A recent announcement from President Donald Trump has put mortgage rates back in the spotlight - and a lot of people are already drawing comparisons to the COVID-era when mortgage rates dropped to record lows.

The question that's got people talking is really pretty simple: will this actually bring mortgage rates down - and if so, how much?

The short answer is: probably not as much as they did during the pandemic — at least not right away. But understanding why this moment still matters requires separating rate mechanics from market psychology.

Why this announcement matters — beyond mortgage rates

While most of the headlines focus on whether this move could push mortgage rates lower, some industry leaders think the more interesting impact may be on homeowner behavior - not rates themselves.

As first highlighted by market analysts at The Kobeissi Letter*, the real significance of renewed policy attention on housing may be who is now positioned to respond to even modest rate changes. According to the data they cite, the number of homeowners with mortgage rates above 6% has nearly surpassed those holding ultra-low sub-3% pandemic rates.

That shift matters. It suggests the housing market is no longer dominated by “golden handcuffs” alone, but by a growing group of homeowners who are closer to being economically mobile. For these 6%+ borrowers, even a small rate decline, potentially sparked by a one-off bid to purchase mortgage-backed securities, could meaningfully change the math on selling, buying again, or refinancing.

This means the bigger behavioral unlock may not come from convincing 2–3% homeowners to move, but from activating a newer cohort of homeowners who bought more recently, at higher rates, and are already closer to their breaking point. For them, rate stabilization - or simply the perception of policy support - could be enough to bring sidelined housing stock back to market.

In other words, this moment isn’t necessarily about recreating pandemic-era mortgage rates. It’s about lowering the threshold at which today’s higher-rate homeowners feel comfortable moving again, and that could have an outsized impact on inventory.

That context matters, because small shifts in borrower psychology — especially among the 6%+ cohort — can ripple through the housing market in ways that raw rate movements alone don’t explain.

What exactly was announced?

At the heart of this announcement is a proposed $200 billion purchase of mortgage-backed securities (MBS) - which is basically bundles of home loans that investors buy. If there's a strong demand for these securities, mortgage rates often drop slightly - which is the idea behind this new plan.

Now, some of this might sound a little familiar - because a similar mechanism played a key role during the COVID pandemic. However that's really where the similarities end.

If this is all a bit new to you - a quick run-through of what determines mortgage rates would be a helpful starting point.

...in as little as 3 minutes – no credit impact

What happened during the COVID era - and why did it have such a big impact on mortgage rates?

When the economy suddenly shut down in 2020, there was a real risk that lending could freeze. Banks didn’t know how deep the recession would be, investors pulled back, and borrowing could have become much more expensive — or harder to access at all.

To prevent that, the Federal Reserve stepped in.

Instead of focusing only on short-term interest rates, the Fed targeted the mortgage market directly by buying huge amounts of mortgage-backed securities — the bonds that most home loans are packaged into and sold to investors.

Over roughly two years, the Fed bought about $1.3 trillion of these mortgage bonds. At one point, it owned nearly 30% of the entire mortgage bond market.

That scale is what made the difference.

Why did buying mortgage bonds push rates so low?

Think of it like this: Mortgage-backed securities are essentially the “product” behind mortgage rates. When lots of investors want them, lenders can offer lower rates. When investors pull back, rates go up.

During COVID, the Fed became the buyer of last resort — and then some.

By stepping in so aggressively, the Fed:

- Created constant demand for mortgage bonds

- Pushed bond prices higher

- Which automatically pushed mortgage rates lower

At the same time, the Fed took on a lot of risk that private investors didn’t want to touch during a crisis. That helped calm the market, reduce volatility, and keep mortgage lending flowing even while the broader economy was under stress.

The result was something we’d never really seen before: mortgage rates falling extremely fast, and staying unusually low. In some cases, 30-year rates dipped below 3%.

