If you’re a homeowner, refinancing a mortgage can get you lower payments and better rates. This type of refinancing means replacing your existing home loan with a new one that fits your current needs, like different terms or better interest rates.

But the options for refinancing get complex. Whether you want to adjust the terms of your loan or access your home’s equity, you need to understand refinance mortgage loan types and how they work.

This guide will explain the different types of refinance, their benefits, and how to choose the best one for you.

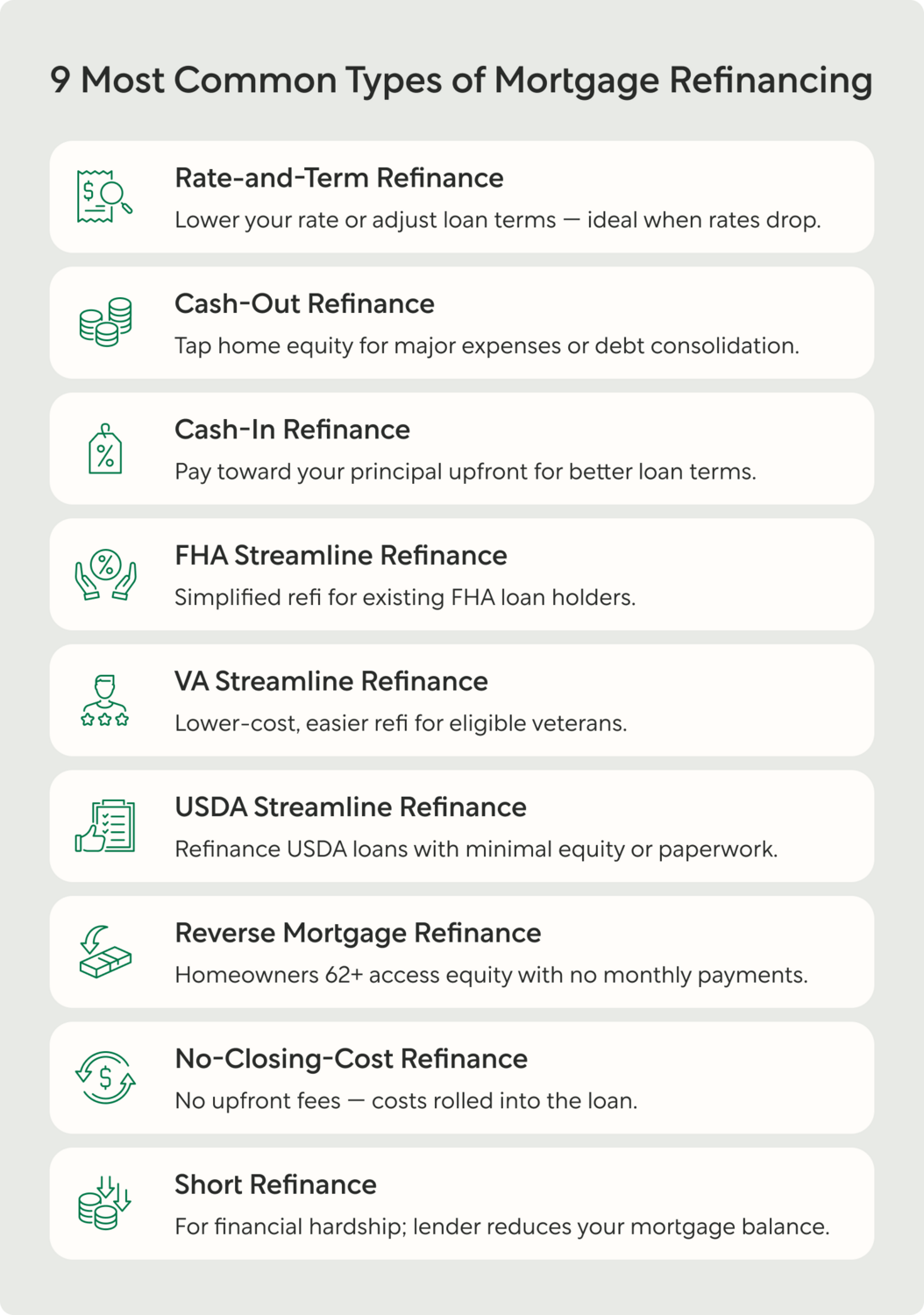

9 types of mortgage refinance

While there are many types of mortgage refinance, these nine options are the most common.

1. Rate-and-term refinance

A rate-and-term refinance lets you change your interest rate and/or the terms of your loan without changing the actual loan amount. It’s one of the most common refinancing options for homeowners, especially when interest rates drop, because it can help you reduce monthly payments or pay off the loan faster.

2. Cash-out refinance

With a cash-out refinance, you take out a new, larger mortgage — one that allows you to receive the difference between your new and existing loans in cash. You might find this kind of refinancing useful for major expenses like renovations, medical costs, or education, and some people even use it for debt consolidation.

For a seamless application process and experience, use Better’s cash-out refinance. Better offers a fully online option where you can access your equity easily in minutes.

