Here’s a look at the latest developments in the mortgage market for the week beginning 1/4/21.

- How Better Mortgage helped make 2020 the year of the home

- More homeowners opt to defer or lower their payments amid financial struggles

- Prices rise in middle America as buyers flee coasts

- A guide to the underwriting process

How Better Mortgage helped make 2020 the year of the home

To say that 2020 was a major year for homeownership would be an understatement. In the middle of a global pandemic, homes became more than just living spaces—they were offices, gyms, schools, creative studios, and more. Millions of people chose to buy or refinance in the last year, and Better Mortgage alone took on over 88,000 new clients, funding over $20B in home loans.

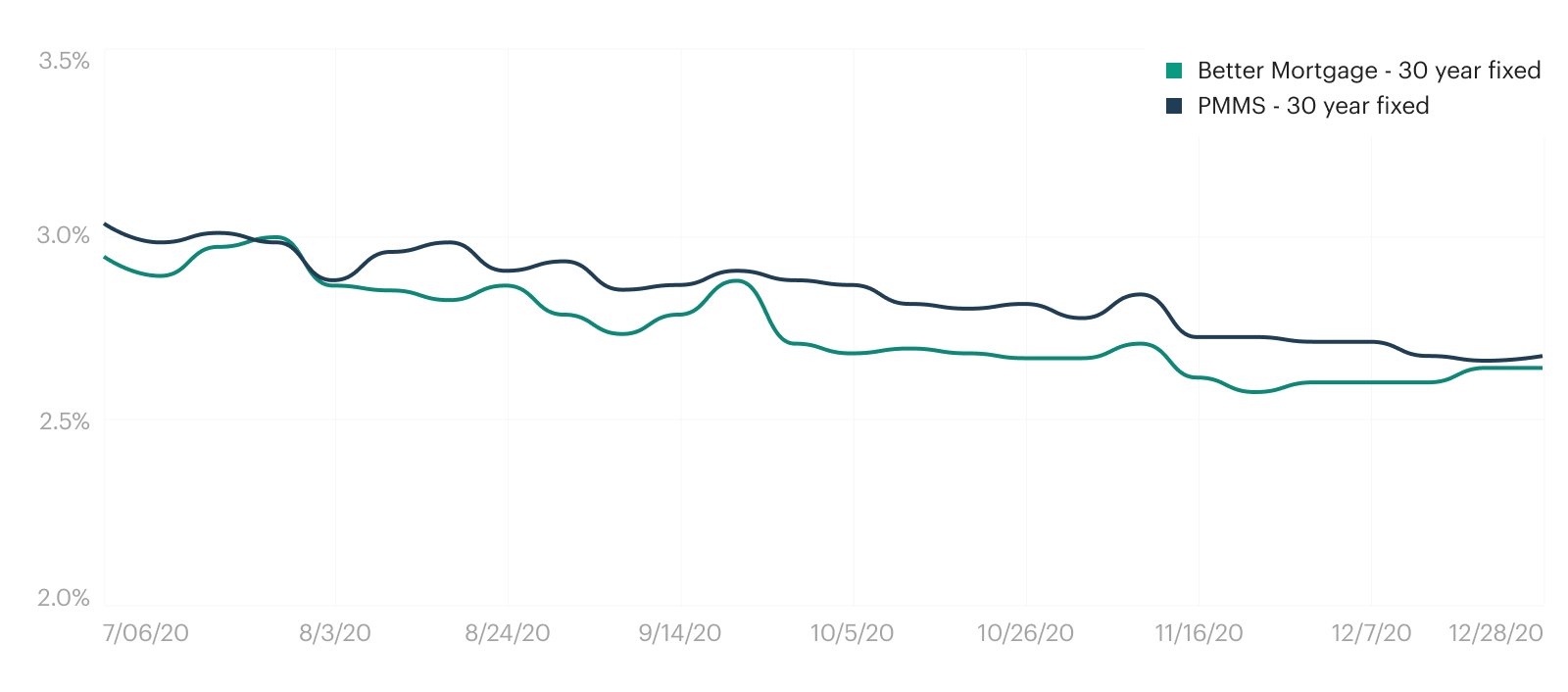

It was a historic year for interest rates. Due to intervention by the Federal Reserve, rates fell below previous records over a dozen times. Better Mortgage was able to offer competitive Market Rates, often lower than Freddie Mac PMMS rates, even as those benchmarks continued to drop.