Why this matters now

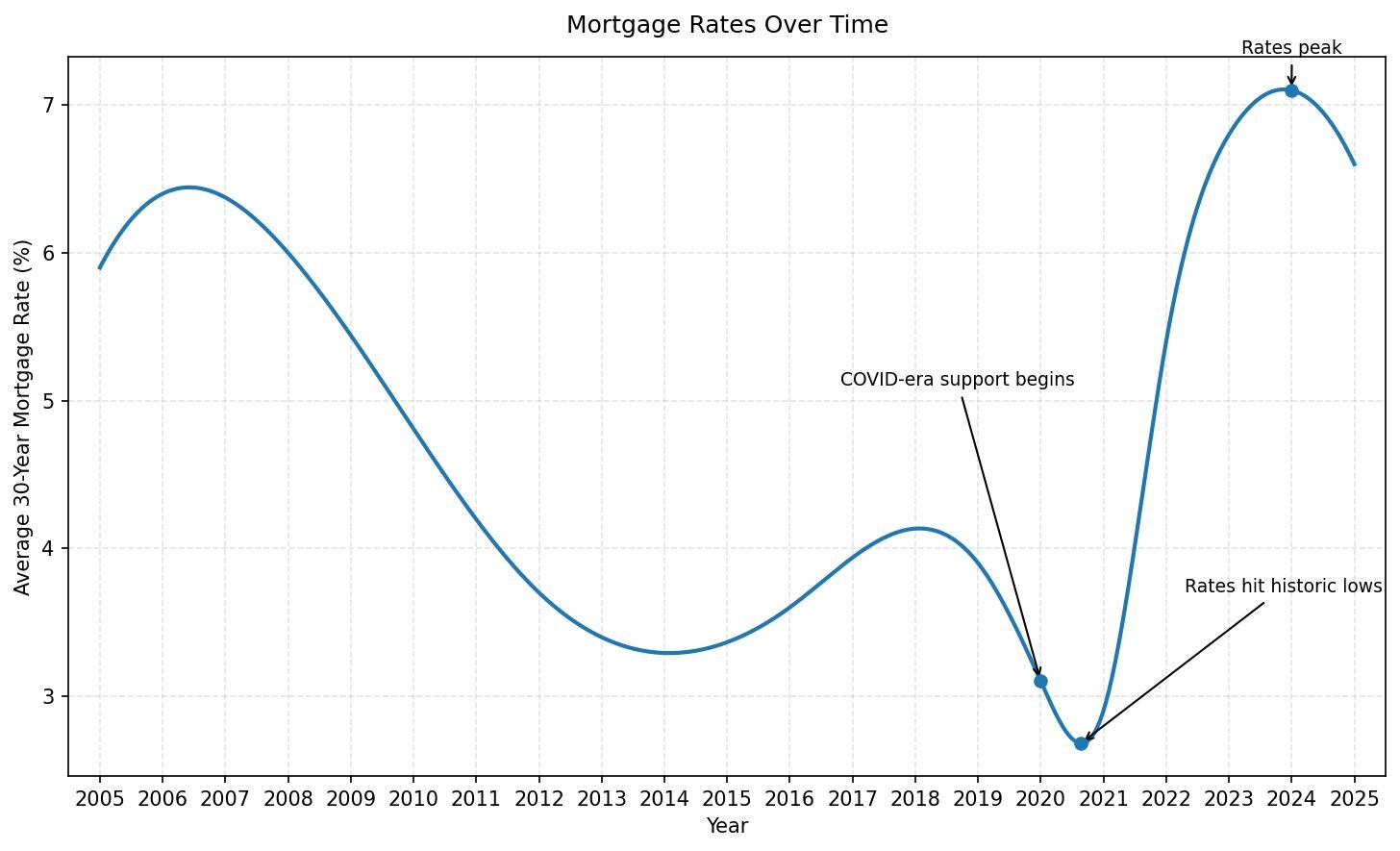

To understand just how unusual that moment was, it helps to zoom out.

The chart below shows mortgage rates over a longer period of time. Compared to the gradual ups and downs we normally see, the COVID-era drop stands out as sudden and extreme.

As you can see, the drop in mortgage rates during COVID was both sharp and unusual - and driven by policy tools that aren’t in play today.

As the chart shows, rates didn’t just drift lower during COVID; they collapsed due to emergency policies designed for a once-in-a-generation crisis.

Those same tools, scale, and conditions simply aren’t in place today. That’s why comparing today’s housing announcements to the COVID era requires a lot of context - not just about rates, but about how long frozen homeowner behavior may finally begin to thaw.

What makes Trump's new plan different than COVID?

While $200 billion is still a big number - context matters.

1. Who is buying

When the Fed was buying MBS back in the pandemic, it was because it had all the money and the ability to take on the risk. Donald Trump making a public announcement isn't quite the same - at least not unless it's backed up by some serious Fed action.

2. The scale is much smaller

During the COVID pandemic the Fed was buying MBS worth $1.3 trillion - this new proposal is closer to $200 billion. In today's market that $200 billion amount barely covers a month or two of new mortgage issuance - so it's unlikely to have a huge impact on rates.