3. Cash-in refinance

A cash-in refinance is what it sounds like — the opposite of cash-out. As the homeowner, you pay a lump sum amount toward the principal of your mortgage. This type of loan helps to reduce your loan-to-value (LTV) ratio, and it can qualify you to receive better loan terms overall.

This type of refinance can lower your interest rate and reduce your monthly payments. In some cases, it also helps you avoid private mortgage insurance (PMI) by increasing your home equity to the right threshold.

4. FHA Streamline Refinance

A Federal Housing Administration (FHA) Streamline refinance is a good option if you have existing FHA loans. It provides a simplified process with fewer necessary documentation requirements if you have an FHA, Veterans Affairs (VA), or United States Department of Agriculture (USDA) loan type.

There are typically two types of FHA Streamline Refinance options: A credit qualifying loan requires a credit check and verification of your income, while a non-credit qualifying refinance provides a faster process but more limited borrowing. Regardless of which type of refinancing you choose, you must have an existing FHA loan and proof of on-time mortgage payments.

Better Mortgage offers FHA Streamline Refinancing with no income verification or appraisal requirements for faster processing.

...in as little as 3 minutes – no credit impact

5. VA streamline refinance

If you’re a veteran, active duty service member, or a surviving spouse with a VA loan, a VA streamline refinance can reduce your interest rate or help you switch your type of loan. Available benefits include lower monthly payments, a reduced VA funding fee, and an easy qualification process. You just need to prove full-time home occupancy.

6. USDA streamline refinance

This type of refinancing option is best if you’re a homeowner with existing USDA loans and little home equity. A USDA streamline refinance Streamline Refinance Eligibility, amount at time of purchase allows you to make changes to both your rate and loan term — usually without requiring a new appraisal of your property.

There are two available options for this type of refinance: a Standard USDA Streamline or a USDA Streamline-Assist. The standard option requires you to provide income and credit score verification, while the assist option is easier to apply for and does not have those requirements.

7. Reverse mortgage refinance

A reverse mortgage allows homeowners 62 and older to convert home equity into cash without making monthly payments. You only pay for the loan and accrued interest when you sell your home, move out, or pass away.

A refinance of an existing reverse mortgage typically offers lower interest rates, loan terms, or the ability to access a new and larger loan amount. However, you’ll experience additional costs and eligibility requirements.

8. No-closing-cost refinance

With this type of refinance, you avoid paying any closing costs upfront. Instead, they’re rolled into the loan balance or covered with a higher interest rate. This means no large upfront costs and more savings for other needs.

These kinds of refinance loans are best for short-term homeowners or homeowners with limited cash reserves.

9. Short refinance

A short refinance can help out if you’re experiencing financial distress. With a short refinance, your lender reduces the mortgage balance to an affordable level to avoid foreclosure. While this type of refinance can be an enormous help to those in need, it can negatively impact your credit, so it’s best as a last resort.

Choosing the right mortgage refinance

Selecting the best refinance option depends on your circumstances and goals. Here are some factors to consider:

— Existing mortgage payments, interest rates, and loan terms

— Your financial situation, including your credit score, LTV ratio, and DTI ratio

— Your financial goals

— Your home equity

— How long you plan to stay in the home

— Refinancing terms

— Refinancing closing costs

Not sure where to start? Better offers a fast eligibility check in as little as 3 minutes. Plus, the fully digital application process is simple and convenient — whether you're looking to save on interest, consolidate debt, or take out cash.

...in as little as 3 minutes – no credit impact

Refinancing FAQs

Why would you refinance your home?

Some of the key reasons you may want to refinance include:

— Getting a lower interest rate

— Lowering monthly payments

— Changing loan type or term

— Accessing home equity for major expenses

When is the best time to refinance?

While the ideal time to refinance is when interest rates drop, personal circumstances (like your financial situation and existing payments) can make a refinance loan a good option for you regardless of current rates.

Does refinancing affect your credit score?

It’s true that refinancing typically results in a temporary dip in your credit score due to the credit inquiry. That’s because lenders need to perform a credit check to confirm your qualification. With Better, you can see what you’re pre-approved for without a credit impact, but if you decide to move forward, there will be a credit inquiry in line with the standard process of most lenders.

How often can you refinance a home?

While there’s no legal limitation on how often you can refinance, lenders often have policies in place that limit your timing. You also need to meet loan qualification criteria each time you apply.

How much does it cost to refinance?

You can expect to pay a small percentage of your loan amount in closing costs, depending on the type of refinance loan you apply for. Learn more about the cost of refinancing here.

Can I sell my house after a cash-out refinance?

You can sell your house after a cash-out refinance, but be aware that some mortgage agreements have an owner-occupancy clause. This clause requires you to live in the home for a specific amount of time before selling.

Access your equity the Better way

Understanding the different types of refinance options available is the key to making an informed decision that benefits your long-term financial well-being. Whether you want to lower your interest rate, change your loan terms, or access your home equity, there’s a refinance option that fits your needs.

At Better, we make it easy to explore refinancing options. From a fast 3-minute eligibility check to a fully digital process, we help you find the best refinance option to fit your needs.

...in as little as 3 minutes – no credit impact