If you have a mortgage, chances are you’ve seen a statement from your lender, either by mail or online. But what’s a mortgage statement, exactly?Your mortgage statement is a detailed snapshot of your loan activity, showing where your money is going and how your loan is progressing. Below, you’ll learn everything a typical mortgage statement includes and how to use yours to budget effectively and make sound financial decisions.

What’s a mortgage statement?

A mortgage statement is a document that gives you an up-to-date summary of your mortgage loan. It outlines the key details of your loan, including your current balance, monthly mortgage payment amount, and how that payment is allocated across principal, interest, escrow, and fees.

These documents are similar in format to a closing disclosure, but instead of outlining your closing costs, they track your progress once the loan is in motion. And you’ll typically receive them once a month.

If you’re wondering how to get a mortgage statement, the answer is simple: Mortgage servicers are legally required to send them every billing cycle. Depending on your lender, you may get them by mail, electronically, or both. Either way, it’s worth reviewing each one carefully, even if you’re on autopay.

A mortgage statement is different from a mortgage interest statement (also known as Form 1098), which you receive annually for tax purposes. The mortgage statement focuses on your current billing cycle, while a mortgage interest statement totals the interest you’ve paid throughout the year.

What does a mortgage statement look like?

While the layout can vary slightly from lender to lender, mortgage statements generally follow a similar format. You’ll see a breakdown of what you owe, what you’ve paid, and key dates like your due date and loan maturity date. The idea is to give you a clear picture of your financial status without having to dig through a slew of documents or bank statements.

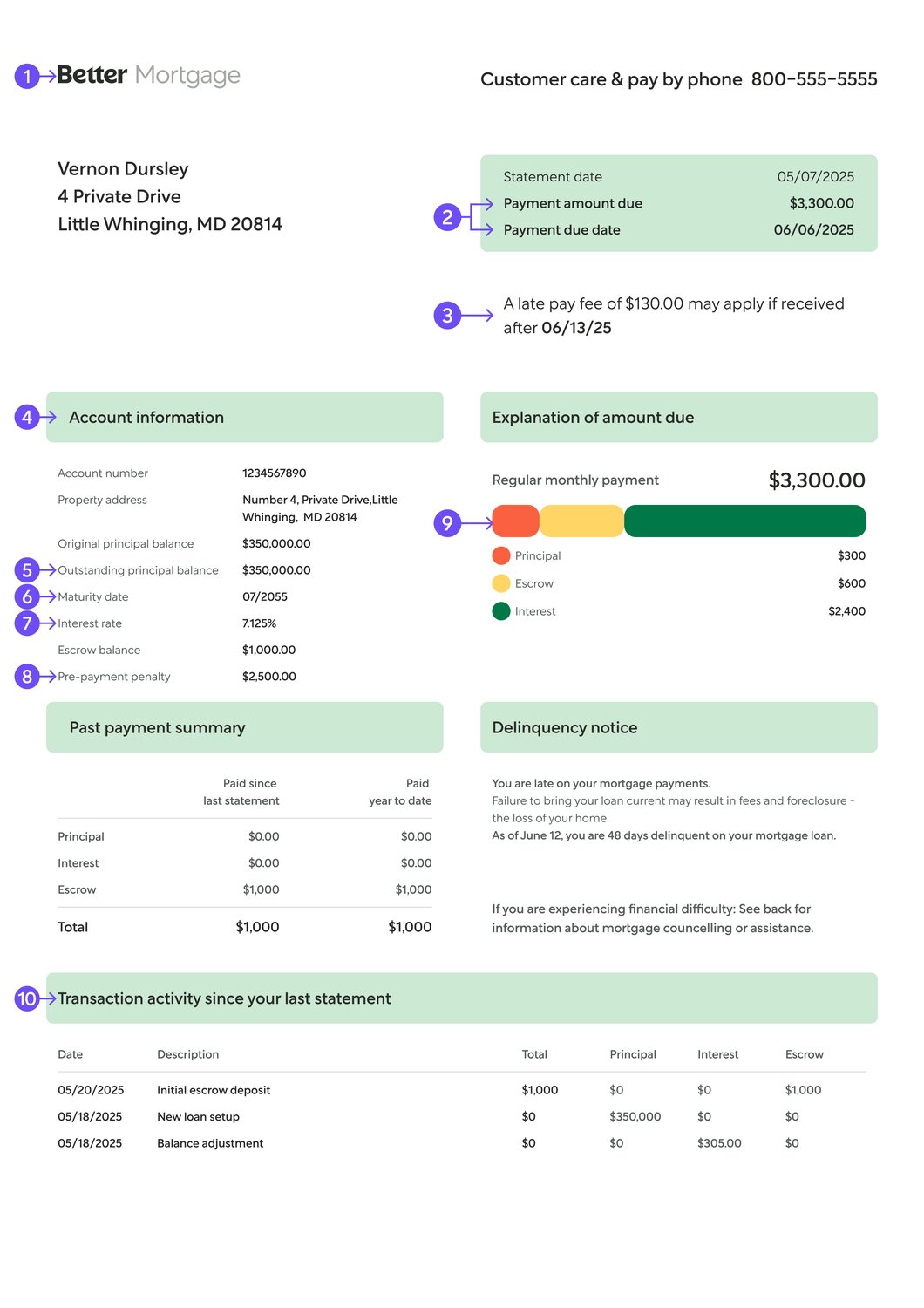

Here’s a mortgage statement example to help you understand how everything comes together:

What’s on a mortgage statement? 10 key components

Every mortgage loan statement is packed with useful information. Here are the core details.

