What You’ll Learn

How to understand your Closing Disclosure form

Why your Closing Disclosure may vary from your Loan Estimate

The significance of different dates on your Closing Disclosure

It’s the last document you’ll receive before you close on your home—and it’s also one of the most important. We’re here to answer some of the most commonly asked questions about Closing Disclosures.

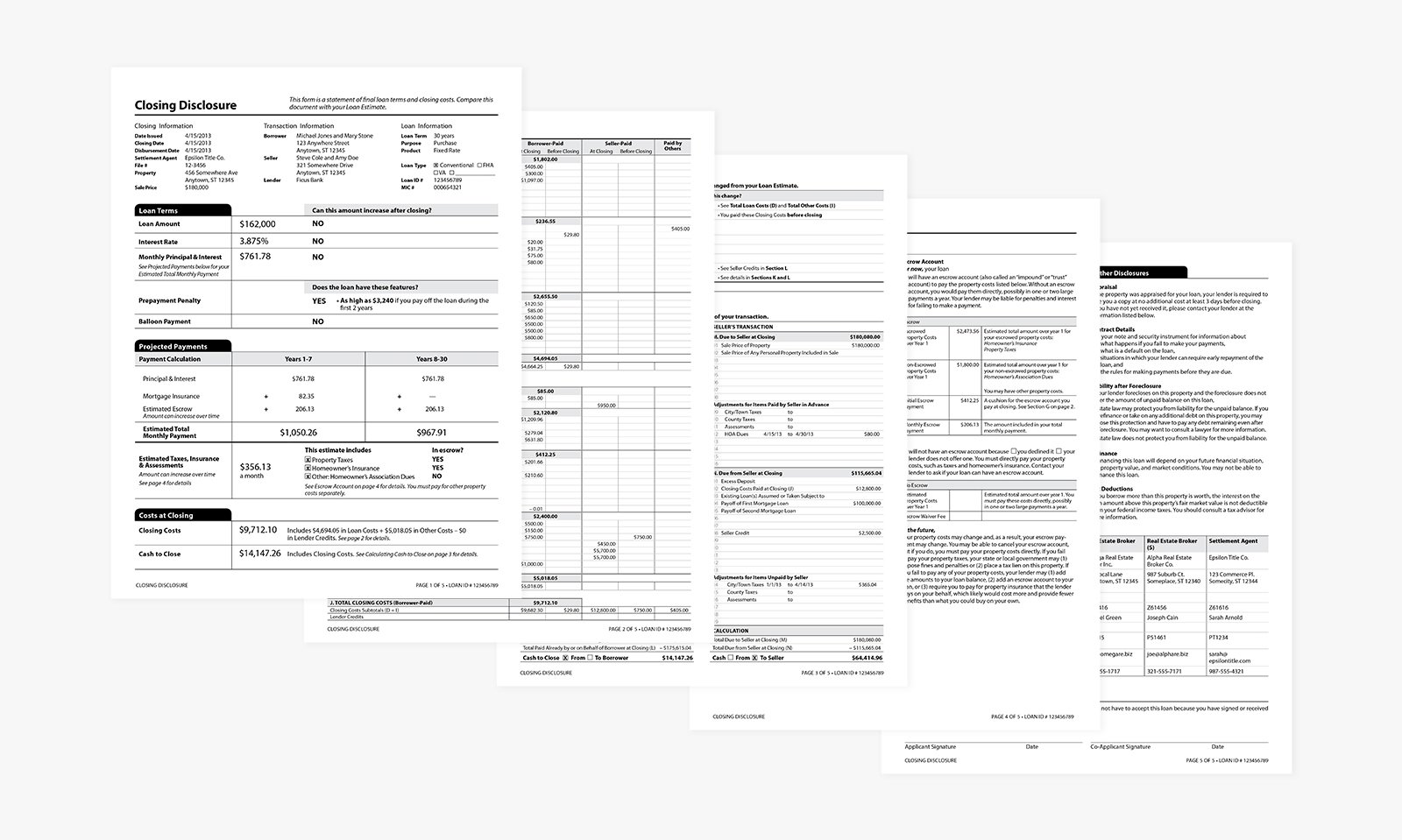

What is a Closing Disclosure?

This document is the final bill of sale on your home loan and closing costs. It shows you the full cost of the home loan you’ve chosen—including the terms, projected monthly payments, fees, and cash to close. A simple way to think about your Closing Disclosure is that your Loan Estimate tells you what you might pay, while a Closing Disclosure tells you what you will pay.

