What You’ll Learn

What points and credits are and how they’re calculated

Why you’d choose one or the other (or neither!)

Where they are on your Loan Estimate and how they affect your true loan cost

Whether you’re looking to buy a home or refinance an existing mortgage, points and credits are two words you’ve probably come across.

In this article, we’ll explain what they are, why one option may be preferable over another, and where to find them on your Loan Estimate so you can use them to calculate the true cost of your loan.

Points (also known as discount points), amount to a one-off fee paid in addition to your normal closing costs that let you get a lower interest rate. Paying points allows you to make a trade-off between your upfront closing costs and your monthly payment. Your closing costs will be higher, however, you can take advantage of a lower rate, meaning lower monthly payments and less paid over the life of the loan.

Credits (also known as lender credits) are the opposite of points. You’re taking a higher interest rate in exchange for money from the lender to lower your closing costs or even pay for them completely. In other words, you’re getting credit during closing.

To recap: points mean paying more at closing to get a lower interest rate, and credits mean paying less at closing in exchange for a higher interest rate.

How points and credits are calculated

Points are calculated as a percentage of the total loan amount, with 1 point equal to 1%.

Credits are also calculated as a percentage of the total loan amount. A lender may, at their discretion, offer incentives to decrease points or increase credits (based on the option you've selected) depending on a number of circumstances including promotional offers, etc.

Every lender has a specific pricing structure, which is why different lenders offer the same rates at different prices.

