Looking to tap into your home’s value without refinancing your entire mortgage? A home equity line of credit (HELOC) could be the flexible financing solution you need.

Think of a HELOC as a loan that uses the difference between your home’s value and the outstanding balance as collateral. With interest rates typically lower than credit cards or personal loans, a HELOC can be a great choice for funding home improvements, consolidating high-interest debt, or covering major expenses. But before you agree to a HELOC, you should understand how to pay it back over both the draw and repayment periods.

This guide walks you through how HELOC payments work, what to look for in a loan agreement, and any penalties you might incur as you borrow. Plus, discover how Better’s streamlined online application process allows you to check your HELOC eligibility in as little as 3 minutes.

How does paying back a HELOC work?

When you take out a HELOC, your repayment process breaks down into two periods. Here’s the basics of how HELOC payments work:

| Feature | Draw Period | Repayment Period |

|---|---|---|

| Duration | Usually 5-10 years | Usually 10-20 years |

| Can you withdraw funds as needed? | Yes | No |

| Payment type | Interest-only payments | Principal plus interest payments |

| Balance | Can increase if only minimum payments are made | Decreases with each payment |

And here’s a deeper look at each period:

HELOC draw period

The first phase of your HELOC is known as the “draw period.” This is when you can take out and use funds. During this time, you only make interest payments, not principal — meaning you only make small payments instead of paying off the credit line.

The draw period varies depending on your loan terms, but usually lasts 5-10 years. Once it ends, you won’t be able to access the money, so it’s important to know the draw period timeline.

Many lenders take 30-45 days to process and fund HELOC applications take time. If you want quick cash, apply with Better to get approved for a $50,000-$5100,000 HELOC and receive the funds in as little as 7 days. Get the resources you need faster than traditional lenders.

....in as little as 3 minutes – no credit impact

HELOC repayment period

When the draw period ends, you enter the repayment period. Now, you pay both the principal and interest you owe each month, similar to a mortgage. The most important change here is that your monthly payment will jump significantly compared to what you paid during the draw period.