For illustrative purposes only.

You’ll want to compare your Closing Disclosure to your Loan Estimate to see if there are any discrepancies. Luckily, the Consumer Finance Protection Bureau (CFPB) requires lenders to provide your initial Closing Disclosure at least 3 business days before you close. The CFPB also requires that this document be standardized, itemized, and easy to read—there’s even a section that will show you exactly what has changed between receiving your Loan Estimate and receiving your Closing Disclosure. If you have any questions or final changes you’d like to make, you can use the 3-day grace period to call your lender and have those made. No adjustment is too small— even if your lender misspells your name or printed a typo on your address, you’ll want to have that corrected before closing. They’ll send you a revised Closing Disclosure, which you should check again. Then you’ll receive your final Closing Disclosure, which you’ll sign as part of the closing process.

It’s important to know that there are three revisions that can trigger a new three day grace period:

i. If your loan terms change after receiving your initial Closing Disclosure and APR increases more than 1/8th of a percent. That’s why it’s important to lock in your rate and make any changes prior to entering closing.

ii. If your lender decides to add a prepayment penalty to your terms. These are growing increasingly uncommon, but you should still keep an eye out for it.

iii. If you decided to go with a different loan product. This is essentially like “going back to start” and requires a bit of a backtrack.

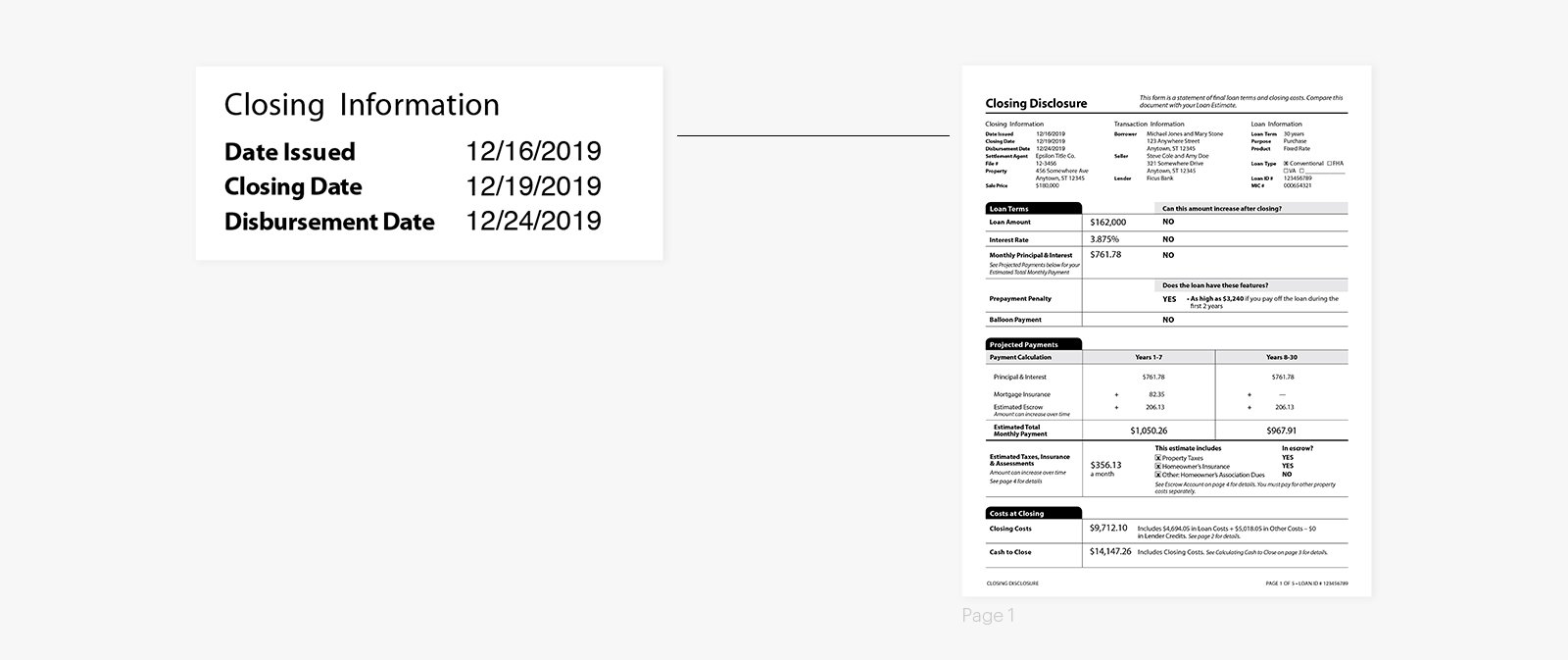

What are the key dates on my initial Closing Disclosure?