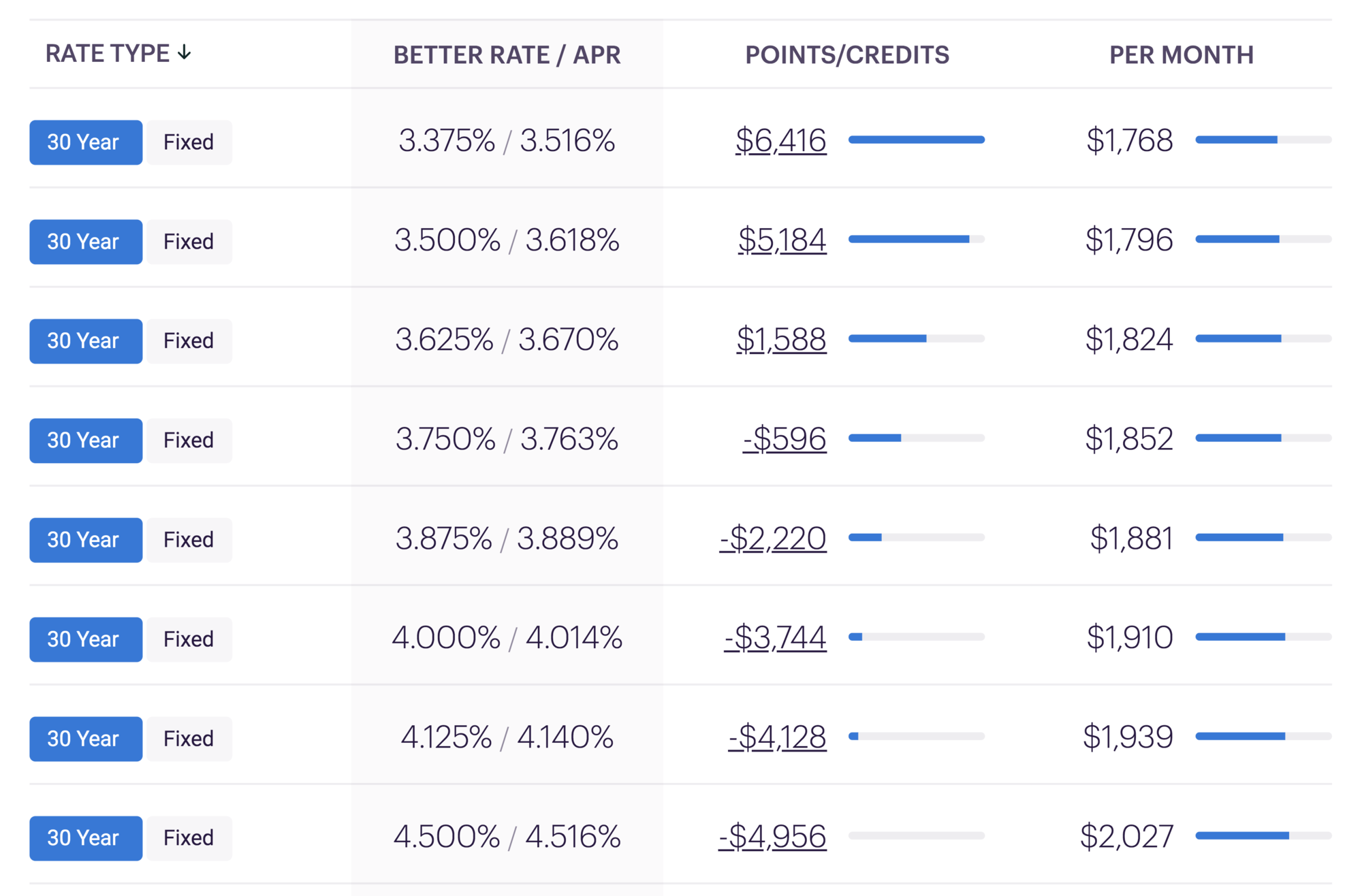

At Better Mortgage, transparency is key to us, which is why points and credits are displayed in actual dollar values when you view your personalized rate options in your Better Mortgage account. Positive numbers in your points/credits column represent points (paying more upfront at closing), and negative numbers represent lender credits (paying less upfront at closing).

Here’s a rate table* you might see from Better Mortgage

How to choose between points or credits

As with a lot of decisions during the mortgage process, the right choice depends on your personal situation. In this case, it largely depends on one of the first questions your Mortgage Expert will ask you:

“How long do you intend on keeping the property that you’re purchasing or refinancing?”

Like a lot of financial choices, there’s a break-even point at the heart of this issue. Most Americans will sell, refinance, or otherwise close within 6 years.

This can change on a case-to-case basis and choosing credits versus points depend on how long you plan on keeping the loan. If you’re like most Americans and don’t plan on keeping the loan for a long time, credits might make more sense. The upfront savings will outweigh any potential savings down the road. If you know that you will keep the loan for a longer period of time, points might make more sense. Your monthly payment will be higher but the long-term savings will outweigh the cost of points upfront.

Keep in mind that you can also choose the par rate, which is the lowest rate option that comes with no points. If you’re unsure about your future plans this might make the most sense.

In addition to time, another factor to think about is how much cash you’re comfortable paying upfront. Remember, points mean more money at closing, credits mean less.

Below are three different situations with the same loan amount, and why you might opt for points, credits, or neither with your rate.

The table below reflects how different situations could affect a loan amount of $250,000

| Situation | Recommendation | Rate | Points/Credits |

|---|---|---|---|

| Your unsure about how long you’ll keep the mortgage, but you still want a low rate. | You may decide to choose the par rate, which is the lowest available rate that comes with no points. You don’t get a lower interest rate, but you also don’t pay more at closing. |

4% | Par rate (no points) |

| You plan on keeping your mortgage for a long time and you have enough cash to closing (or have enough equity in the property to roll your closing costs into the loan) | You may decide to pay a point (an additional $2,500) on top of your regular closing costs in exchange for a reduced 3.875% rate. You pay more at closing but your monthly payment will be lower. |

3.875% | 1% point (+$2,500) |

| You may have plans to sell or refinance your home at some point over the next few years. You also don’t want to bring a lot of cash to closing, and you can afford a higher monthly payment. |

You may decide to accept a higher interest rate in exchange for a $2,500 lender credit. That credit covers some or even all of your closing costs. |

