Mortgage rates today

Home Equity

Have another rate? Let us match it →

The above rates are estimated rates current as of:

Rates and other loan terms are subject to lender approval and not guaranteed.

Get the latest tips and tools for homebuyers and sellers Sign up →

Get the latest tips and tools for homebuyers and sellers

Mortgage rates today

Mortgage rates are a crucial factor to consider when buying a home or refinancing an existing mortgage. These rates decide how much interest lenders charge you to borrow money, and affect your total loan cost. Knowing your mortgage rate is key for making informed financial decisions and securing the best deal.

What are today's interest rates and why do they matter?

To grasp the importance of mortgage rates, let's start by clarifying what they are. Mortgage rates refer to the current interest rates that lenders offer on mortgage loans. Rates can change based on factors like the economy, Federal Reserve policies, and market expectations.

Your rate impacts the home's affordability and the total interest paid over the loan's life. That's why it's crucial for homebuyers or those refinancing to monitor the current mortgage rates.

When it comes to mortgage loans, the lower the interest rate, the lower your monthly payment will be. For example, the monthly principal and interest payment (not including taxes and insurance premiums) on a $350,000, 30-year fixed mortgage at 6% interest is $2,098, compared to a monthly payment of $1,987 at 5.5% interest.

Factors that affect your current mortgage rate

Your mortgage rate is influenced by several personal and economic factors. Here are some of the key elements that impact the rate you receive:

Credit score: Your credit score and credit history play a significant role in determining the interest rate you qualify for. Lenders use your credit score to assess your creditworthiness and the risk of lending to you. Higher credit scores generally result in lower interest rates, while lower credit scores generally lead to higher rates.

Down payment: Making a 20% or higher down payment can lower your interest rate, because lenders may see higher levels of equity in the property as a lower risk.

Loan term: Loan term is the length of time over which you repay your mortgage. Shorter-term mortgages, like 15 year terms, often come with lower interest rates and less total interest, but higher monthly payments than longer-term mortgages, like 30 year terms, because you pay off a shorter loan term faster.

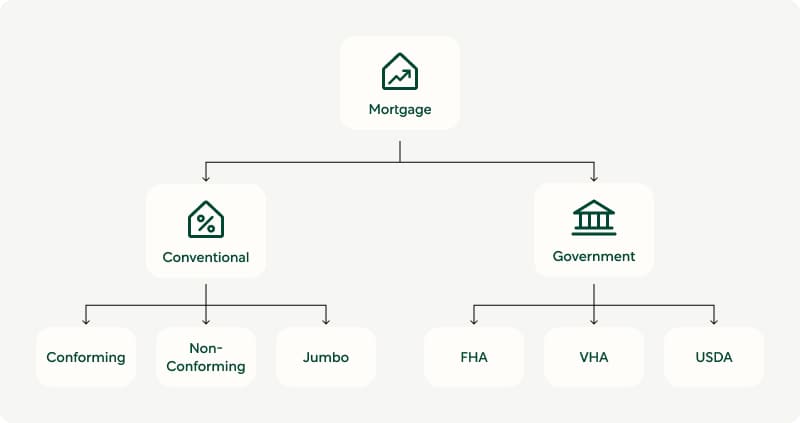

Loan type: The type of loan you choose, such as a conforming loan or an FHA loan, can also impact your interest rate. There are many different loan types with different benefits and qualification criteria. Read up on the types of mortgage loans to understand which might be best for you.

The Fed: The actions of the Federal Reserve can influence mortgage rates as well. The Federal Reserve, the central bank of the United States, sets the monetary policies that affect interest rates. Their decision to raise or lower rates, known as rate cuts, can have an impact on mortgage rates.

Understanding these factors can help you navigate the mortgage process and secure a rate that aligns with your financial goals. For more tips on comparing mortgage offers, see our guide.

Click to see our 2024 mortgage rates housing market forecast and analysis.

How to choose a mortgage rate

Choosing the right mortgage rate is crucial for ensuring that you get the best deal on your home loan. Here are some factors to consider when selecting a mortgage rate:

Fixed versus adjustable mortgage

Understanding the different types of mortgage rates is the first step in the decision-making process. Fixed-rate mortgages have a stable interest rate throughout the loan term, while adjustable-rate mortgages (ARMs) have rates that can fluctuate after an initial fixed period.

There are pros and cons to each type so it's best to determine which one is the best fit for your financial goals.