For illustrative purposes only.

Date issued: Sounds pretty self explanatory—this is the date the initial Closing Disclosure is provided to you. But there’s a bit of a catch—your “date issued” is assumed to be the “date received.” Pro tip: you should acknowledge your initial Closing Disclosure on your Better Mortgage account on the same date that you receive it in order to move into the rest of the closing process as soon as possible.

Closing date: If you're purchasing a new home, this date will be the same as your "Close of Escrow." However, in Alaska, Arizona, California, Hawaii, Idaho, Nevada, New Mexico, Oregon, and Washington, you are generally allowed to sign your closing documents prior to this date. If you’re refinancing your home, there’s no need for a transfer of ownership, and there are far fewer parties involved. 3 business days after you receive and acknowledge your initial disclosure, you’ll be ready and expected to sign your final Closing Disclosure.

Disbursement date: This date is important for two reasons.

First: this is the date your loan will fund—which is generally the same day the title company will “disburse” your transaction. That’s a lender term for “paying all the people you promised to pay.”—including the seller, appraisers, cash-back payments for yourself, and more. If you're buying a home, your disbursement date is considered your "close of escrow" date. On the other hand, for primary refinances, your disbursement date is the day after your recission period ends—or 4 days after you've signed your closing package. For refinances of second homes or investment properties, this date is 2-3 days after you've signed the closing package.

Second: your disbursement date is also the date your loan begins to accrue interest. You can see all the details of your prepaid interest in section F of your Closing Disclosure.

What to Check on Your Closing Disclosure

When you receive your Closing Disclosure, it's essential to thoroughly review each section to ensure all the details are correct. Here's a checklist of key details to verify:

Spelling of your name: Confirm that your name is spelled correctly. Any discrepancies can cause issues later on, especially during the title transfer process

Loan term: Check the length of your loan term. It should match what was agreed upon with your lender.

Loan amount: Verify the total loan amount. It should match the amount stated in your Loan Estimate.

Interest rate: Confirm the interest rate on the Closing Disclosure. It should match the rate you locked in with your lender.

Monthly principal and interest: Review your monthly payment amount, including both the principal and the interest. Make sure this amount is within your budget and as expected.

Closing costs: Check the total closing costs. These costs should be very close to the estimate provided earlier in the Loan Estimate.

Cash to close: This is the total amount you'll need to bring to closing, including your down payment and any remaining closing costs. Make sure this amount is correct and that you're prepared to pay it at closing.

If you find any discrepancies or have any questions about the details in your Closing Disclosure, contact your lender immediately.

What to Do if You Find Discrepancies in your Closing Disclosure

If you find a discrepancy between your Loan Estimate and your Closing Disclosure, it's essential to address it right away. Here are the steps you should take:

Contact your lender: Reach out to your lender immediately if you notice any discrepancies. These could be minor, like a spelling mistake, or major, like a difference in the loan amount or interest rate.

Review the changes: Ask your lender to explain any changes. Some changes are normal, but your lender should be able to justify and explain each one.

Request xorrections: If there are errors, request that your lender correct them. This might delay the closing process, but it's essential to ensure that all the details are correct.

Review Revised Closing Disclosure: Once the corrections have been made, your lender will provide a revised Closing Disclosure. Review it carefully to ensure all the changes have been made correctly.Delay closing if necessary: If there are significant errors, it may be necessary to delay closing until they're corrected. It's better to delay closing than to proceed with inaccurate information.

