What's a no-closing-cost refinance and is there a catch?

What You’ll Learn

What a “no-cost” refinance really means

The difference between taking lender credits and rolling closing costs into your loan

How to determine if a no-cost refinance is right for you

If you know the saying, “There’s no such thing as a free lunch,” then you may be skeptical when you see an advertisement for a “no-closing-costs refinance.”

Does this actually mean you can refinance your mortgage for free?

Not quite.

A no-closing-cost refinance means you can refinance your home without having to pay closing costs immediately. However, it doesn’t mean that it won’t cost you anything at all.

The truth is that there are always costs associated with any mortgage transaction. It’s who pays these costs at closing that is the determining factor between two possible scenarios in a no-cost refinance situation. Here’s what you need to know about how you can refinance without paying any money upfront out of pocket, and how a no-cost refinance can affect your short- and long-term mortgage expenses:

What is a no-closing-cost refinance?

First things first, when you refinance your home, you effectively swap your old mortgage for a new one. You may be considering a refinance for a ton of reasons—a better interest rate, a shorter mortgage term, or even to trade some of the equity you’ve built in your home for cash. Refinancing is another tool to help you achieve your financial goals. However, it’s important to keep in mind that every mortgage has a certain number of associated costs that are required to complete the transaction. There are appraisal fees, escrow fees, credit report fees… Some lenders (not Better Mortgage) even charge origination fees for taking out the mortgage in the first place. These expenses are paid either upfront or at the closing table—and they can really add up.

With that said, there are ways to have your refinance expenses “baked” into the overall costs of your mortgage. Doing so prevents you from paying any money out of pocket to refinance your home, which can be ideal if you’ll also end up with lower monthly payments or a shorter loan term. One way to secure a no-cost refinance is letting the lender pay all of these costs with lender credits in exchange for a higher interest rate. The other and, in our view, more advisable no-cost refi option, allows you to roll your closing costs into your principal loan amount.

Let’s compare both scenarios to show you how you might fare, and explain why rolling in your closing costs might be a better option.

A no-closing-cost refinance with lender credits

A common way for lenders to advertise a no-cost refinance (with a big asterisk) is through lender credits—which allow the lender to absorb closing costs in exchange for you paying higher interest. The exact increase in your interest rate depends on several factors, including the lender, the type of loan, the amount of closing costs covered, and the available mortgage rates at the time.

If you choose to take this route, your new principal loan amount (the total amount that you’re borrowing for your new loan) will be enough to pay off your existing mortgage. However, it’s worth noting that a higher rate will result in a higher monthly payment for as long as you have that mortgage compared to the rate you would have secured if you didn’t trade a lender paying your closing costs for that higher rate.

A no-cost refinance with “rolled in” closing costs

Another way to avoid paying any money out of pocket for a refinance is to borrow a higher loan amount to cover your closing costs. In this scenario—also known as “rolling in your closing costs”—the total amount of your closing costs is added onto the principal balance of your new mortgage and there’s no change to the interest rate.

Here’s how it works: Let’s say your existing loan amount is $320,000 and you’re faced with $6,400 in closing costs to refinance. If you decide to roll in the closing costs, your new refinance loan amount will be $326,400 and you wouldn’t pay anything up front.

Unlike lender credits, rolling in your closing costs usually means no changes to your interest rate. Instead, you’ll likely receive the lowest rate you qualify for through your lender. If you’re interested in rolling in your closing costs, there is one thing to note: it will change your loan-to-value ratio (LTV). As a refresher: Your LTV is a measure of how much money you are borrowing versus the property’s value. LTV matters because if your new loan amount is greater than 80% of your appraised home value, then you may be required to pay private mortgage insurance (PMI), which will also raise your monthly payment. Having too high of an LTV may prevent you from being able to refinance altogether.

