Mortgage tax deductions you should know

What You’ll Learn

Which mortgage interest payments and property taxes the IRS allows homeowners to deduct

How marginal tax rates, tax credits, and tax deductions work

How to determine the true cost of your mortgage payment

How does buying a house affect taxes?

A home loan is typically the largest debt that most of us will ever take on. But being a homeowner can also qualify you for some unique financial benefits. In fact, some of the costs related to owning a home, such as mortgage interest payments and private mortgage insurance (PMI), are considered “deductible.” That means they can be subtracted from your total taxable income, reducing the amount of federal taxes you owe each year. If you qualify for these types of mortgage-related tax deductions, it will only make sense to claim them when the total of your itemized deductions exceeds your standard deduction. You’ll want to see how much your deductibles reduce your total taxable income, and whether that reduction puts you in a significantly different tax rate bracket. Tl;dr: The true cost of your mortgage might be less than you think.

Let’s take a look at how you might be able to deduct some mortgage interest costs and PMI from your taxes.

Home mortgage interest

All mortgage payments are composed of principal (the original amount of money that you borrowed) and interest (the cost associated with borrowing that sum, expressed as a percentage rate.) The IRS allows homeowners to deduct mortgage interest if the following conditions are met:

- Your mortgage is for a primary or secondary residence

- Your mortgage is a secured debt—meaning it uses your home as collateral to protect the interests of the lender

- You file your taxes with a Form 1040 tax return, and you itemize deductions on Schedule A

Deductible mortgage interest falls into one of three categories:

- Mortgages you took out on or before October 13, 1987

- Mortgages you (or your spouse, if filing a joint return) took out after October 13, 1987, and prior to December 16, 2017, but only if the mortgage debt totaled $1 million or less ($500,000 or less if married and filing separately)

- Mortgages you (or your spouse, if filing a joint return) took out after December 15, 2017, but only if debt totaled $750,000 or less ($375,000 or less if married and filing separately)

The dollar limits for mortgages made after October 13, 1987 apply to the combined mortgages on your primary home and second home. It’s important to note that the size of your mortgage loan may limit the deductibility of your loan interest.

Private mortgage insurance

If your down payment on a home is less than 20%, your lender will probably require you to take out private mortgage insurance (PMI). This protects the lender in the event that you are unable to make mortgage payments and default on your loan. Once you’ve built up 20% equity in your home, you can request to cancel PMI. Until then, the monthly cost of your PMI payments will differ based on the type of mortgage you have and the size of your down payment, so it’s important to find the mortgage that’s right for you. A smaller down payment will typically mean a larger monthly PMI cost.

PMI became tax deductible for qualifying homeowners starting in 2007. However, in 2017, Congress successfully changed the legislation, only for it to be reinstated again in 2020. This means you can deduct PMI now and retroactively for payments made between 2017–2020.

To qualify for PMI tax deduction, you must have bought or refinanced your mortgage after 2007 and your home must be a primary or secondary residence. If your adjusted gross income exceeds $109,000, you can’t claim PMI.