4.125% | 1% credit (-$2,500) |

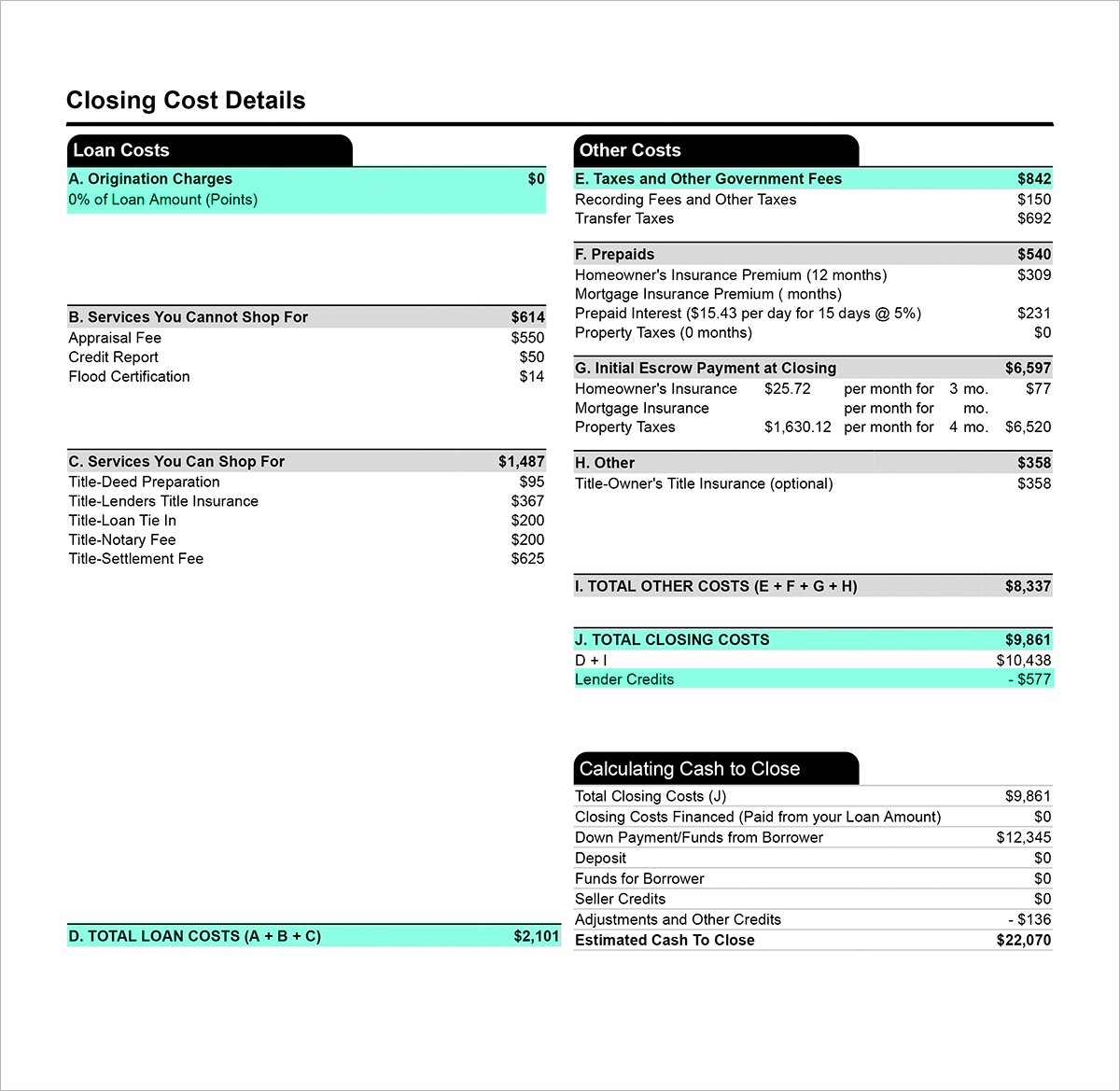

Where to find points and credits on your Loan Estimate**, and how they affect your loan’s true cost

Points will be found under Section A on page 2 of your official Loan Estimate. They’ll be shown as a percentage of your loan amount and as the equivalent dollar amount you’ll pay upfront.

Lender credits are listed under Section J as a negative number. That’s the dollar amount that’ll be taken off your upfront closing costs.

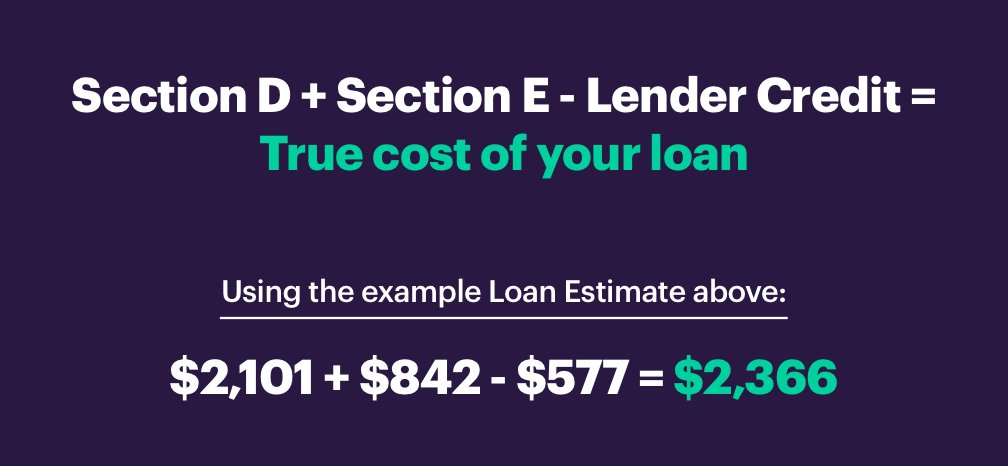

When calculating the true cost of your loan, it’s important to only factor in costs that are mortgage-related (i.e., they occur as a result of the loan itself). The costs to include are listed in Section D (which is the total of Sections A, B, C), Section E, and Section J under lender credits.

Simply input information from your official Loan Estimate into the following formula to calculate your true loan cost:

Costs listed under section F and section G are non-mortgage related, and will occur whether you continue with the loan or not. For this reason, they should not be included in calculating the true loan cost.

Have more questions about points and credits, or need help deciding which is right for you and your loan? We’re here to help.

*The rate table displayed above is for illustrative purposes only. It does not reflect any specific loan terms and is not a commitment to lend. Your loan terms will be different based on current market rates, property type, loan amount, loan-to-value, credit score, debt-to-income ratio and other variables.

**The Loan Estimated displayed in this article is for illustrative purposes only. It does not reflect any specific loan terms and is not a commitment to lend.