—you would likely qualify for a conforming loan.

If your home loan exceeds the conforming loan limit, you will need a jumbo loan and must meet jumbo loan eligibility criteria. As jumbo lenders set their own underwriting guidelines, the eligibility criteria can vary from lender to lender.

Conforming vs. jumbo loan lending eligibility criteria:

| Conforming loans** | Jumbo loans** | |

|---|---|---|

| Credit score | ≥620 | >700 |

| Debt-to-income ratio | ≤50% | ≤43% |

| Down payment required | ≥5% of the purchase price | >20% of the purchase price |

**There may be some exceptions to these requirements for certain transactions. A Better Mortgage Loan Consultant can give more detailed information tailored to your unique financing needs.

Is a jumbo loan right for you?

If you’re a borrower with an excellent credit profile, significant money in savings, and a steady income, then qualifying for a jumbo loan could give you the flexibility you need to finance your dream home.

However, if you’re concerned about the qualification standards and higher interest rates of a jumbo loan, there are ways to stay within conforming loan limits.

How to stay within conforming loan limits for a purchase:

Stick to a budget: Make sure you know the conforming loan amount for your county. Then, determine the maximum purchase price that will keep you within that limit.

Increase your down payment: Conforming limits don’t apply to purchase price; rather it’s the amount financed that needs to be considered. If you’re on the cusp of jumbo loan requirements, consider increasing your down payment.

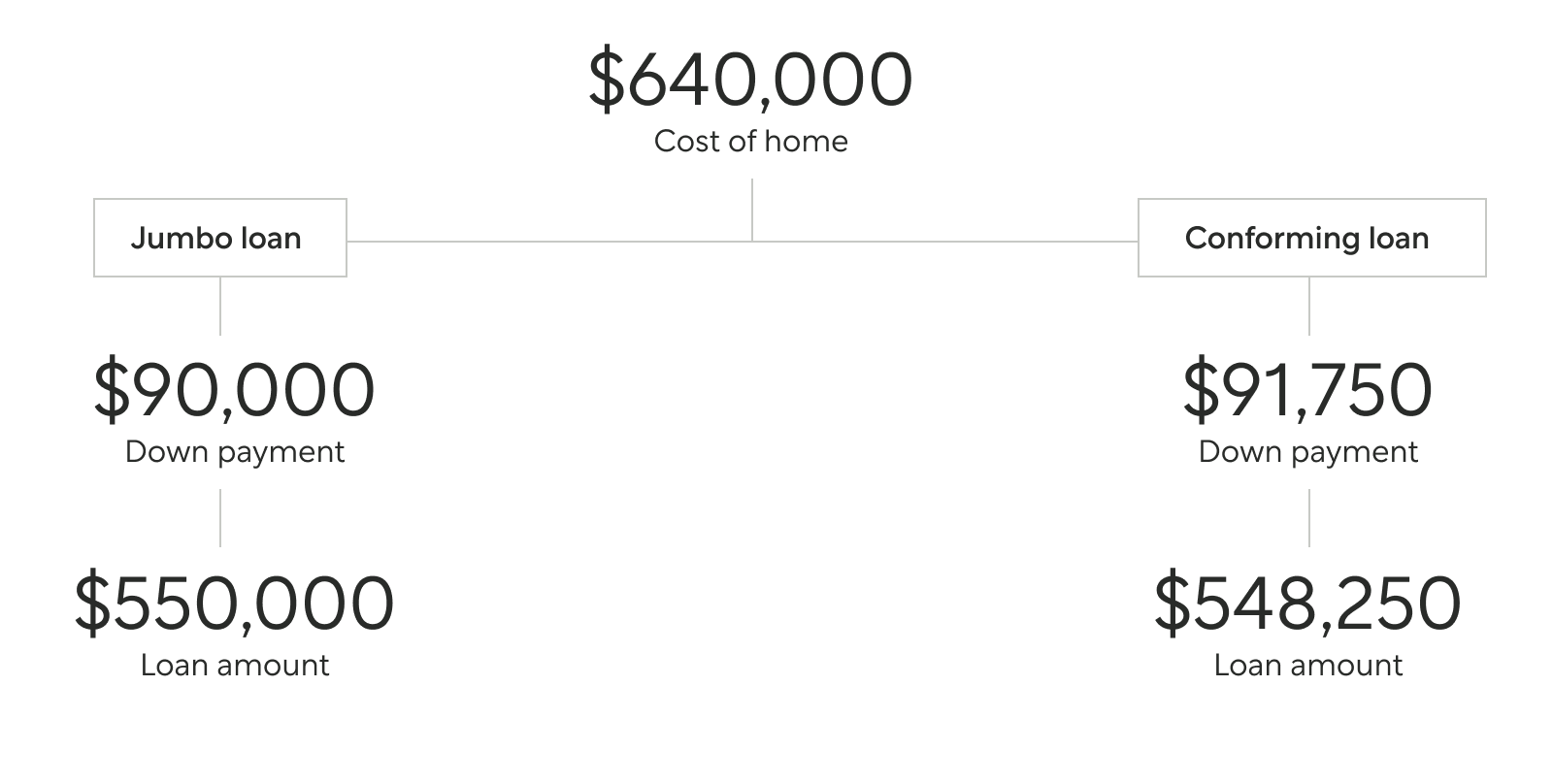

For example, if you buy a home that costs $640,000 in an area where $548,250 is the conforming loan limit, and you have a down payment of $90,000, adding just $1,750 to your down payment would bring your loan to $548,250, meeting the conforming loan limit.

How to stay within conforming loan limits for a refinance:

Wait until you’ve paid off enough of your balance: If your existing mortgage is a jumbo loan, you can refinance to a conventional mortgage once your loan balance drops below the conforming loan threshold. Note: if you plan to roll any closing costs into your loan or tap into home equity, this will add to your mortgage balance.

See what kind of loan you’ll need

Whether you’re buying in a county with a low conforming loan limit or a higher-cost area, Better Mortgage can help you get an accurate estimate of your homebuying potential. In as little as 3 minutes, you can get pre-approved with Better Mortgage and receive your free, no-commitment pre-approval letter. We’ll show you the types of loans and interest rates you qualify for so you can set your house-hunting budget.