Research different lenders

Comparing rates from different lenders is essential to ensure that you secure the most competitive interest rate. Obtain rate quotes from multiple lenders and mortgage brokers to find the best deal. Don't forget to take into account the loan officer's expertise, customer ratings, and the lender's reputation.

Consider the length of your loan

Choosing a longer loan term, like a 30-year mortgage, lowers monthly payments but increases total interest paid. A shorter term, such as a 15-year mortgage, has higher monthly payments but can save you a lot on interest in the long run. Evaluate your financial situation and goals to determine the most suitable loan term for you.

Loan comparison calculator

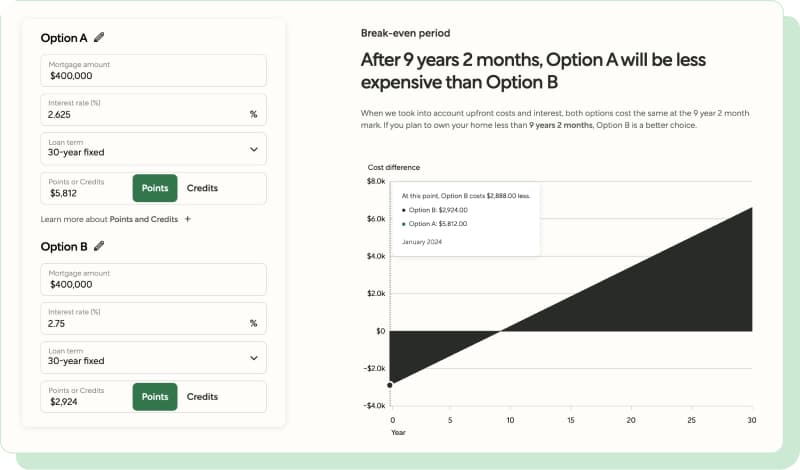

Both points and credits may help you save money on your mortgage, but they do so in different ways. When you purchase mortgage points, you’ll pay more at the closing table in exchange for a lower interest rate. This can provide you with significant savings throughout your mortgage, as a lower rate means you’ll pay less in interest over time.

On the other hand, when you accept lender credits, you can decrease or eliminate your upfront closing cost. The catch? You agree to a higher interest rate for the term of your loan.

So, how do you decide if points or credits are right for you? Typically, if you plan to stay in your home for many years, buying points could save you significant money on interest overall.

Conversely, if you plan to sell or refinance in the next few years, choosing lender credits and saving money upfront may make more sense. Our fixed-rate loan comparison calculator can show you how both would impact your mortgage over time.

What is the current mortgage rate?

Your actual rate may vary based on your financial profile. Get a personalized quote with no impact to your credit score in as little as 3 minutes with our online pre-approval.

See my ratesHow to compare mortgage rates and lenders

Compare APRs: When comparing mortgage rates and lenders, it's crucial to look at the annual percentage rate (APR) along with the interest rate. Lender A might offer you an interest rate of 5.250%, while lender B offers you an interest rate of 5.375%. At first glance, lender A might seem like the better deal. But to truly compare costs, you should also look at the APR.

The APR takes into account not just the interest rate, but also the lender's fees and other loan-related costs, like points you can pay upfront to lower your rate, giving a fuller picture of the total cost to you. If lender A’s offer is 5.250% / 5.816% APR and lender B’s offer is 5.375% / 5.625% APR, then the lifetime cost of lender B’s loan is lower.

Watch out for bait and switch tactics: Lenders may advertise low rates but later reveal higher rates and fees. In some cases, lenders will offer a “fee worksheet” or “initial loan worksheet” to borrowers. This worksheet is a document that outlines estimated rates, terms, and monthly costs based on the initial information you’ve provided.

However, fee sheets are not standardized documents. And since they are not standardized, lenders can choose which fees to include. This means the fees included on a fee sheet can vary from lender to lender. So be sure to request a loan estimate in order to do a side-by-side comparison.

Compare lender fees: Many costs on a loan estimate, like property taxes and homeowners insurance, are not costs that lenders control. Property taxes, for example, are set by your local government, and buyers find their own homeowner’s insurance. To make their offer look artificially attractive, lenders may provide artificially low cost estimates. To strictly compare lenders, check section A and B of your loan estimate. These are the sections that will vary by lender and will tell you which lender is charging less for their services. At Better Mortgage, we believe in letting you keep as much money in your pocket as possible, so we never charge unnecessary fees.

A final important consideration is the option to lock in a mortgage rate. A rate lock allows you to secure a specific interest rate for a specified period, typically 30 to 60 days, protecting you from any rate increases during that time. This can be helpful when interest rates are expected to rise.

