Home Equity Line of Credit Payment Calculator

Use our HELOC Calculator, and quickly estimate monthly home equity payments and discover how all different factors can affect the loan payment for your new home.

Get between $50k-$500k from your home equity

Fund renovations, down payments, college funds, and even pay off high interest debt

Cash in hand in as little as 7 days¹

Get between $50k-$500k from your home equity

Fund renovations, down payments, college funds, and even pay off high interest debt

Cash in hand in as little as 7 days¹

What is a HELOC?

A home equity line of credit, commonly known as a HELOC, is a financial tool that allows homeowners to tap into the equity they have built in their property. It works as a revolving line of credit, similar to a credit card, where borrowers can access funds as needed.

In other words, it’s a type of loan that uses the difference between the market value of your home and the outstanding balance as collateral.

What can you use a HELOC for?

HELOCs can be used for various purposes, like funding home improvements, a down payment for a new home, education expenses, emergency expenses, or even debt consolidation – pretty much anything you want!

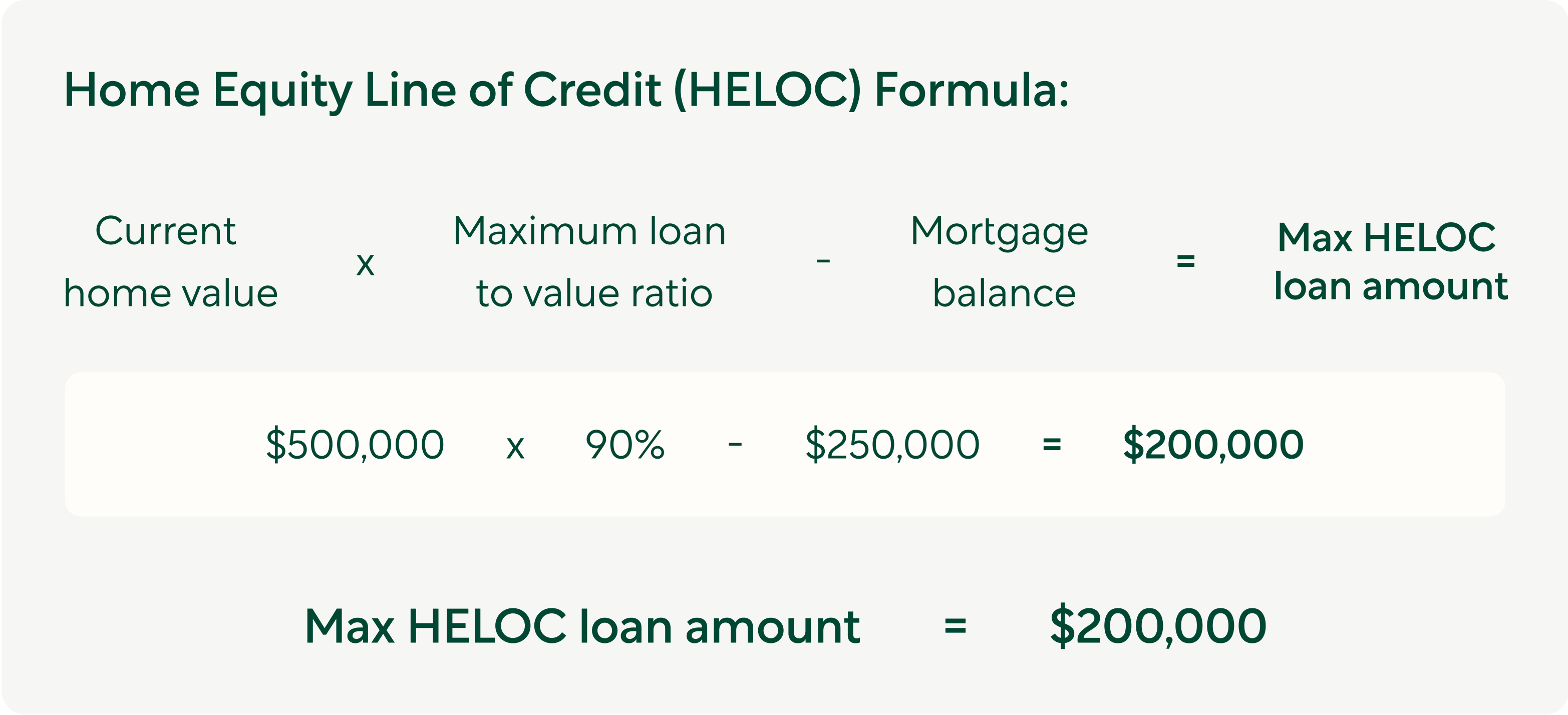

How much equity can I borrow from my home?