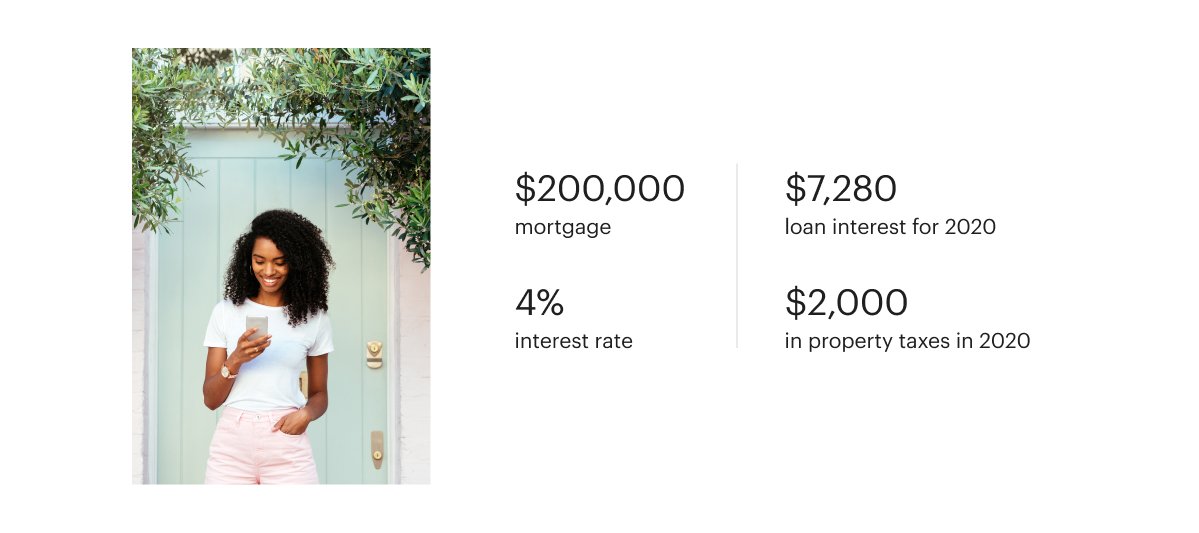

For example, let’s take a look at Sally’s mortgage

This image is for illustrative purposes only

On December 31, 2019, Sally took out a $200,000 mortgage at a 4% interest rate. Using a mortgage calculator, we’ll say Sally paid $7,280 in loan interest for 2020. In that same year, she paid $2,000 in property taxes. Mortgage interest and property taxes are deducted on Schedule A of Form 1040. You can read more about the fine print on home mortgage interest deduction in IRS Publication 936.

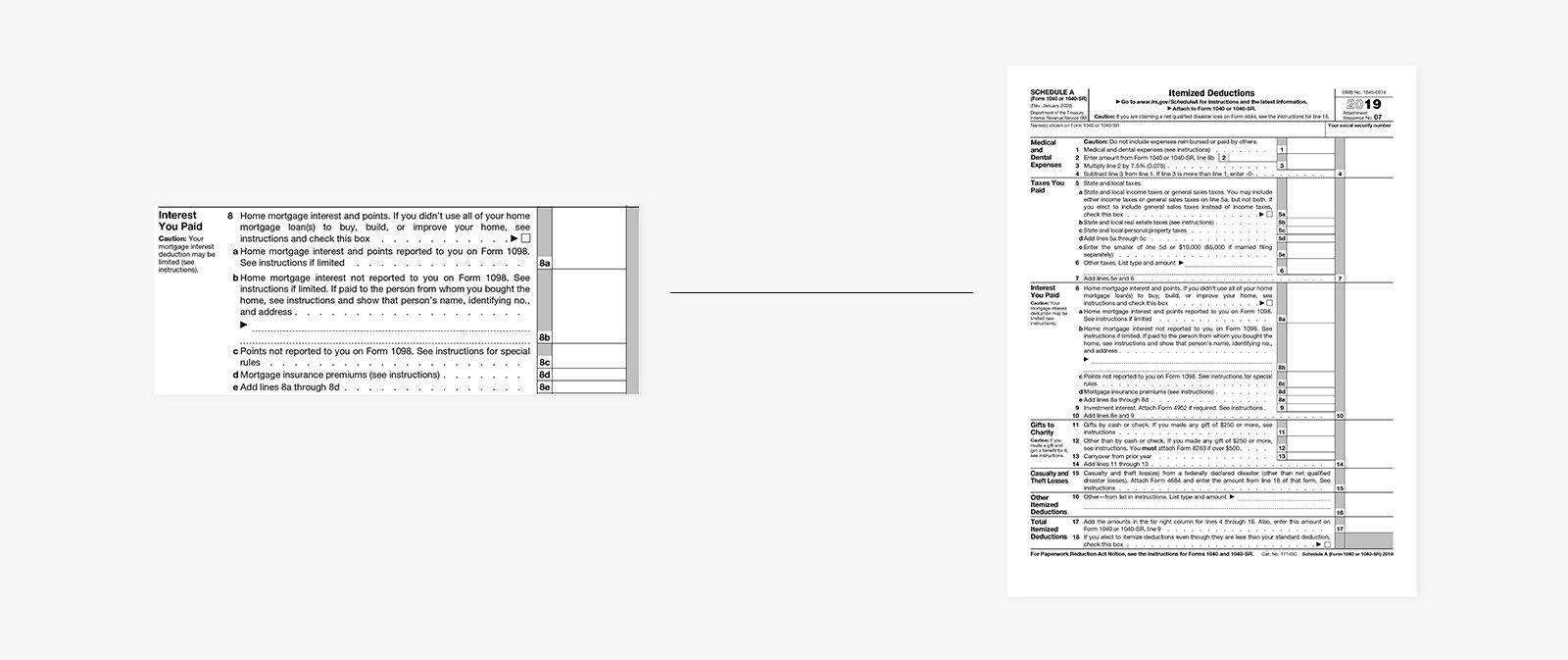

Schedule A

Sally paid points on the home purchase in 2019 and those are deducted on Schedule A, line 8 along with her home mortgage interest payments. Here are Sally’s itemized deductions for 2020:

- Mortgage interest: The bank provided Form 1098, which listed the $7,280 in loan interest

- State and local taxes: Sally paid $4,500 in state and local taxes and $2,000 in property taxes in 2020 —a total of $6,500

- Charitable donations: $1,500

In Sally’s case, her itemized deductions in 2020 total $15,280 which is more than the $12,200 standard deduction, so she elects to use the higher itemized amount on her tax return.

The true cost of Sally’s mortgage is reduced by the mortgage interest as well as the state, local, and property taxes that she paid throughout the year. These items can all be deducted on her tax return. The exact dollar value of the deduction is based on Sally’s marginal tax rate.

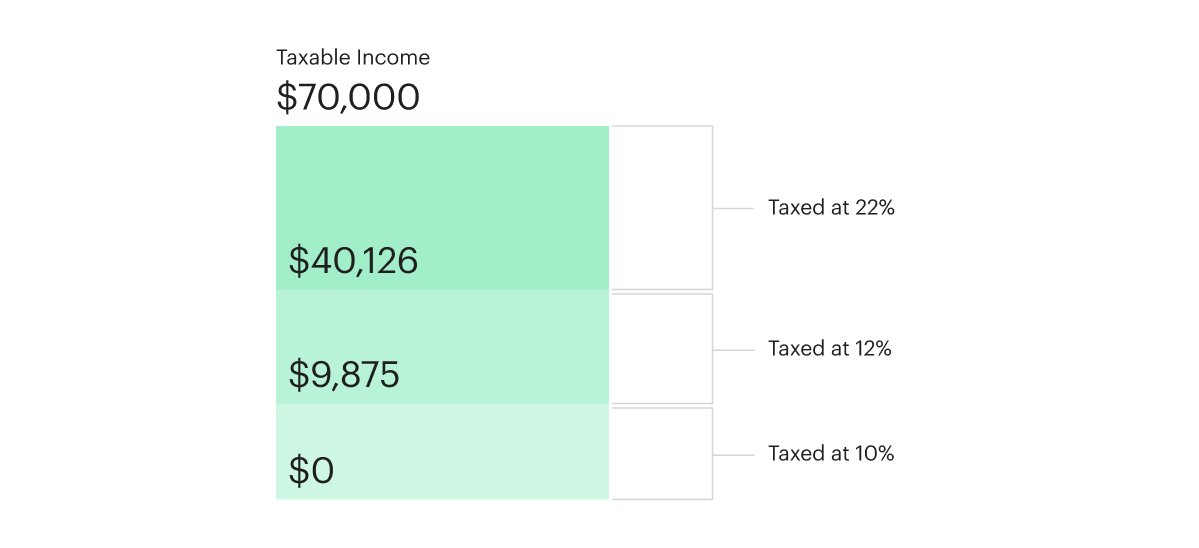

Understanding marginal tax rates

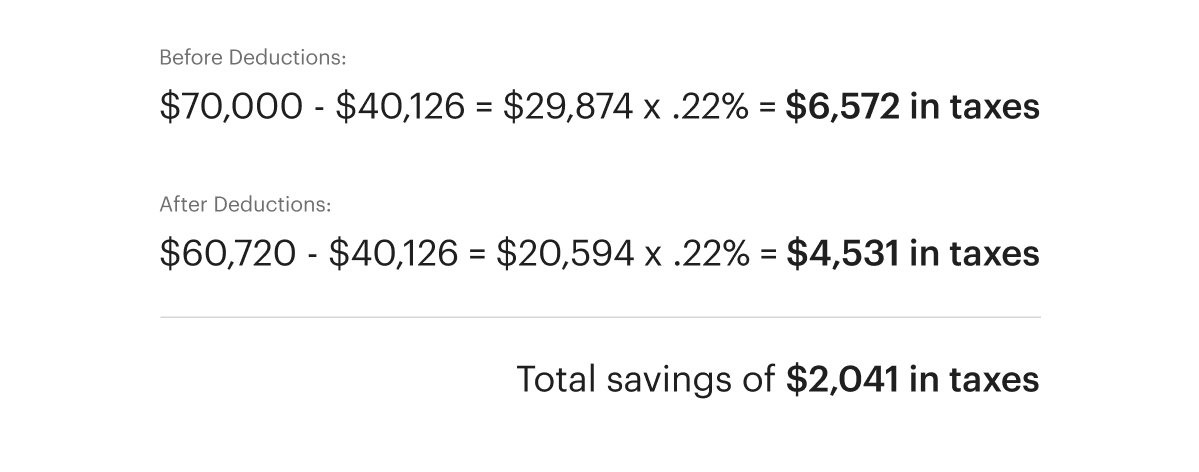

The federal government taxes your income based on a bracketing system. These brackets section out different income ranges, and your tax rate is determined by wherever your income falls on that scale. If you’re a single taxpayer in tax year 2020, you may be subject to as many as 7 different brackets, each with a unique tax rate, depending on your total taxable income. Marginal tax rates work by applying different rates for each subsequent bracket of qualifying income. For example, Sally pays a 10% rate on her first $ $9,875 in earnings, and 12% on earnings between $9,876 and $40,125. If she earned $70,000 she would be taxed at a 22% marginal tax rate.

But Sally’s mortgage interest and property taxes total $9,280 in deductible costs, and subtracting those expenses brings her total taxable income down to $60,720. This is important because it reduces the amount of dollars in the bracket subject to that 22% tax rate.

This image is for illustrative purposes only

By subtracting $2,041 in savings from the total of $9,280 paid in interest and property taxes, the true cost of Sally’s mortgage is $7,239. If Sally’s taxable income was higher, the deductions could potentially be worth more.

Let’s say instead that Sally’s taxable income is $100,000 which puts her in a 24% marginal tax bracket as a single filer. The true cost of Sally’s mortgage would be ($9,280 interest and property taxes — $ 2,228 tax savings), or $7,052. The higher deduction lowers the true cost of Sally’s mortgage.

Tax credit vs. tax deduction

Assume that Sally’s state provides a $500 tax credit to homeowners who install solar panels. If Sally takes the credit, her state tax liability (the amount she owes) is reduced by $500.

