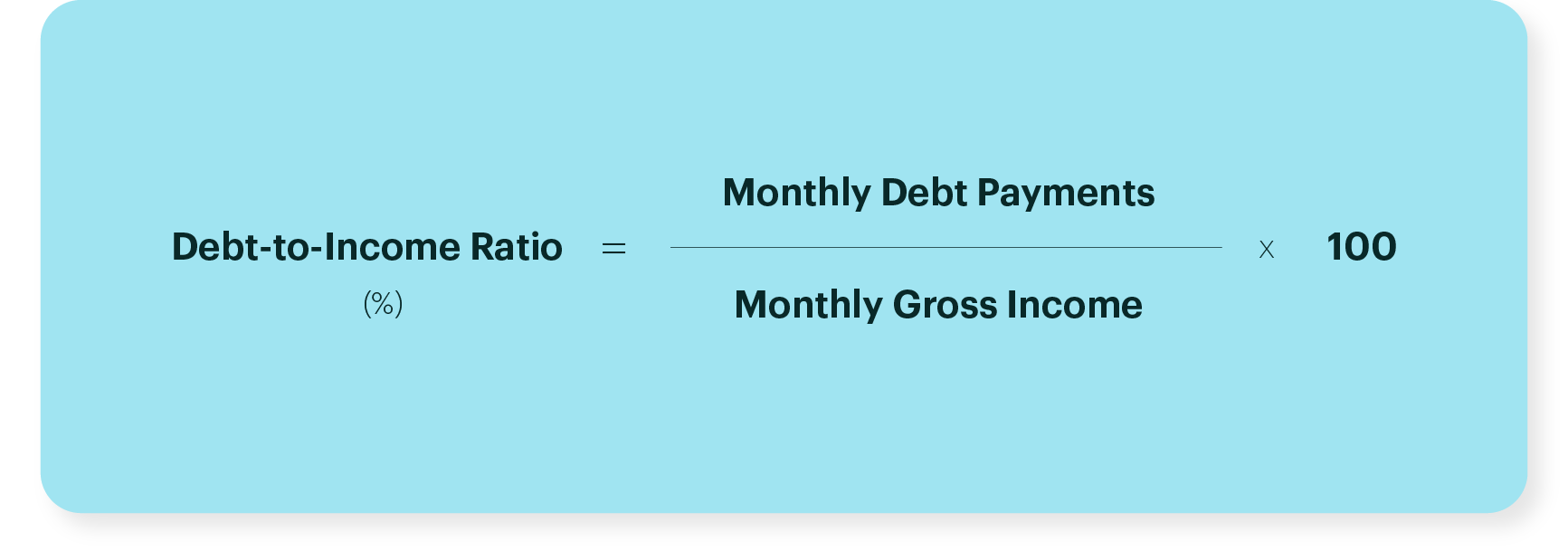

When I talk to customers about getting a mortgage, they’re often concerned about their credit score, which is an indicator of their ability to pay back loans and can affect the rates they’ll be able to get. While credit scores are certainly important, what they often don’t know is that another number, debt-to-income ratio (DTI), can play an even bigger role in their ability to get a mortgage. In fact, a high DTI is the #1 reason mortgage applications get rejected1. So what's a DTI, exactly? Your debt-to-income ratio is all your monthly debt payments divided by your gross monthly income. I’ll get into the specifics of this calculation next.

Most lenders typically offer loans to creditworthy borrowers with DTIs as high as 43-47%. That limit is based on policies by government-backed lenders like Fannie Mae, put in place to protect customers against predatory lending practices. As of July 29th, 2017, we are working with Fannie Mae to offer loans with DTIs of up to 50% for creditworthy borrowers2. However, the lower your DTI, the more financing options will be available to you. Let’s look at what goes into calculating that number.

How to calculate the debt to income ratio

On the one hand, the math for [calculating your DTI](https://better.com/content/housing-expense-ratio) is simple – we add up what your monthly debt will be once you have your new home (such as student loans, car loans, credit card bills, and your future mortgage payment) and divide it by your gross monthly income (how much money you earn before taxes).

The tricky part about calculating DTI is that there can be several moving parts.

For example:

- If you haven’t found your new home yet, we won’t know your exact mortgage payments, property taxes, or insurance payments, so we’ll have to estimate.

- If you already own a home, we’ll need to include both your future and current mortgage payments as debt (unless the purchase of your new home is contingent on the sale of your old home).

In addition, when we calculate income (the other half of the DTI equation), we use conservative calculations because we want to make sure you get a mortgage that’s affordable, now and in the future.

For example:

- If you’re self-employed or compensated by commission or RSUs, we may not be able to count all 100% of that income, given that these forms of income tend to be less consistent.

- If you are self-employed, it’s typically beneficial to write off your business expenses to lower your tax bill. But those tax deductions may also lower your qualifying income, since underwriters are looking at your net (not gross) income.

- If you have rental income from an investment property, we’ll need to see that income on your tax returns (or rental checks if your taxes haven’t been filed yet) and we’ll only be able to use a portion of that income to be conservative.

- If you plan on turning your current home into a rental property, you’ll need to have a lease agreement in place for us to consider the potential income.

We can help give you clarity about your DTI

At Better Mortgage, our goal is to give you as much certainty as we can, as soon as we can, about how much you’ll be able to get financing for.

When you get our 3-minute pre approval, we run a soft credit check (which doesn’t affect your score). This allows Mortgage Experts like me to look at your debts and credit in more detail and get a more accurate picture of your DTI.

If you’re planning on buying soon, we also encourage you to upgrade to our verified pre-approval. Our underwriting team will review things like your tax returns, pay stubs, and any other documents specific to your financial situation, so we can tell you exactly how much you are qualified to borrow. This helps ensure there aren’t surprises about your DTI when you do apply for a mortgage.

Tips to consider for lowering your DTI

[Lowering your DTI](https://better.com/content/what-percentage-of-income-should-go-to-mortgage) can have a big impact on the type of [financing you can get](https://better.com/content/how-to-qualify-for-a-mortgage). If you have some flexibility on when you plan on buying, taking time to lower your DTI (and improve your credit score) can save you a lot of money over the life of your loan.

A few DTI reduction strategies to consider:

- If possible, pay off your car loan before applying for your mortgage.

- If you plan on purchasing a car, considering waiting until after you’ve bought your home.

- Start paying off your credit cards in full, one by one. (Don't close the cards after you pay them off, as this can hurt your credit score.)

- If possible, refinance or consolidate current loans to reduce your monthly payments.

- Consider adding a co-borrower with a low DTI to your loan (keep in mind that if they have a low credit score, it could negatively affect your financing options).

- If you plan on using rental income, make sure you have lease agreements in place.

- If you plan on living with a partner, parent, or roommate in your new home, talk to us about how we might include some of that income in your DTI calculation.

Ready to explore your options?

We can help you understand your DTI and the financing options available to you. Start by getting your 3-minute pre approval. Then schedule a call so we go over the numbers with you.

https://www.housingwire.com/articles/40382-fannie-mae-raises-debt-to-income-ratio-to-further-expand-mortgage-lending ↩