What will my monthly mortgage interest payments be?

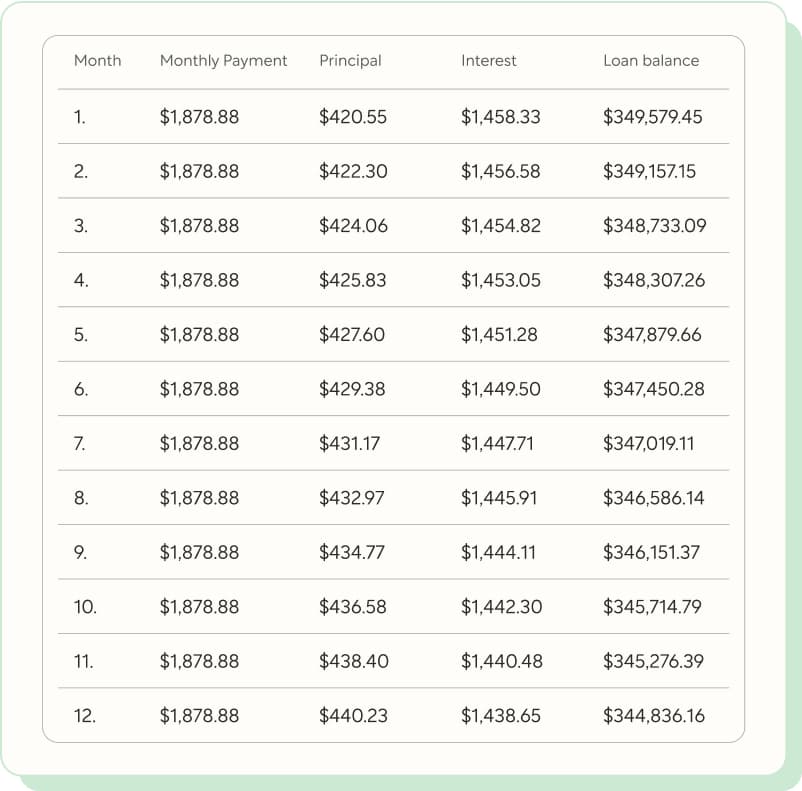

Your monthly mortgage interest payment is calculated based on the annual interest rate divided by 12. For example, if your annual interest rate is 5%, your monthly rate would be approximately 0.417% (.05/12 = .00417). This percentage is then applied to the remaining loan balance each month, resulting in a varying interest amount as you pay off more of the loan.

It's important to note the overall mortgage payment on a fixed-rate mortgage remains the same throughout the loan term. A mortgage payment has two elements, principal and interest. Principal is the amount you still owe on the loan.

To get a better understanding of how interest payments are distributed over the life of a loan, you can use an amortization calculator. Here's an example of amortization during the first year of a 30-year fixed loan of $350k with a 5% interest rate.

Image and monthly payment amounts are for illustrative purposes only.

You can use our free mortgage amortization calculator and table here.

Will I have the same mortgage interest rate forever?

No, you have the option to refinance your mortgage as often as makes financial sense.

Refinancing can be a wise financial move if interest rates have dropped since you obtained your original mortgage. By refinancing to a lower rate, you can lower your monthly payment and potentially save thousands of dollars in interest over the life of the loan. However, it is important to carefully consider the costs associated with refinancing, such as closing costs, to ensure that the savings outweigh the expenses.

Next steps

Find out your max homebuying budget

Try our mortgage calculator →See the cost of any home

Try the mortgage calculator →- Rates can change several times a day, so we make sure you have the latest. We updated them at . Interest rates and APRs are for informational purposes and do not include all applicable fees. Your actual rates, payments, and costs may differ.

- Rates and fees are as of time displayed above and are subject to change without notice.

- The one-time costs shown include points/credits and third-party fees. An escrow deposit, pre-paid interest, and other charges may be required depending on your situation.

- We don’t yet have your complete financial picture. Your actual rate, payment and costs could be higher. Get an official Loan Estimate before choosing a loan.

- Loan approval is subject to underwriter review: not everyone who applies will be approved.

- We also assume: closing costs are paid out of pocket; your debt-to-income ratio is below 35%; you are purchasing or refinancing a single-family home that is your primary residence; you are making a down payment of 20%; and your credit score is 760 or higher.

- Refinancing may cause your finance charges to be higher over the life of the loan.

Get the latest tips and tools for homebuyers and sellers Sign up →

Get the latest tips and tools for homebuyers and sellers