A tax deduction, on the other hand, reduces your taxable income rather than your tax bill. Sally’s $85,000 of taxable income is reduced by the mortgage interest and property taxes paid. She could apply the tax credit toward the total amount she owes after everything has been calculated. It’s important to understand the difference between a tax credit and a tax deduction so you can file your taxes correctly and avoid surprises.

How to determine the true cost of your mortgage

Take these steps to determine your mortgage-related tax deductions:

- Determine if you can take the itemized deduction. Again, your itemized deductions should total more than your standard deduction. The PMI and mortgage interest tax deduction only apply if you itemize.

- Gather your tax documents. You should receive a 1098 form that reports the mortgage interest payments you made throughout the year, and your local government will send a statement that reports your property taxes paid. If you bought a home during the tax year, you can also deduct the points paid so have your closing statement available. If you just bought a home or you’re in the process of doing so, you probably already have most of this documentation set aside.

- Verify your total mortgage debt. Current tax law states that your mortgage debt must be less than $750,000 in order to deduct 100% of the mortgage interest.

Tax benefits of owning a home

The true cost of any mortgage is closely tied to your taxable income. Higher taxable income usually generates a higher marginal tax rate, and the marginal rate is used to calculate the value of any tax deduction. Understanding the nuances of tax deductions and tax rates can ultimately save you money on your home loan. But as you can see, it’s important to evaluate the details of your financial situation before filing any mortgage-related tax deductions.

In Sally’s case, the total of her itemized deductions was greater than the standard deduction amount—so it made sense to itemize. And since her mortgage balance was less than $750,000, she could deduct paid interest and taxes on her home.

If Sally rented an apartment, she could not deduct the interest and property taxes because renters don’t pay interest on a mortgage loan or property taxes on their homes. Renting might not have as many tax complexities as owning a home, but it also doesn’t offer the same tax benefits. Renters pass the bulk of these tax deductible savings on to landlords. As a homeowner, you’re in a better position to qualify for tax breaks and earn back money on your investment.

Check your tax rates to see what kind of deductions you might qualify for and how those breaks could translate to a better monthly mortgage outlook. Ready to start saving?

This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.