What You’ll Learn

How a cash out refinance works and when it might make sense for you

Qualification requirements for a cash out refinance

What to expect during the cash out refinance process

Here’s everything you need to know about a cash out refinance: What it is, how it works, and the answers to some frequently asked questions.

What is a cash out refinance?

When you refinance a mortgage, you replace your existing mortgage with a brand new one. A traditional refinance can help you lower your interest rate, shorten your loan term, lower your monthly mortgage payments, or, in some cases, all three.

But with a cash out refinance, you’ll get an added bonus — access to a lump sum of cash based on your home equity.

Your home equity is the portion of your home you actually own. Here’s how it’s calculated:

Estimated Home Value - Outstanding Mortgage Balance = Home Equity

For example, if your home is worth $300,000 and your current loan balance is $175,000, then you have $125,000 in home equity.

Your equity generally increases in 2 ways:

- When you make your mortgage payments: As your principal loan balance decreases, you own more of your home.

- When your home value appreciates: This can happen when the cost of houses in your area or throughout the country increases, and as you make home improvements.

Can a cash out refinance be used for anything?

Luckily, how you choose to spend the money from a cash out refinance is completely up to you.

But, that doesn't mean it makes sense to spend the funds on just anything. You want to consider if tapping your equity will be financially beneficial.

Keep in mind, you'll be paying interest on the money you borrow for years to come. You'll also have to pay closing costs, just like you did when you first got your mortgage. Closing costs are typically based on a percentage of your loan amount — around 2-5%. So, they may be slightly more than what you paid last time, as you’ll be borrowing more to access the cash.

But there are plenty of reasons why a cash out refinance may make sense, and actually help improve your financial situation. Here are a few reasons to consider a cash out refinance:

- Home renovations: Not only can renovating improve the look and useability of your home, but it can also increase the value — which means you’ll build more equity.

- Pay off high-cost debt: Mortgage interest rates tend to be far lower than rates for other types of debt, such as personal loans or credit cards. If you have bills or loans with higher interest costs, then it might make sense to pay these off with the proceeds from your refinance.

- A major investment: Your equity could help you pay for a second home or investment property or start a business.

How much money can I cash out?

The amount you can cash out depends on your loan-to-value (LTV) ratio. Your LTV ratio is how much you owe on your home in relation to what your property is worth, expressed as a percentage.

Most lenders, including Better Mortgage, generally allow you to borrow up to 80% of your equity with a cash out refinance.

How to calculate loan-to-value ratio (LTV)

