Key highlights

A VA IRRRL, or VA Streamline Refinance (or VA Refinance), helps veterans lower their interest rates and monthly payments on existing VA loans.

This program offers a faster and simplified refinance process compared to traditional options.

VA IRRRLs come with less paperwork, often eliminating the need for appraisals and income verifications.

Veterans benefit from lower funding fees, and closing costs can be rolled into the new loan, reducing out-of-pocket expenses.

While offering numerous advantages like lower interest rates and payments, it's essential to weigh your options.

Introduction

Did you get your dream home using a VA home loan but want a lower interest rate? A VA Interest Rate Reduction Refinance Loan could be the answer. This program helps US Veterans, service members, certain reservists, National Guard members, and select surviving spouses to lower their monthly payments and potentially save money on interest.

Understanding the VA IRRRL Program

The VA IRRRL stands for VA Interest Rate Reduction Refinance Loan. It is a great benefit for qualified VA borrowers, including veterans, active-duty members, and some surviving spouses who qualify. It is otherwise known as a VA Streamline Refinance. This program helps homeowners change their current VA loan to a new one with better terms, usually with a lower interest rate.

The goal of this program is to make refinancing simpler for VA loan holders. It makes the process easier, often allowing you to skip new appraisals and submit less documents. This option is especially appealing for those looking to lower their interest rates quickly and easily.

What is a VA IRRRL Loan?

A VA Streamline Refinance requires minimal paperwork and fast processing. It is an entitlement as part of your VA benefits, designed to thank you for your service. With this product, you can get better terms like a lower interest rate, or switch from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage.

In short, it's a way to refinance your current VA loan without the hassle of a traditional refinance. Better's VA IRRRL requires no home appraisal and no income verification. Plus, with the option to roll closing costs into the new loan balance, it gives you a lower monthly mortgage payment with virtually no out-of-pocket costs.

Benefits of refinancing with a VA Interest Rate Reduction Refinance Loan

Choosing a VA IRRRL can offer many benefits over other refinance options:

Lower interest rate

The primary reason veterans and their families often choose to refinance a VA loan is to obtain a lower interest rate. The VA recommends considering a VA IRRRL when the new interest rate is lower than the original loan's rate. At Better, we will only refinance your mortgage if there is a "net tangible benefit", meaning there must be a clear, measurable advantage that you gain from refinancing your existing loan.

Lower monthly payments

If you're considering refinancing with a VA Streamline, you could see a reduction in your monthly mortgage payments. This decrease may come from extending the loan term, giving you more time to pay off the mortgage. Alternatively, securing a lower interest rate can also reduce your monthly payment, provided the loan term remains the same.

Low funding fee

For a standard VA loan, the funding fee ranges from 1.25% to 3.3% of the loan amount, depending on service status. For a VA Streamline (IRRRL), the funding fee is a flat 0.5% of the loan amount.

However, certain borrowers are exempt from paying the funding fee. Exemptions include:

These exemptions aim to reduce the financial burden on veterans, active-duty service members, and their families when refinancing a VA loan.

Switching from ARM to Fixed-Rate Mortgages

For homeowners with adjustable-rate mortgages (ARMs), the VA IRRRL program is a great chance to switch to a fixed-rate mortgage. With ARMs, homeowners face the risk of sudden payment hikes when interest rates go up. This can make budgeting hard.

By refinancing to a fixed-rate mortgage, you can lock in your interest rate for the life of the loan. This gives you stability and peace of mind. Here are some benefits:

Eligibility Criteria for a IRRRL VA Loan

Before you enjoy the benefits of the VA IRRRL, make sure you are eligible. One main requirement is that you need to have an existing VA loan. This means you cannot refinance from a conventional loan, FHA loan, or any other type of loan to a VA IRRRL.

Also, homeowners must show that they have made their mortgage payments on time, as well as show that refinancing offers a clear financial benefit.

Qualifying for a VA IRRRL Refinance

The VA IRRRL program has an easy process, but there are basic requirements to qualify. First, you need to have a VA home loan already. This program is only for people who currently have a VA loan and does not include other loan types. Second, you need to be in good standing with your mortgage company — meaning no late payments in the past 12 months.