The maximum amount you’re allowed to borrow, also known as your loan amount, is determined by the equity in your home. Typically lenders will extend a line of credit that, when combined with the balance of your current mortgage, does not exceed 85-90% of your home’s value.

For example, if your home is worth $500,000 and you still owe $250,000 on your mortgage, then you may qualify for a HELOC up to $200,000.

How do HELOCs work?

Unlike a traditional loan, which provides a lump sum upfront, a HELOC allows borrowers to draw funds periodically during a predetermined draw period, usually 5 to 10 years. This draw period is often accompanied by a "credit line" or "checkbook" that enables homeowners to access funds whenever they need them.

During the draw period, homeowners can withdraw and repay money as needed, paying interest only on the amount utilized. This flexibility allows borrowers to manage their cash flow more effectively, as they only pay interest on the outstanding balance. For example, if you have a $50,000 HELOC but only use $40,000, you will only be charged interest on the $40,000.

Once the draw period ends, the line of credit is converted into a repayment period, typically around 20 years, where borrowers must start paying back the principal amount borrowed. During this repayment period, borrowers are required to make monthly payments that include both principal and interest.

When considering a HELOC, it's essential to assess your financial situation and determine if it aligns with your goals and needs. If you need help making an informed decision and understanding the potential risks and benefits associated with a home equity line of credit, reach out to us at hello@better.com, or call us at (415) 523 8837.

What are the Pros & Cons of a HELOC?

Pros of a HELOC

From its flexibility in borrowing to potential tax advantages, a HELOC can provide individuals with greater control over their finances and potential savings. One of the key advantages is flexibility – accessing the funds as needed – making it an ideal solution for home renovation, education expenses, or unexpected financial challenges. Also, because a HELOC is secured by your home, it generally comes at a lower interest rate than traditional loans or credit cards. Finally, you may be able to deduct the interest you pay on your HELOC annually on your tax return!

Cons of a HELOC

While a home equity line of credit offers homeowners financial flexibility, it’s important to consider potential drawbacks before deciding if it’s right for you. One thing to keep in mind is the variable interest rate associated with HELOCs which can lead to increased payment requirements over time. It’s also important to note that while you can use the cash for anything you’d like, using it for non-essential expenses may result in accumulating debt and jeopardizing your long term financial stability. Lastly, if property values decline, it could impact the available credit on your HELOC. So, before committing to a home equity line of credit, it’s important to carefully weigh out these considerations and assess whether the benefits align with your financial goals.

HELOC vs home equity loan

While both a HELOC and a home equity loan leverage the equity in your home, they are different in their structure and usage. A HELOC acts as a revolving line of credit – like a credit card – offering you the flexibility to borrow as needed. Its variable interest rate and draw period make it an ideal option for ongoing projects or unpredictable expenses. On the other hand, a home equity loan provides a lump sum with a fixed interest rate making it better suited for one-time expenses. That said, each option has pros and cons and the right choice depends on your individual financial goals and preferences.

HELOC vs refinance

While both avenues leverage home equity, they serve distinct purposes that will help dictate which one is right for you. In a nutshell, a HELOC operates as a flexible line of credit, allowing homeowners to borrow against their equity as needed, similar to a credit card. On the other hand, a mortgage refinance involves replacing the existing mortgage with a new one, often to secure a lower interest rate, change the loan term, or extract equity. In a nutshell, a HELOC offers flexibility for ongoing financial needs, whereas a refinance is a strategic move to improve overall mortgage terms.

Homeowners often weigh the option of a HELOC against a cash-out refinance – where you replace your current home loan with a larger one, pocketing the difference in cash to use for things like home improvements or paying off high-interest debt. While both are common ways to tap into your home equity, a HELOC is a second loan that lets you keep your existing mortgage, while a cash-out refinance replaces it with a new one. HELOCs often make sense for people who need cash, but have a low mortgage rate they want to keep.To see which option might be better for you, use Better’s HELOC vs Cash Out Refinance Calculator.