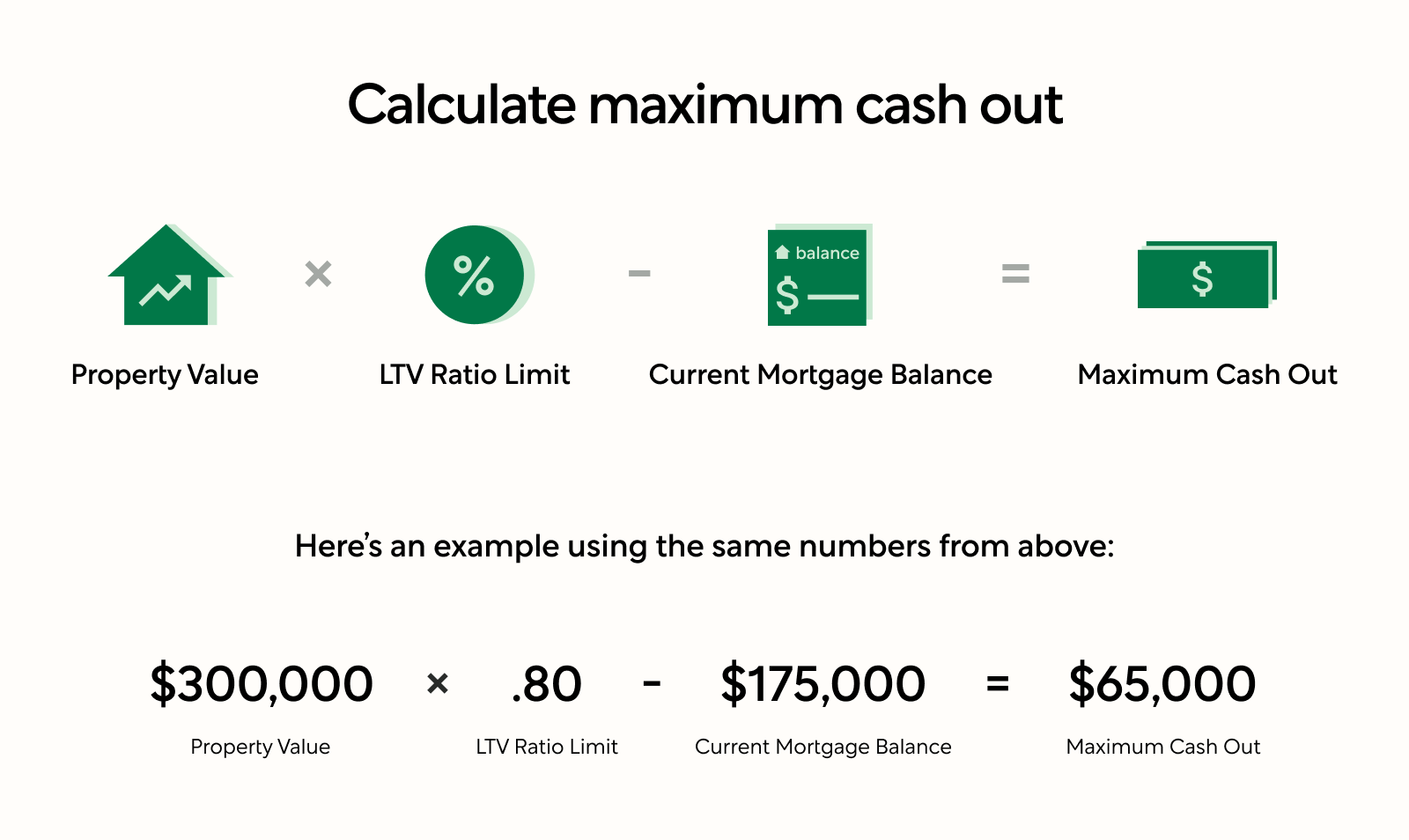

Here’s a simple example to calculate the maximum amount of cash you can take out:

Property Value x LTV Ratio Limit - Current Mortgage Balance = Maximum Cash Out

Here’s an example using the same numbers from above:

- Estimated home value: $300,000

- LTV ratio limit: 80%

- Current mortgage balance: $175,000

$300,000 x .80 - $175,000 = $65,000

In this scenario, you’d be able to cash out a maximum of $65,000. Of course, this is a basic example for illustration purposes. Your final amount may be less due to closing costs or other expenses associated with your loan.

Is my monthly mortgage payment going to change?

With a cash out refinance, your monthly mortgage payment will likely change. This can happen for a few reasons:

- Your principal balance will be higher than your current mortgage to account for the additional cash you’re accessing from your equity.

- Your mortgage interest rate may increase or decrease, according to current market rates and your financial profile.

- Your loan term might change. For instance, if you’ve paid your mortgage for 5 years already, and refinance to another 30-year loan, then your term would be extended for 5 years.

While you might assume that your payments will increase due to the larger loan balance, this isn’t always the case. For example, if interest rates have decreased or your credit score has improved since you got your loan, then your new mortgage payments could be lower — even with the additional cash out. You may also be able to ditch private mortgage insurance by refinancing. Of course, your payments could be higher, too — but you’ll have cash in your pocket for your goals.

Your lender will provide you with a loan estimate you can review before you accept the new mortgage terms, so you know exactly how your refinance will impact your budget now and in the future.

Cash out refinance requirements

Although qualification guidelines can vary by lender, here are the typical requirements for cash out refinance approval:

What is the minimum credit score for cash out refinance?

Typically, the minimum credit score for a cash out refinance is 620. However, the higher your credit score, the better the rates you may qualify for, which can lead to significant savings over the life of your mortgage.

What is the maximum debt-to-income ratio?

Your debt-to-income (DTI) ratio is how much you pay toward debt versus how much you earn each month, expressed as a percentage. This calculation helps lenders understand if you’d be able to afford your new loan payment, along with your other debts.

To determine your DTI ratio, simply divide all your monthly debt payments by your gross (pre-tax) income and multiply that by 100.

Generally, you’ll need to have a DTI ratio of 50% or less to qualify for a cash out refinance.

Is an appraisal required for a cash out refinance?

Just like when you first purchased your home — or refinanced the last time — you’ll need an appraisal to confirm that your property is worth at least as much as you borrow. Therefore, an appraisal is necessary for a cash out refinance.

Your appraisal will also confirm the amount you’ll be able to tap into based on your equity.

How does a cash out refinance work?

Here’s the cash out refinance process you can expect with Better Mortgage:

- Pre-approval: Submit basic information about your debt, income, credit score, current mortgage, and property. Receive a pre-approval in as little as 3 minutes.

- Loan choice: Review the loan options you received with your pre-approval, and select the mortgage that makes the most sense for your budget and financial goals.

- Rate lock: Order a property appraisal (with a $550 deposit) to lock in your interest rate for up to 60 days while your cash out refinance transaction is completed.

- Information-gathering and processing: Prepare and submit the required documentation, such as pay stubs, bank statements, and tax returns. Your loan underwriter will review everything you send to ensure you meet the qualification guidelines.

- Conditional approval and final review: Receive a conditional mortgage approval or submit any additional information as requested. Your underwriter will then give your file a final review.

- Clear to close: Set a date, time, and location for your closing day. Review your Initial Closing Disclosure (an itemized list of all mortgage-related expenses, including closing costs), ensure any errors get corrected, and sign a final version of the document.

- Closing day: Review and sign all mortgage-related paperwork and pay any required closing costs. At this point, your cash out refinance transaction is finalized!

After you close, your previous mortgage will be paid off, and your new one will be initiated. Then, you can prepare for the excitement of checking your bank account — within just a few days, that pile of cash will be waiting for you.

How long does a cash out refinance take?

With a traditional lender, the mortgage refinance process can take around 5 to 7 weeks, from application to closing.

But the entire application process at Better Mortgage’s is 100% online, so it’s possible to close much faster. In fact, our average closing time is 10 days faster than the industry average.

Why you should cash out with Better

Here’s why you can expect a better refinance experience with Better Mortgage:

- As little as 3-minute pre-approval. Just answer a few quick questions to find out if you’re pre-approved.

- Close faster. Our 100% online application process can shave days off the transaction.

- Save money. We don’t charge any lender fees to process, underwrite, or originate your loan.

- Be supported, not sold. Our loan officers don’t work on commission, so you’ll never get pressured to take on a larger mortgage than you need.

Ready to get started? Find out how much of your equity you can access by refinancing today.

Better Mortgage Corporation. NMLS #330511