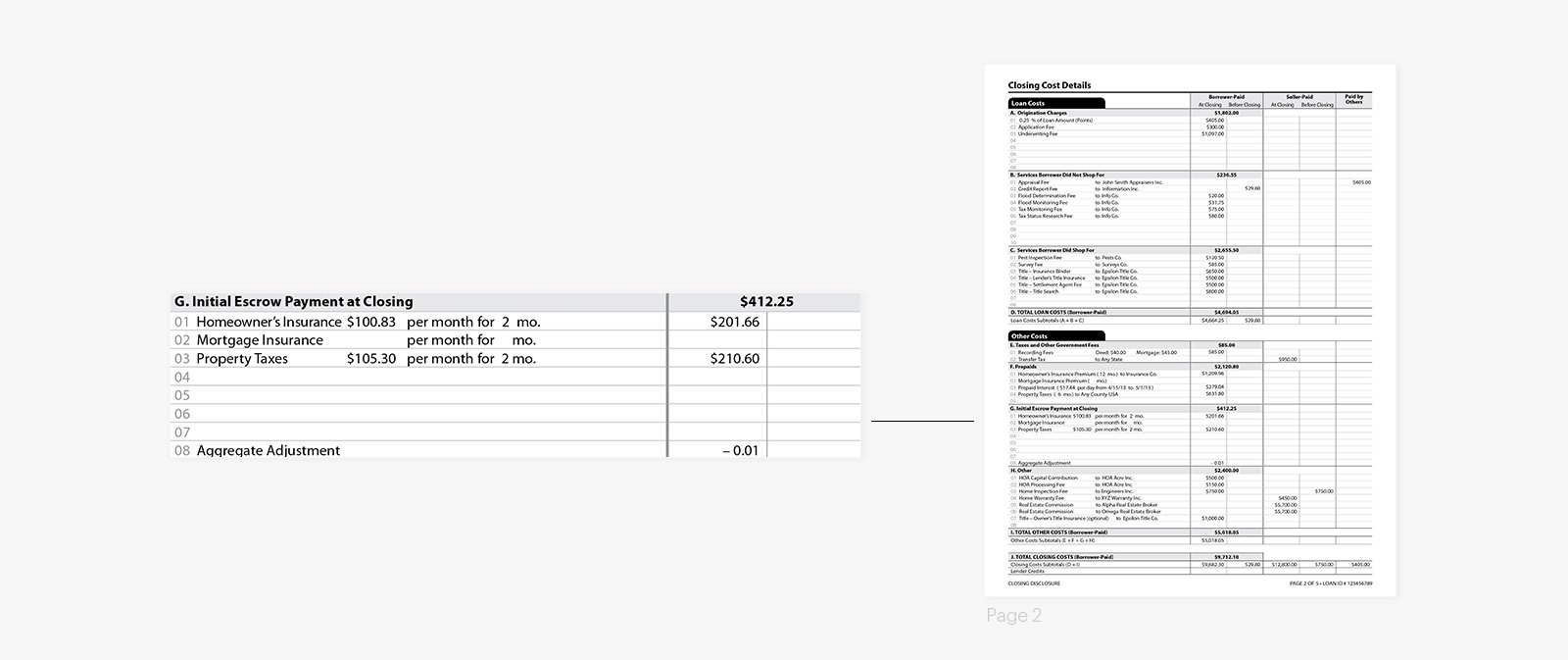

What are escrow accounts and aggregate adjustments?

Escrow accounts, also known as impound accounts, are set up by your lender and are used to hold the money you'll pay for property-related expenses (i.e. property taxes and homeowner's insurance).

Your escrow deposits are outlined in Section G of your Closing Disclosure. If your closing is moved from one month into the next (closer to the due dates for future installments), you will see your escrow deposits increase by one month.

For illustrative purposes only.

We generally include a 2-month buffer for taxes and insurance (although, in some states it's less—check with your Closer to confirm).

Another item you’ll see in section G is the “aggregate adjustment,” which refers to any credits your lender may need to return to you. By law, lenders can’t hold more than ⅙ of your annual tax and insurance payment in escrow. If you pay more than that amount into escrow, your lender will “adjust” that amount, and credit you back the difference.

Why are you collecting property taxes and/or homeowners insurance as a prepaid?

