Even with an online lender, a mortgage pre-approval requires turning in a lot of paperwork. First-time homebuyers often feel overwhelmed by the documents lenders ask for.

Learning, in advance, what documents you'll need makes the pre-approval process faster and easier. Instead of pausing the application to go find documents, you can keep the process moving toward its goal: your preapproval letter.

The preapproval letter shows your home buying budget. It also shows Realtors and sellers that you're a serious and capable buyer.

Smart checklist: Documents you need for mortgage pre-approval

So, what documents will you need to get preapproved?

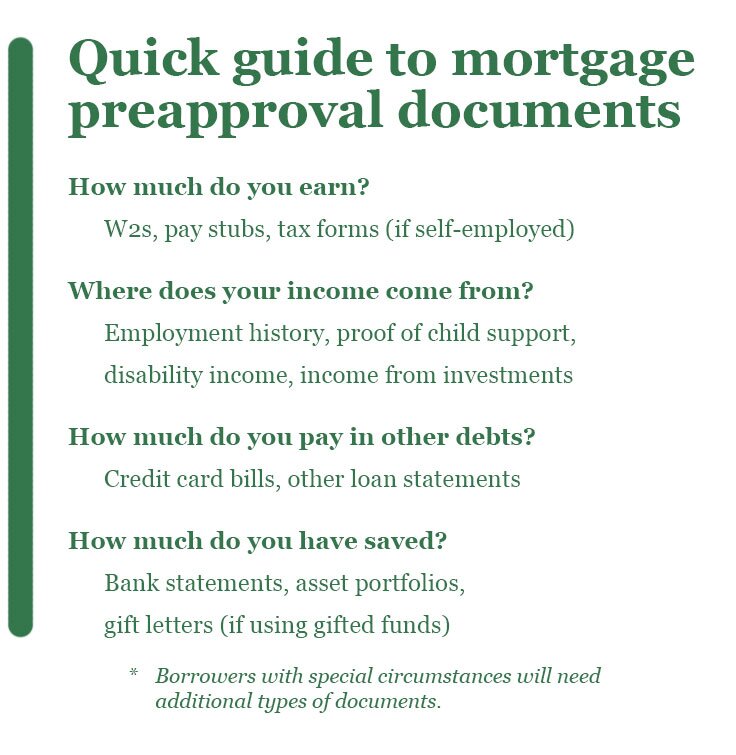

Proof of income (pay stubs, W-2s, tax returns)

You'll need your last 30 days of pay stubs, W-2 forms from the past two years, and federal tax returns covering the previous two years. These papers help lenders see how stable your income is and track your earnings growth.

Why this matters: Lenders need solid proof of what you earn so they can find out how much you could afford to spend on housing.

...in as little as 3 minutes – no credit impact

Employment verification

Your pay stubs tell only part of the story. Lenders will ask for your current employer's contact details to confirm your position, salary, and how long you've worked there. Job changes in the last two years need explanation, so keep your previous employers' information handy.

Why this matters: A stable work history means your current income should continue into the future. Future income shows whether you'll be in a position to make monthly mortgage payments.

Credit report and credit score

Lenders will check your credit report and credit score, so there's no need to upload your own copy. But knowing your own credit score will help you set realistic expectations.

Most conventional loans need at least a 620 FICO score, though some government-backed loans, especially FHA loans, can go as low as 580. Your chances of getting better interest rates improve with a higher score.

Why this matters: Your credit history reflects your financial habits. Higher credit scores usually belong to borrowers who keep debts up to date.

Bank statements and assets

Lenders need to see two to three months of statements from all your financial accounts: checking, savings, retirement, and investments. These statements show your overall financial health.

Why this matters: Bank statements show whether you can afford the loan's down payment and closing costs. Also, a borrower with a healthy savings account can afford to make a few mortgage payments even if struck by an unexpected expense or loss of income.

Debt and monthly obligations

Lenders need to know about all your other monthly debts, including credit card accounts, personal loans, student loans, auto loans, and other mortgage debt.

Why this matters: Income spent on other loan payments can't also be spent on a mortgage payment. Debt documentation helps show lenders how much money you could spend on a mortgage each month.

Government-issued photo ID

You'll need to upload a valid driver's license, passport, or other government ID to verify your identity throughout the mortgage process.

Why this matters: Lenders need to make sure you're applying in your own name and with your own Social Security number.

Rental history (if applicable)

First-time homebuyers may need to show proof of their rental history.

Why this matters: Making 12 consecutive months of on-time rent payments shows you can handle monthly house payments.

Gift letters for down payment (if applicable)

Is someone helping make your down payment? They may need to submit a letter confirming the money is a gift and not a loan. The letter must clearly state the donor doesn't expect repayment.

Why this matters: If down payment help must be repaid, it will affect the borrower's monthly debt payments.