Lender credits vs. rolled in closing costs

| Taking lender credits | Rolling closing costs into your loan | |

|---|---|---|

| Who pays the closing costs | Your lender (credits) | You |

| What goes up | Your interest rate | Your principal amount |

| What stays put | Your principal loan amount | Your interest rate |

| How this impacts you and your loan | You may pay more in interest over time | You’ll have a higher loan amount |

How to choose between lender credits and rolling in closing costs

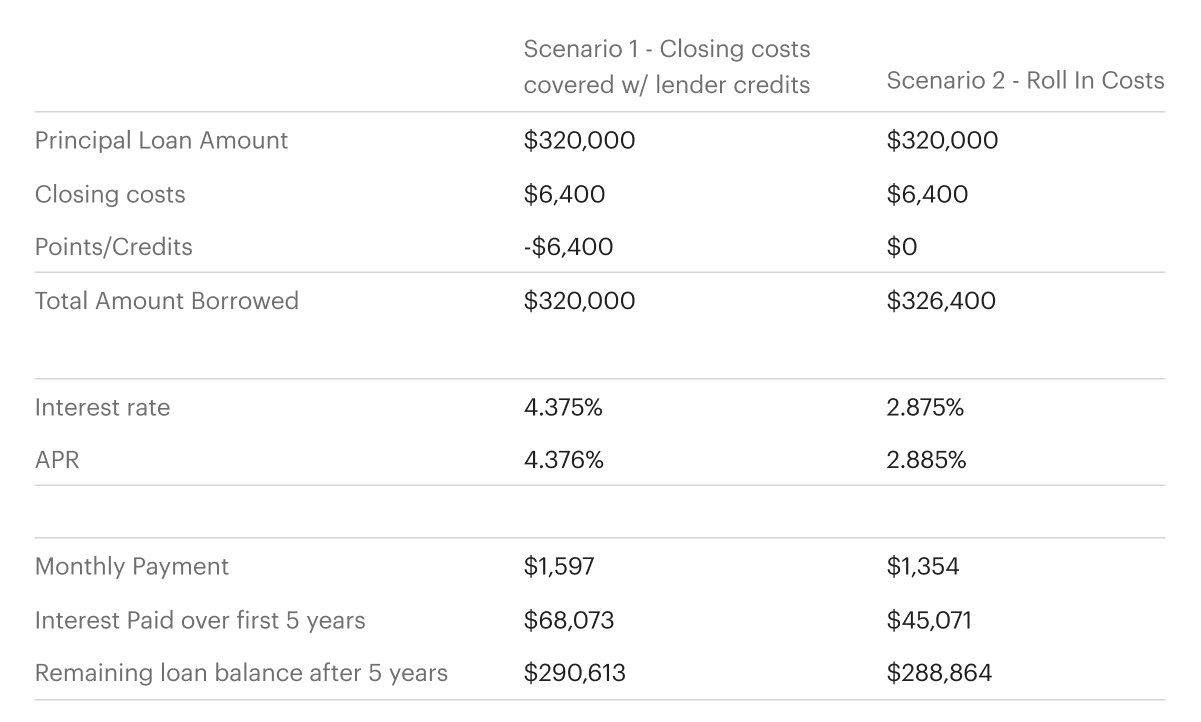

To determine whether taking lender credits or rolling in closing costs makes more sense, you have to figure out the short- and long-term impact of both. Using the earlier example, let’s say your loan amount is $320,000 and your estimated closing costs are $6,400.

This image is for illustrative purposes only.

Impact of a higher interest rate versus a higher loan amount

Scenario 1: Lender credits

Your lender may allow you to take lender credits which will give you an interest rate of 4.375% over the life of your loan in exchange for paying no closing costs up front. Your monthly mortgage payments become $1,597, not including PMI, property tax or homeowners insurance.

Scenario 2: Rolling-in closing costs

If you wish to roll-in all of your closing costs, then you’ll have a higher loan amount, which we have rounded up to $326,550. However, your interest rate is lower and your monthly payments become $1,354.

While the $243 difference in monthly payment between the 2 scenarios may seem relatively low, it adds up significantly over time. In fact, taking lender credits would be an additional $23,000 over the next 5 years.