3. It's not a long-term commitment

During the pandemic markets really thought the Fed was committed to keeping buying MBS - and that expectation kept rates low for what felt like an eternity. A one-off deal like the one Trump is proposing on the other hand tends to have a much shorter-lived effect if inflation or treasury yields move higher in the meantime.

So what does Trump's announcement really mean for mortgage rates?

In all reality, most experts think this will have a modest impact - but it won't be anything like the big changes that happened during the pandemic.

During the pandemic, the Fed's actions actually lowered mortgage rates by more than a full percentage point, and kept them low for nearly two years.

If you're tracking rates on a daily basis, check out Better's mortgage rate page to get a clear idea of just how small changes show up in real time.

What does Trump's announcement mean for homebuyers?

For homebuyers, even modest shifts in rates can have a meaningful impact on affordability. Following the announcement, mortgage rates moved down roughly 0.05% to 0.15%. Not a dramatic swing, but enough to change the math for many buyers.

Part of that movement comes from a slightly tighter mortgage-backed securities (MBS) spread. In simple terms, mortgage rates are influenced by how investors price the risk of mortgage loans relative to safer assets like Treasury bonds. When that spread tightens, lenders can offer slightly lower rates without changing the underlying economic fundamentals. But it’s a market-driven adjustment, not a guarantee of a longer-term trend.

Even so, small rate changes matter. A fraction of a percentage point can reduce monthly payments, increase buying power, and improve the long-term cost of owning a home, especially when paired with the right loan structure. Over time, those differences can add up to real savings.

That said, moves like this can fade unless they’re reinforced by broader economic signals, such as sustained inflation cooling or clearer guidance from the Fed. And waiting for confirmation can come with tradeoffs.

Markets often move before anything is set in stone, and when rates fall—even slightly—more buyers tend to re-enter the market. Increased demand can quickly lead to tighter competition and higher home prices, offsetting some of the benefit of a lower rate.

For many buyers, the bigger risk isn’t locking in a rate that isn’t the absolute bottom. It’s delaying a purchase that already works financially, only to face higher prices or fewer options later. In that context, buying when the numbers make sense today—while keeping the flexibility to refinance if rates fall further—can be a more practical approach than trying to time the market perfectly.

If you’re actively shopping, running a few scenarios can help bring clarity. Tools like Better’s mortgage calculator allow you to see how different rate paths affect monthly payments, buying power, and long-term costs, so you can make decisions based on real numbers, not short-term market noise.

...in as little as 3 minutes – no credit impact

What does Trump's announcement mean for homeowners?

If you already own a home, headlines like this might naturally make you wonder whether it’s time to revisit refinancing. That’s a reasonable question, but it’s important to keep expectations grounded.

This isn’t a return to the pandemic-era refinance boom, when rates fell fast and millions of homeowners rushed to lock in historic lows. Today’s rate environment is very different, and even if mortgage rates ease slightly, the changes are likely to be incremental, not dramatic.

That said, refinancing doesn’t require a massive rate drop to make sense.

For some homeowners, even a small improvement in rate can still deliver meaningful benefits, especially if it helps:

- Lower monthly payments

- Reduce long-term interest costs

- Eliminate mortgage insurance

- Align the mortgage with longer-term financial goals

Whether refinancing is worth it depends on a few key factors, including your remaining loan balance, how long you plan to stay in the home, and what you’re hoping to accomplish, not just today’s headline rate.

Tools like Better’s refinance guide can help you quickly see how different rate scenarios might affect your monthly payment and total interest over time, without any pressure to commit.

The bottom line: while this announcement alone probably won’t transform the refinance market overnight, it may create opportunities at the margins. And for homeowners who stay informed and prepared, those smaller windows can still be worth paying attention to.

...in as little as 3 minutes – no credit impact

The bottom line

This news is a bit reminiscent of the times when mortgage rates just kept plummeting and stayed low for ages. But that was a whole different ball game - and the market's changed a lot since then.

A $200bn MBS purchase might provide a bit of short-term support to rates - but its got nothing on the scale compared to when the market was in record-low territory during COVID.

As a borrower, it's best practice to not try to time the market. Instead, you'll gain greater impact by understanding how rates work, what your options are, and being ready to make a move when the numbers make sense for you.

If you want to get a sense of your homebuying power today, or a custom rate for a refinance, you can do so with Better's pre-approval.

...in as little as 3 minutes – no credit impact