...in as little as 3 minutes – no credit impact

More about why lenders need these documents

When combined, all this documentation says a lot about your financial health, financial habits, and financial future.

The documents also show your risk as a borrower. You're asking to borrow a significant sum of money: hundreds of thousands of dollars or more. The lender needs to know whether you're able and likely to repay the money.

Lenders use documentation to measure borrower risk through:

Debt-to-income ratio (DTI)

Your debt-to-income (DTI) ratio is a key metric for mortgage borrowing. This number shows how much of your income goes toward debt each month.

- If you earn $8,000 a month and spend $2,000 a month on debt payments, your DTI would be 25 percent. (That's a very good DTI, by the way.)

- If you earn $4,000 a month and spend $2,000 a month on debt payments, your DTI would be 50 percent. (That's too high for most mortgage lenders.)

Ideally, DTI should be 43 percent or lower for FHA loans and 36 percent or lower for conventional loans.

How lenders calculate DTI: The pay stubs, tax returns, and debt documentation you provide give lenders the numbers they need to measure DTI.

To verify you can repay the loan

Federal law requires mortgage lenders to find out whether borrowers can repay their loans. This law is designed to keep lenders and borrowers away from risky loans.

Your employment history and income documents show your earning ability. Bank statements show how well you can save and manage money. These records tell your financial story and help lenders predict whether you'll make your mortgage payments on time.

To determine your loan eligibility

Lenders use all this financial data to help decide which type of mortgage loan you should use. Different loan types (conventional, FHA, VA, USDA) come with different rules about credit scores, down payments, and income.

Using the right kind of mortgage can lead to a lower interest rate and lower monthly payments. This, in turn, lowers DTI and helps with loan qualification.

Additional documents needed in special circumstances

Some borrowers need more documents to show lenders their full financial picture.

Expect a few extra steps if:

You already own a home

Mortgages work a little differently when you're not buying a primary residence. If you already own a home, you may need to provide homeowners insurance and property tax documents. You may also need to file paperwork proving you plan to sell the home and use the new home as a primary residence.

You're self employed

Self-employed borrowers don't usually have W2s and pay stubs to show their income. Instead, they'll need to provide:

- Personal and/or business tax returns from the last two to three years

- Year-to-date profit and loss statements for the current year

- Balance sheets for your business

- Bank statements showing business deposits

- A letter from your accountant confirming business stability

Lenders usually want at least two years of self-employment history to call this income stable enough for mortgage qualification.

You receive child support and alimony

Child support or alimony payments affect your debt-to-income ratio. You must show divorce decrees, separation agreements, and court orders with payment details.

To use this income for mortgage qualifying, you'll need bank statements showing you've received consistent payments for at least six months. You'll also need proof that payments will continue for at least three years after your mortgage starts.

You earn disability and other forms of income

Disability insurance, Social Security, or pension income can be used to qualify for a mortgage, but lenders will need to see award letters from the issuing agencies. Specifically, lenders need to know whether the income will continue for at least three more years.

Qualifying with income from investments will require showing recent statements showing your dividend or interest payments.

You're a veteran using a VA home loan

Veterans should have their Certificate of Eligibility (COE) documents ready for VA loans. The COE allows veterans and active duty service members to apply for VA loans; it doesn't ensure the loan will be approved. Veterans still have to qualify with income, debt, and employment history.

FAQs about mortgage preapproval

How can I improve my chances of getting preapproved?

Do your own credit check and improve your credit score before applying. Even a 20-point increase could help qualify for a better rate. Fortunately, improving your credit score can also improve other parts of your loan file. For example, paying down credit card balances can improve your credit score and your debt-to-income ratio (DTI).

Does mortgage preapproval affect my credit?

Modern lenders like Better Mortgage do soft credit checks for mortgage preapproval. Soft credit checks don't hurt the borrower's credit score. Some lenders still do hard credit checks. Hard inquiries could drop your score temporarily.

How long does preapproval take?

Different lenders have different timelines. Online lenders might approve you the same day, while traditional banks need three to five business days. For some borrowers, Better Mortgage can turn around a preapproval in as little as three minutes. Collecting all the required documents in advance will speed up the process.

Most lenders respond within 72 hours once you submit all documents. Your preapproval letter usually stays valid for 60 to 90 days after they issue it.

Is mortgage prequalification the same as getting preapproved?

No. Mortgage pre qualification doesn't usually require full documentation. It's an estimate based on unverified data. Prequalification can still be useful, but it doesn't reflect the borrower's true mortgage eligibility.

Shop with confidence with a mortgage preapproval in hand

The volume of documents needed for a mortgage preapproval overwhelms a lot of new home buyers. But this upfront work can pay off when it's time to submit a formal mortgage application.

Plus, preapproval gives buyers and sellers confidence in their ability to close a mortgage loan.

With its online preapproval process, Better Mortgage does its best to make getting preapproved faster and easier for borrowers.

...in as little as 3 minutes – no credit impact