Better's VA IRRRL product allows a credit score minimum of 580 and does not require a Certificate of Eligibility (COE). In addition: the property you refinance must be your primary residence. This means you cannot use the program for investment properties or vacation houses.

Last, the new loan amount cannot be more than what you owe on your current loan, plus any allowed closing costs and fees. This rule keeps the program focused on just refinancing, rather than taking out cash from home equity.

It's important to note that there are time limits. Usually, you need to have made at least six timely payments on your current VA loan and have lived in the property for at least 12 months.

The Application Process for VA IRRRL

The VA IRRRL program is great because it has a simple application process. It reduces the trouble that comes with regular refinancing options. This makes it fast and easy for qualified borrowers.

Usually, you work directly with a lender approved by the VA, like Better.

Preparing Your Documents for Application

While the VA IRRRL process makes it easier by needing fewer documents, having the important papers ready can speed up your application. Other lenders may ask for employment verification, even though it's not required. So, it helps to have recent pay stubs and W-2s ready to keep everything running smoothly.

At Better, you will not need to provide your original COE (Certificate of Eligibility) to show you qualify for the VA loan program. Because you are refinancing an existing VA loan, you are automatically qualified as long as you meet other eligibility criteria.

Lastly, you should be ready to provide standard mortgage documents. These often include bank statements to show your financial history, and government-issued ID, like a driver's license or passport, to confirm your identity.

Cost and Fees Associated with VA IRRRL

A VA IRRRL makes refinancing easier, but it's important to know the costs and fees involved. Even though these are usually lower than in traditional refinancing, you still need to pay closing costs and a VA funding fee.

The percent funding fee is a percentage of the loan amount and helps pay for the program. The good news is that the VA IRRRL has a much lower funding fee than other VA loans. You should consider these costs when looking at the overall benefits of refinancing.

Understanding the Funding Fee

The Funding Fee is an important part of the VA loan program, which includes IRRRLs. This fee is a one-time payment that goes to the Department of Veterans Affairs. It helps fund the program and keeps it available for future service members.

For VA IRRRL refinances, the funding fee is usually lower than for a standard VA purchase loan. Right now, it is 0.5% of the loan amount for most borrowers. There are some cases where this fee can be waived, especially for veterans with service-connected disabilities. To see a list of exemptions, revisit the section titled "Low Funding Fee".

Even though it adds to your costs, you do not have to pay this fee upfront. You can include it in the new loan amount. This means you do not need to spend any money out of your pocket when closing.

Closing Costs and Other Expenses

A VA IRRRL may help you save money when compared to other home loan refinance options, but you should be aware of some main costs. Closing costs are fees you will pay to finish your refinance. These costs usually range from 2% to 5% of your loan amount. They include services like title searches and origination fees.

Origination fees are the payments mortgage lenders get for handling your loan. This fee is often a percentage of your loan amount and covers the lender's administrative expenses.

You might also face discount points. These are fees you pay upfront to lower your interest rate. One discount point costs about 1% of your loan amount.

Comparing VA IRRRL with Other Refinancing Options

When you think about refinancing, it’s important to look at the VA IRRRL and other choices. These could include cash out refinance, rate and term refinance, a HELOC, or a home equity loan (HELOAN). Each option has its own details, benefits, and drawbacks.

You need to know how these programs differ in things like eligibility, terms, cash-out options, and costs. This understanding will help you make a smart choice that fits your money goals. Let’s compare some of these options to the VA IRRRL.

VA IRRRL vs. Cash-Out Refinance

Both the VA IRRRL and cash-out refinance help homeowners update their current loans with good terms, but they have different goals. The VA IRRRL is designed to make it easier to refinance for lower interest rates or monthly payments. In contrast, a cash-out refinance lets you use your home equity to get cash.

The cash-out refinance takes your current mortgage and replaces it with a new one. This lets you get cash based on the area between your home's value and what you still owe on the mortgage.

The VA IRRRL is all about making an existing mortgage more affordable while a cash-out refinance gives you the chance to use your home equity for things like home improvements, paying off debts, or other major expenses.