Better Mortgage Market Rate* vs Freddie Mac Primary Mortgage Market Survey (PMMS) Rate** (July - December 2020)

This is not a commitment to lend. Interest rates are for informational purposes only. Details on rate calculations below.

Economic hardship has been felt everywhere since COVID-19 first emerged in the U.S. in late winter, putting 40 million people out of work by May. With interest rates low, many homeowners took the opportunity to refinance. Better Mortgage saved clients who refinanced an annual total of over $300M.***

On the flip side, the same year saw the demand for homes rise. Many millennial first-time buyers entered the market, contributing to a home buying boom. As sales rose, however, so did home prices. Better Mortgage met the need for an affordable, transparent home loan experience, and saved 2020 homebuyers an average of $8,200 over the life of the loan.****

Looking ahead to 2021, the lasting impacts of the pandemic are expected to keep interest rates low, with a gradual rise throughout the year. There is still plenty of time for loan applicants to take advantage though, especially before prices and sales are expected to climb as the year goes on.

(For more on how Better Mortgage impacted the homeownership landscape, check out our Year in Review.)

More homeowners opt to defer or lower their payments amid financial struggles

Alongside a nationwide vaccine rollout and second economic stimulus package, 2.8 million homeowners ended the year in forbearance. Due to the high demand, the FHA announced they’ve extended the deadline for single-family borrowers to request forbearance up until February 28, 2021.

For a growing number of homeowners, refinancing may be a more financially viable alternative to forbearance. While forbearance is a short-term measure used to avoid defaulting or foreclosure, refinancing is an opportunity to renegotiate the terms of a home loan.

In late December, refinance applications made up three quarters of all mortgage applications, driving a 124% increase from the same period last year.

Prices rise in middle America as buyers flee coasts

Extended work-from-home policies and a desire for more space and comfort drove an urban flight trend in 2020, as families moved away from tech hubs towards suburbs and smaller cities.

Now, prices in those historically affordable cities are rising. Mid-American areas like Pittsburgh, Austin, Cincinnati, Cleveland, are seeing price gains 10% higher than they were last year.

The shift could result in better deals for buyers in traditionally high-priced coastal markets. For example, the Bay Area has seen a slower price incline compared with other cities, despite historically high home values.

A guide to the underwriting process

Underwriting is one of the final steps of the loan process, essentially deciding whether or not a home loan is approved. It involves taking a close look at an applicant’s entire financial picture and paying attention to a series of established risk factors. Here’s a handy guide to what underwriters look for, the documents needed, and a timeline of the process.

Considering a home loan?

Get your custom rates in minutes at Better.com. Our team is here to walk you through your options and help you make an informed decision about which loan is right for you.

*Better Mortgage Market Rates were calculated from an average of rates using the assumptions below to provide a representative offered interest rate for each month. Assumptions include: $200K, $300K, $400K, $500K loan amount; 30-Year Fixed purchase, 30-Year Fixed rate and term refinance; borrower with above average credit (i.e., FICO score of 760 or higher); loan-to-value ratio of 80%; subject property is a Single Family Residence; subject property is borrower’s primary residence; subject property is located in one of our six highest volume metropolitan statistical areas.

**Freddie Mac PMMS Rates are the result of surveys to lenders on the rates and points for their most popular 30-year fixed-rate conventional mortgage products, and an origination-weighted average of lender responses. The survey is based on first-lien prime conventional conforming home purchase mortgages with a loan-to-value of 80 percent. This average is widely regarded as the industry standard tracker of mortgage rates week over week.

***Annual savings in loan payments for each loan are calculated as the monthly principal and interest payment of the borrower’s prior mortgage less the monthly principal and interest payment on their new loan from Better Mortgage, multiplied by 12 (savings are incurred each month in a year). Individual savings could vary based on current market rates, property type, loan amount, loan-to-value, credit score, debt-to-income ratio and other variables.

****The average lifetime savings estimate is based on a comparison of the average interest rate offered by Better Mortgage to prospective borrowers for a $322,000 30-yr mortgage against the Mortgage Bankers Association index from April 2019 to April 2020. Individual savings could vary based on current market rates, property type, loan amount, loan-to-value, credit score, debt-to-income ratio and other variables.