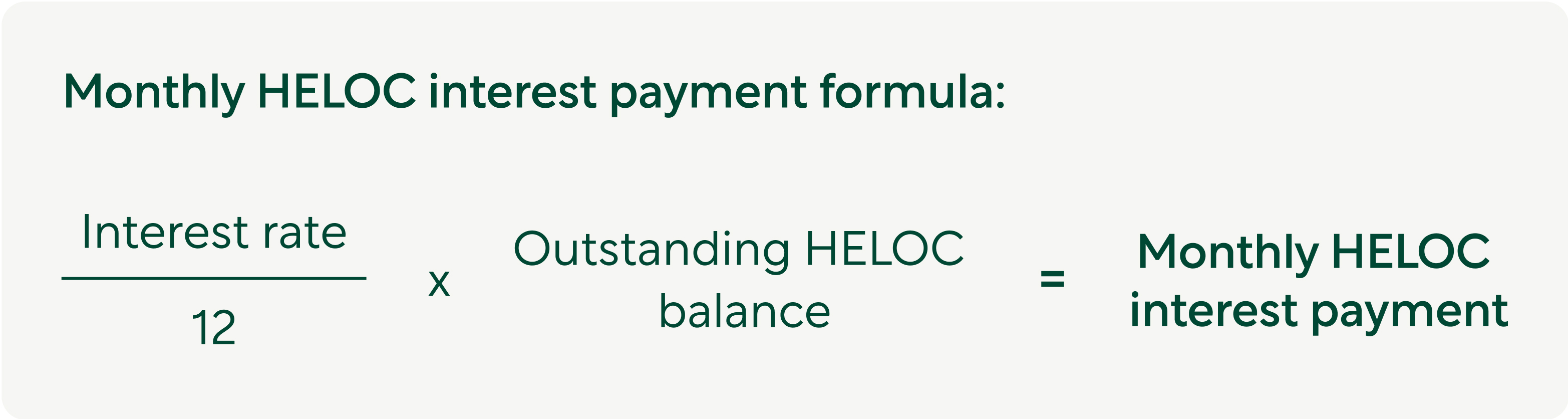

How are HELOC payments calculated

HELOC payments are calculated based on only the funds that you borrow. The lifetime of the loan is divided into when you can borrow, called the Draw Period and when you can’t borrow, called the Repayment Period.

During the draw period, which is the initial phase, you can borrow from your line of credit and are required to pay back only the interest on the amount used. The interest is calculated on the outstanding balance, not the total line amount, making monthly payments more manageable.

Once the draw period ends, the repayment period begins and you enter the phase where you can no longer borrow more funds. During this time you can enjoy the interest only payments for a short period, called the interest only period, - but after that period ends you will be required to repay both principal and interest for the remainder of the loan’s term.

It’s important to note that HELOCs often have variable interest rates, so payments can fluctuate.

To estimate your monthly payment, you can use a simple formula:

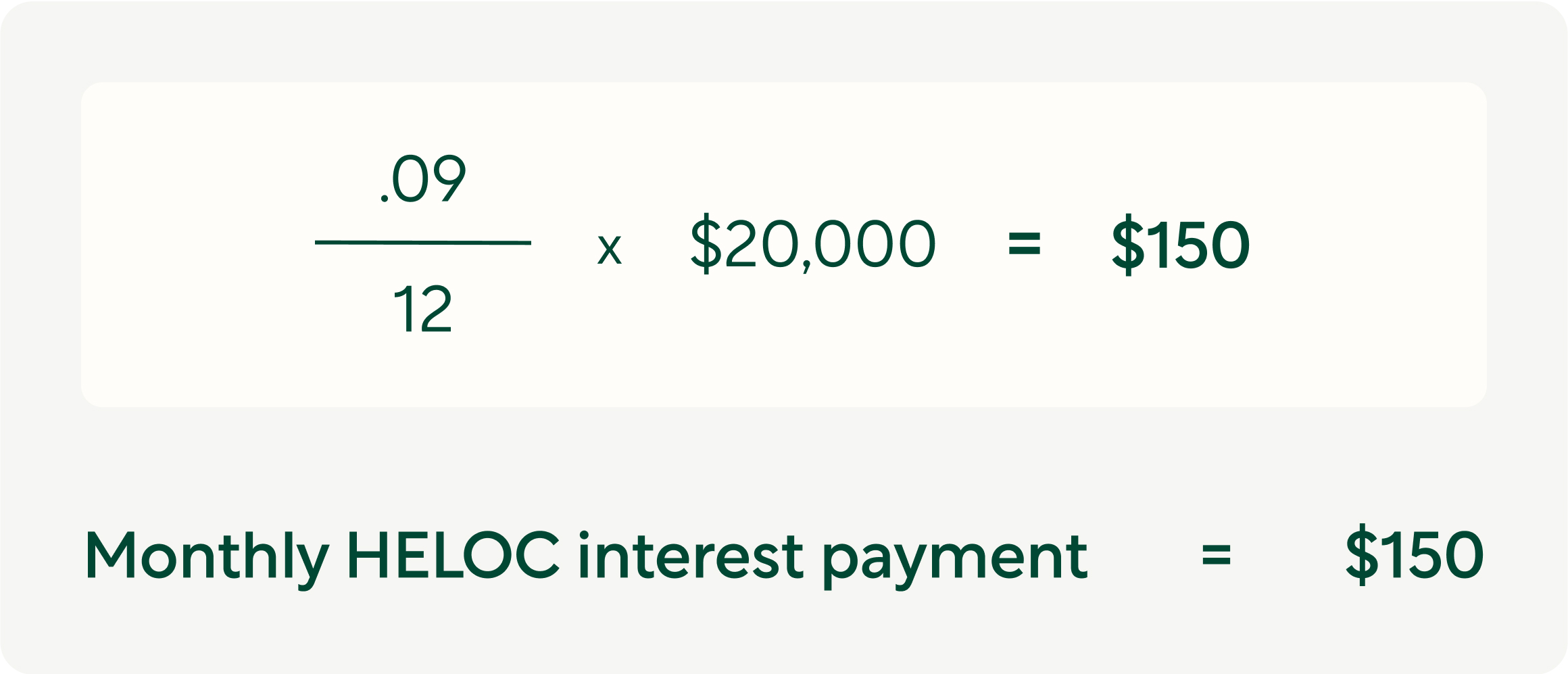

For example, if you owe $20,000 and the annual interest rate is 9%, the monthly interest payment would be:

Remember that month to month your balance and interest rate can change, so payments may not be predictable.

But, exploring the terms and details of your HELOC agreement is crucial for a clear understanding of your specific payment structure and any potential fluctuations.

Does a HELOC affect your credit score?

When you apply for a HELOC, the lender may perform a hard inquiry on your credit report, which could cause a temporary, small decrease in your score. However, once approved, responsible use of the HELOC can positively influence your credit. Timely payments and maintaining a low balance relative to your credit limit can demonstrate financial responsibility and contribute to a healthier credit profile.

Many lenders, like Better, only use soft credit pulls so you’ll be able to get pre-approved for a HELOC without an impact on your credit score!

Refinancing Your HELOC

If you think current interest rates are high, you have the option to refinance your HELOC in the future. Refinancing allows you the opportunity to replace your existing HELOC with a new one on more favorable terms. This could include securing a lower interest rate or adjusting the repayment period – potentially reducing your monthly payments and saving you money over the life of the loan. Keep in mind that while refinancing can bring benefits like a lower interest rate,it’s essential to consider any associated fees or closing costs, i.e. you don’t want to increase your overall financing costs over the life of the loan . Exploring your options and understanding the potential savings can help you make an informed decision.

¹Assumes borrowers are eligible for the Automated Valuation Model (AVM) to calculate their home value, their loan amount is less than $400,000, all required documents are uploaded to their Better Mortgage online account within 24 hours of application, closing is scheduled for the earliest available date and time, and a notary is readily available. Funding timelines may vary and may be longer if an appraisal is required to calculate a borrower’s home value.

²Maximum LTV dependent on borrower eligibility.

³The Variable APR (annual percentage rate) and monthly payment amount shown are based on the information you provided above (and other factors) being initially withdrawn at account opening and are for illustrative purposes only. Your actual APR and monthly payment amount may vary and may be greater. APRs and monthly payments assume: a new HELOC on a single family detached property, you have a debt-to-income ratio (DTI) that is lower than 50%, the maximum points allowed are being paid at closing (only applicable for the Lowest Monthly Payment option selected above, not applicable for the Maximum Upfront cash option selected above), and a home equity combined loan to value (CLTV) ratio based upon information you provided. Advertised APRs will vary with Prime Rate (the index) as published in the Wall Street Journal. HELOC rates start at 9% APR, may be as much as 14.75% APR and are subject to change at any time. Advertised rates are current as of 11/01/2023 and are subject to change without notice. This is not a commitment to lend.

Better Mortgage's HELOC product is available in all states other than TX.

Please note that you are required to draw at least $50,000 or 75% of your credit limit, whichever is greater, at the time of funding (ex. if your credit limit is $200,000, you must draw $150,000 or more at funding). If you would like to draw less at funding, you may lower your credit limit.