In this scenario, the math seems to support Scenario 2—rolling in your closing costs. If you want help with any of this stuff, you can use our super simple refinance calculator to see how much you’ll pay in interest charges for both scenarios.

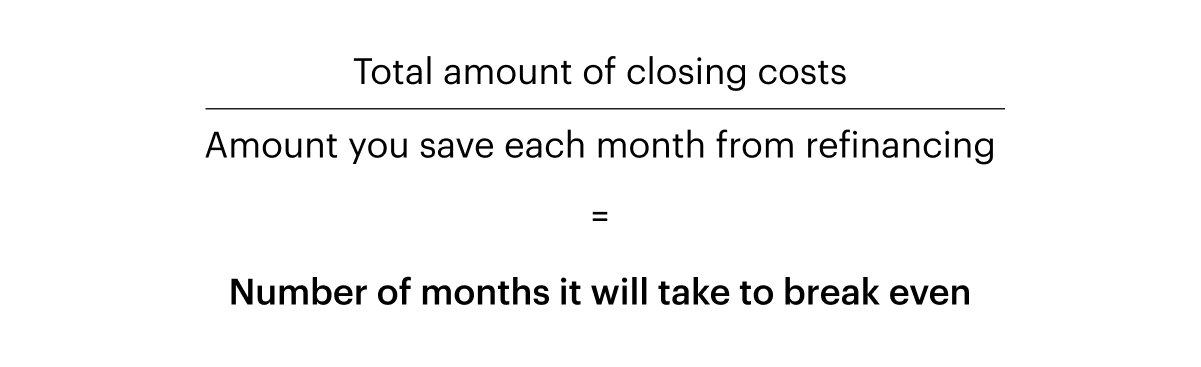

Calculating your break-even point

When it comes to any refinance, you should always calculate your “break-even point” before you make any decisions. This is the number that determines how long it will take to recoup the cost to refinance. It can also be considered the point at which you’ll have saved enough money from refinancing to cover your closing costs. You can calculate it as follows:

For example, let’s say your current monthly principal and interest payment is $1,733. Using the same scenarios from above, you’ll save $136 per month over your existing mortgage payment under Scenario 1 with lender credits (higher rate, lender credit toward costs):

No-cost refi with lender credits

$6,400 (closing costs you save) / $136 (monthly payment savings) = 47 months until you reach your break-even point

Now, let’s consider Scenario 2 where you’ll have a lower rate with closing costs rolled in. You’ll save $379 per month over your existing mortgage payment:

No-cost refi by rolling-in closing costs

$6,400 (closing costs you save) / $379 (monthly payment savings) = 17 months until you reach your break-even point

In Scenario 1, it takes you 30 months longer to recoup the expense of refinancing, and the interest you’ll pay over the next 5 years is substantially higher—a whopping $23,002.21 higher.

In the end, while it may seem counterintuitive, the better loan option is the no-cost refinance with closing costs rolled in. Though it has a higher loan amount, it does allow you to take advantage of your savings faster and pay less interest over time.

Something we can all get behind: Fewer closing costs

While there’s no such thing as a no-closing-cost refinance, covering all of your closing costs through lender credits or rolling them into your loan can provide you with the flexibility of not having to come up with thousands of dollars at the closing table. Deciding which option is better for your circumstances comes down to the math. By determining your break-even point and how much each option will cost you over the life of the loan, you’ll be able to decide which makes the most sense for you.

Remember, regardless of which loan you choose, the lower your closing costs, the less they’ll impact your bottom line. With most mortgage lenders, closing costs comprise lender fees and third-party fees. But at Better Mortgage, we never charge lender fees. That means there are no loan officer commissions, lender origination fees, application fees, or underwriting fees to inflate your closing costs—saving you more over the life of your loan. Crunch the numbers and see how much you could be saving every month with a refinance—we’ll even help you roll in closing costs ;)