1. Servicer information

Your mortgage servicer is the company managing your loan, although this might not be the same lender you closed with. The statement will list your servicer’s name and contact info so you can reach out with questions about payments, billing, or your escrow account.

2. Account information

Each loan has a unique account number assigned by your mortgage lender. Keep this handy if you need to call or email your servicer — it helps them quickly pull up your file.

3. Payment due date and amount due

This section shows your next monthly payment and when it’s due. Most mortgage payments are due on the first of the month, with a grace period before late fees kick in. That grace period is usually around 15 days, but check your statement for specifics.

4. Late payment date

If you miss your due date, you may see a note that includes the “if paid after” amount, which adds on the applicable late fee. While your credit report likely won’t show a late payment until it’s 30 days past due, your lender may charge fees sooner.

5. Remaining principal

Your outstanding principal balance is the amount you still owe on the loan, not including interest. Each payment received chips away at this number. If you make extra payments toward your principal, you can pay off your mortgage faster and save on interest.

6. Maturity date

This is when your loan is scheduled to be fully paid off. At the start, this reflects what that date will be if you only make the required monthly mortgage payments. If you’re making extra payments, the maturity date will arrive sooner, and that date will be reflected on your statement.

7. Interest rate

This shows the current interest rate on your mortgage. If you have a fixed-rate loan, it won’t change. But if you have an adjustable-rate mortgage, keep a close eye on this in case you want to refinance. Lenders are required to notify you of upcoming rate changes, but your statement is a good place to track them too.

8. Prepayment penalty

Most standard mortgage loans no longer include prepayment penalties, but if you have a nontraditional loan, a fee may apply if you pay off your mortgage early. Your statement should flag this clearly if it’s relevant.

9. Payment breakdown

This is a detailed breakdown of your monthly mortgage payment. It shows how much is going toward the principal, how much is going toward interest, and how much is set aside in your escrow account for property taxes and insurance. Any late fees will be listed here as well.

10. Transaction history

This section shows how your lender applied last month’s payment. You’ll see the split between principal, interest, and escrow, along with any fees or additional transactions like refunds or partial payments.

Other mortgage statement details you should know

Beyond the basics, here are a few additional details that might show up on your mortgage statement:

— Escrow balance: If your lender manages an escrow account, this section shows how much is currently available to cover upcoming bills. Not all lenders list your escrow balance on every statement, but you should receive a separate escrow analysis at least once a year.

— Delinquency notices: If your mortgage payment is 45 days late or more, your statement may include a delinquency notice. These notices outline outstanding amounts, fees, and steps to get you back on track. Multiple delinquency notices in your payment history can affect your ability to refinance later.

— Borrower resources: Some lenders include a section with additional support options, especially if you’re having trouble making payments. This might include links to housing counselors or instructions for requesting mortgage assistance.

Making the most of your mortgage statement

Understanding your mortgage statement helps you stay organized, avoid late fees, and plan your next move. Here’s how to make it work for you.

Review your statement for accuracy

It’s a good idea to glance through your statement every month to make sure everything looks right. That includes your escrow balance, payment due dates, and how your payment was applied. Mistakes happen, and catching them early can prevent unnecessary stress.

Keep copies of your statements

While you don’t need to keep every last monthly statement forever, it’s smart to hold onto your annual mortgage statements for at least three years, especially if you’re self-employed or need documentation for your taxes. Having a record of your mortgage loan activity can also come in handy if you decide to refinance.

Make your mortgage payment online

Most borrowers pay online, and for good reason. It’s fast, easy, and you can set up autopay to stay on track. If your lender offers a payment portal, you can link your bank account, view your escrow account details, and check your payment history all in one place.

Some lenders still issue coupon books instead of monthly mortgage statements. These work like old-school checkbooks, with detachable slips for each payment. If you’re using one, make sure to track payments separately because these slips include limited information.

Of course, you can still mail a check. Just send it early to avoid any issues with your due date.

From making your first payment to tracking your loan every step of the way, Better makes managing your mortgage a breeze. Check your homebuying budget in as little as three minutes with Better’s online pre-approval.

...in as little as 3 minutes – no credit impact

Take the next step with Better

Keeping an eye on your mortgage statement is an easy way to stay informed and in control as a homeowner. Each statement gives you a clear view of where you stand and where you’re headed.

Better makes mortgage management simple with a streamlined digital platform and competitive loan terms. With no hidden fees and an application process that takes as little as three minutes, you could get up to $500,000 and receive your funds in as little as seven days.

Still have questions? Try our AI assistant, Betsy, to get instant answers.

Start your mortgage journey on the right foot with Better.

...in as little as 3 minutes – no credit impact