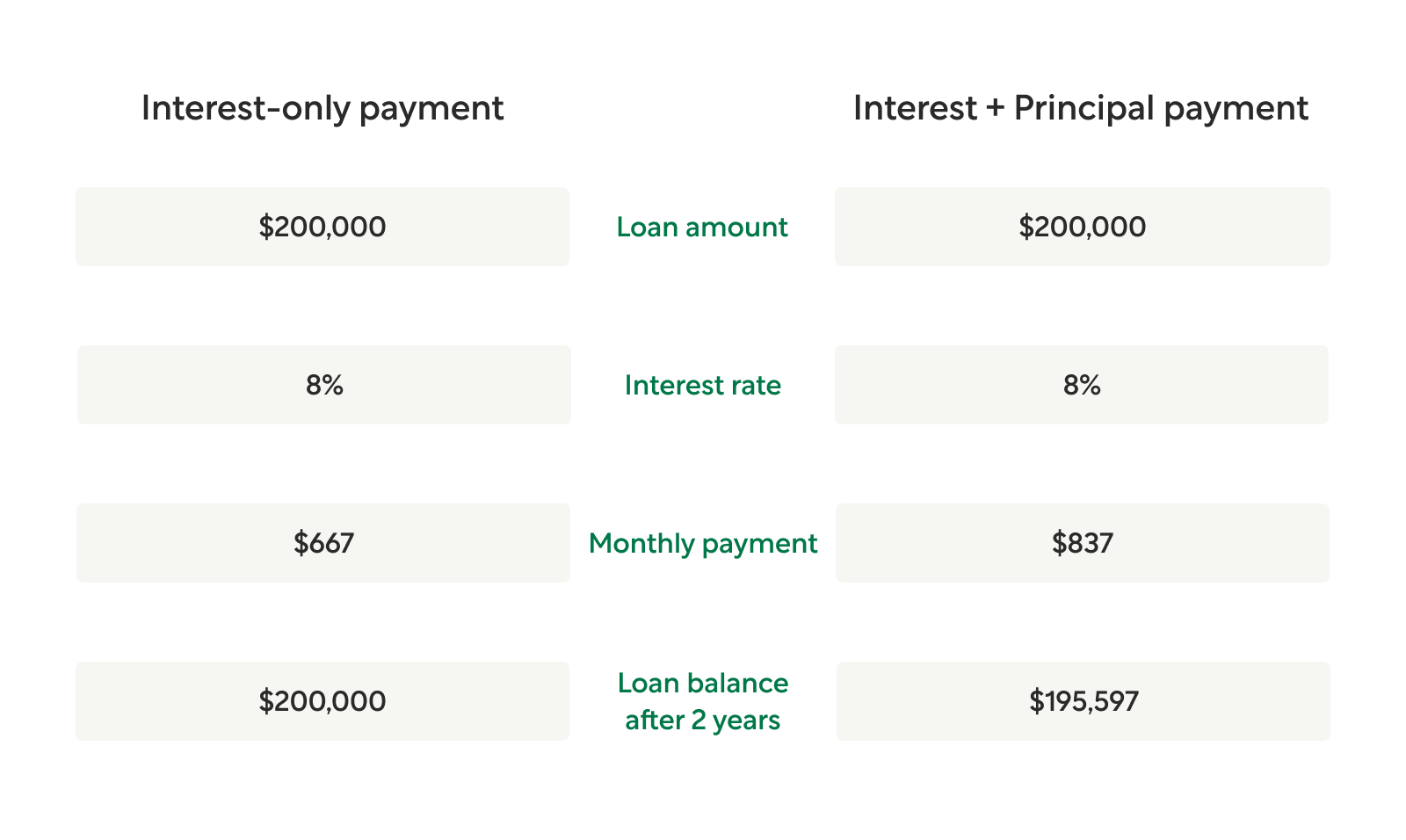

An example

Let’s say you have a HELOC for $200,000 at a 7% interest rate (while most HELOCs have a variable rate, we’re using a fixed rate for example purposes). The draw period is 10 years, and the repayment period is 15 years.

If you withdraw $200,000 during the draw period, you would make interest-only payments of $667 per month, and during the repayment period, your interest plus principal payments would be $837 per month — a difference of $170 each month (or an increase of 25.5%).

This is why it’s important to estimate your payments beforehand and plan ahead to make sure you have the funds to repay. To better understand your potential repayment terms, use Better’s HELOC calculator.

Quickly learn how much equity you can borrow from your home and what your projected monthly payments might be.

....in as little as 3 minutes – no credit impact

HELOC prepayment penalties

If you get a HELOC with some lenders, paying it off early could cost you extra. The loan agreement may include a clause that requires you to pay a HELOC prepayment penalty for early loan repayment. That’s because the lender misses out on the interest you pay when you fulfill the whole agreement.

Depending on your loan terms, you could have fees during your draw period, repayment period, or both. These could include:

—Percentage-based fee: Lenders typically charge a variable rate based on your outstanding loan balance as a prepayment charge.

—Flat fee: Instead of a percentage-based fee, some lenders charge a flat fee for early prepayment.

—Early closure fee: This is an early termination fee for paying your loan off in the first few years of the repayment period.

—Reimbursement of closing costs: Your lender may ask you to repay closing costs if they originally waived these fees.

—Tiered penalties: These fees decrease over time, dropping from, say, 4% in the first year to 2% in the third year after opening the loan.

Unlike many HELOC lenders, Better doesn’t charge any prepayment penalties for paying off your loan early, giving you more flexibility and potentially saving you money.

....in as little as 3 minutes – no credit impact

How to pay off your HELOC

There are several things you can do to reduce your HELOC balance and ultimately pay your debt off on time. Here are a few of your options:

Refinancing

—Refinance your current HELOC: If you can get a lower rate today, it may be advantageous to pay off your current HELOC by refinancing to a new one. You could save money and settle your debt sooner.

—Take out a home equity loan: You could also switch from a HELOC to a home equity loan with a shorter repayment term. The monthly payments may be higher, but you might pay off your debt faster. You’ll also lock in a fixed interest rate, giving you predictable monthly payments that can make budgeting easier.

—Cash out refinance: With a cash out refinance, you can tap into your home’s equity to pay off the HELOC, reduce other debts, and decrease your overall monthly interest payments. This could be a good option if you want to switch from a variable-rate mortgage to a fixed-rate mortgage.

Alternative payment strategies

—Renegotiate your loan: Ask your lender to adjust your loan terms. Not all will, but it’s worth trying to make your payments more manageable.

—Increase your income: Boost your income with a side hustle or by selling possessions you no longer use. Then, use that extra cash to pay off the loan faster.

Frequently asked questions

How does paying back a HELOC work?

The first stage of paying off a HELOC is the draw period, where you only pay interest. After that, you reach the repayment period, during which time you pay both interest and the principal balance.

Can you pay off a HELOC during the draw period?

During the draw period, you only pay interest, not the original loan amount. You can’t pay off the whole loan during the draw period.

How long do you have to pay back a HELOC?

Your lender sets the repayment terms in your loan agreement. The draw period on most HELOCs is around 10 years, while the HELOC repayment period is around 20 years.

Navigate your HELOC journey with confidence

Now that you understand how HELOC payments work, you can make an empowered, informed decision about tapping your home’s equity when you need cash. But paying back a HELOC requires planning and discipline, especially when you move from the draw period to repayment with higher monthly payments.

Looking for a better option? With Better, there are no prepayment penalties, so you can pay off your loan whenever you want. We also offer clear terms, useful tools, and 24/7 customer support without the hidden fees and long waits you’re used to with traditional lenders.

Check out Better today and apply for a HELOC in minutes.

....in as little as 3 minutes – no credit impact