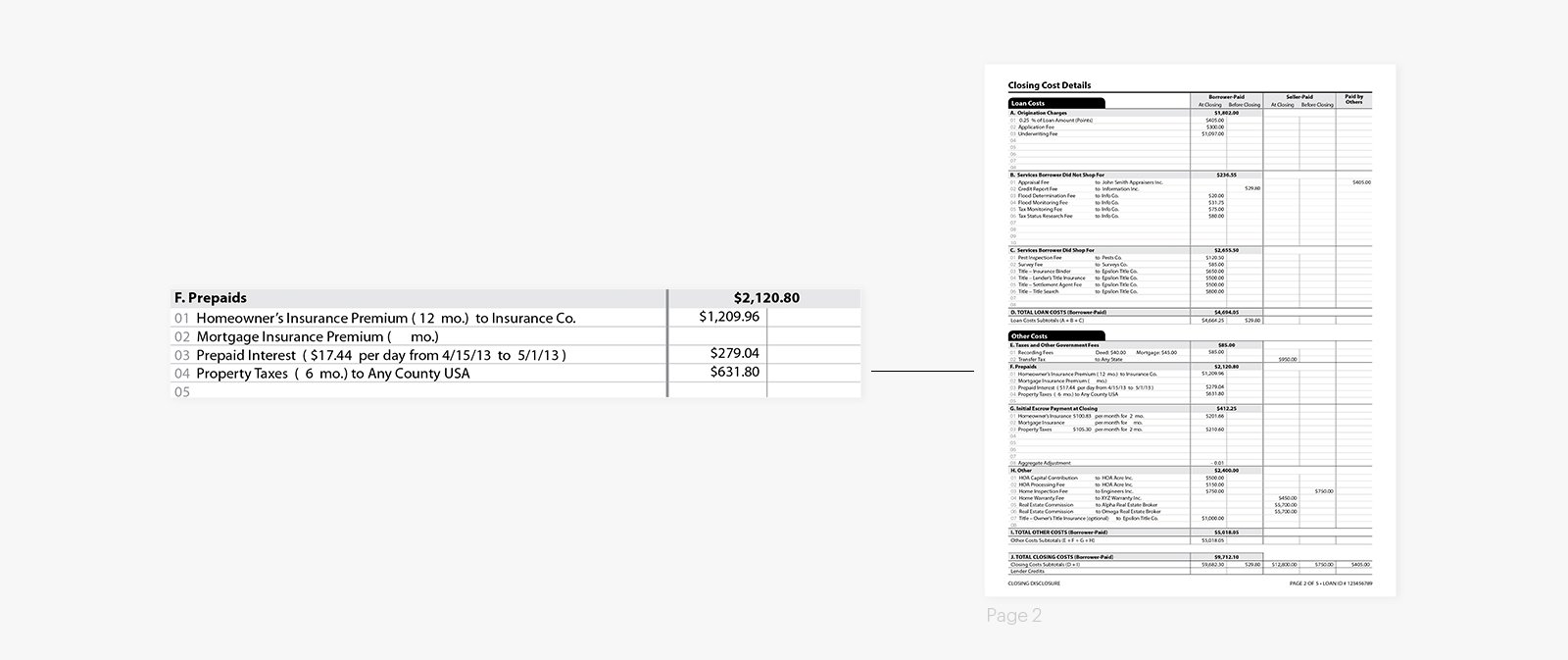

If property taxes are due and payable (generally if they are due within 60 days of closing or due in the same month as your first mortgage payment), they either need to be paid through your new mortgage as a prepaid charge, or paid outside of closing (with proof of payment provided). These costs are referred to as prepaids and you will see them in Section F of your Closing Disclosure.

For illustrative purposes only.

Lenders need to ensure your homeowners insurance premium is going to be paid. If you have waived your escrow account and are on a month-to-month plan for paying your homeowners insurance, we will likely collect at least 3 months of homeowners insurance payments on your Closing Disclosure to ensure your policy is paid through your first mortgage payment.

If you’re refinancing and the policy for your homeowners insurance or your upcoming tax installment is being paid by funds from an existing escrow account, we can generally use that as sufficient proof to remove the prepaid charges from your Closing Disclosure.

What happens to the money in my original escrow account?

During a refinance, you’ll be asked to put down a deposit for your new escrow account with your new lender. It takes up to 30 days after closing on your refinance to get the money back from the original escrow account. By law, lenders have 30 days to disperse the funds from the time that the loan is paid off and the account is closed.

How is my payoff calculated? (For refinance transactions only)

The payoff to your current lender includes your outstanding principal balance (this is typically the figure you'll see on your current lender's website, which doesn't include other fees), interest due, miscellaneous fees, and an interest buffer of at least seven days to ensure the payoff isn't short. Sometimes there’s a gap in processing between the time the payoff is sent to your current lender and when they actually process and apply those funds to your outstanding balance.

My spouse is not on the loan and I don’t want them liable for this loan. Why are they listed as a borrower?

Any person on the title (depending on state and local laws) is required to sign the Closing Disclosure. Although this person may be listed as “borrower” on the Closing Disclosure, this does not mean they are financially responsible for the loan. The only people financially responsible are those listed on the promissory note itself. If your spouse is not on title, they may still be required to sign some documents depending on the laws in your state.

Closing comes up more quickly than you’d think. It’s good to know what to expect before you get there. This is still very much an active part of the home loan process. Ask questions, review carefully, but also know you have a great team behind you in Better Mortgage.

If you have any other questions about your Closing Disclosure or the closing process, you can reach out to your Closer directly by logging into your account.