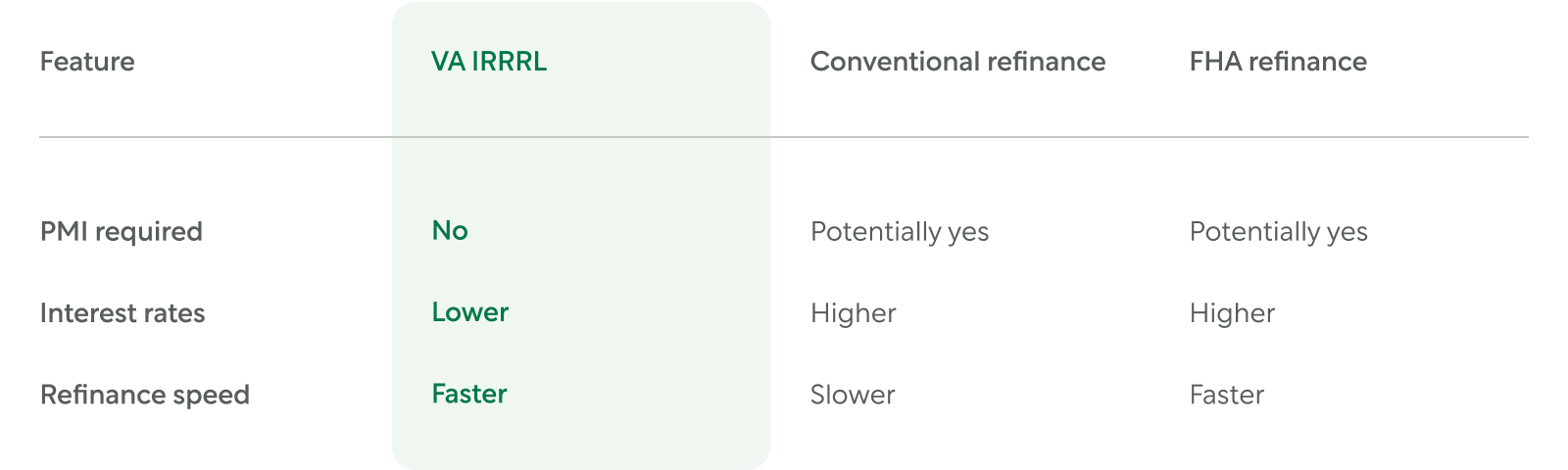

Benefits over conventional and FHA refinancing

VA IRRRLs offer unique advantages, especially for eligible veterans and service members. Firstly, unlike conventional refinance loans, VA IRRRLs don't require private mortgage insurance (PMI), even for borrowers with less than 20% equity.

Secondly, VA IRRRLs often come with lower interest rates compared to conventional and FHA loans, thanks to the backing of the Department of Veterans Affairs. This translates directly to reduced monthly payments and could result in significant long-term savings.

Lastly, the streamlined nature of the VA IRRRL, with less stringent requirements for income verification and appraisals, makes for a faster and more convenient refinancing experience. See a comparison between VA IRRRL, conventional refinance, and FHA refinances below.

Conclusion

In conclusion, the VA IRRRL program is a simple way to refinance. It offers benefits such as lower interest rates and an easier application process. It's a great option for those looking to switch from an ARM to a fixed-rate mortgage, or refinance with the ease and speed of a streamlined process. If you are thinking about refinancing, consider this program to lower your current rates and monthly payments. If you're interested in getting a free quote, click here.

Frequently Asked Questions

Can I use VA IRRRL more than once?

Yes, you can use the VA IRRRL program more than once to refinance a current VA Loan. Each time, you must show a "net tangible benefit," such as a lower interest rate, and be in good standing on your existing mortgage.

What impact does VA IRRRL have on monthly payments?

A refinance using the IRRRL program can help to lower your monthly payment. This happens by getting a lower interest rate. The amount your payment decreases will depend on your new term and the difference between your old and new interest rates.

What are current VA IRRRL rates?

VA IRRRL interest rates will vary depending on factors, such as your credit score. To get a free quote on a VA IRRRL in as little as 3 minutes, click here.

Refinancing may cause your finance charges to be higher over the life of the loan.