The 2026 conforming loan limit is increasing by 3.26%, giving homebuyers more room to borrow with conventional financing. For single-family homes, the new baseline limit is $832,750, up from $806,500 in 2025—an increase of $26,250 that can significantly expand buying power without moving into a jumbo loan.

Conforming loan limits are the maximum loan amounts that most lenders treat as standard. Loans that fall within these limits are typically easier to qualify for and come with lower interest rates and more flexible down payment options than non-conforming loans.

The exact conventional loan limit for 2026 depends on where you’re buying and the type of property. High-cost areas and multi-unit properties have higher limits, allowing buyers to borrow more while still staying within conventional guidelines.

For many buyers, these updated loan limits could make the difference between stretching uncomfortably—or qualifying confidently for the home they want, whether it’s a first home, a move-up purchase, or an investment property.

What is a conforming loan and why conforming loan limits matter for homebuyers

A conforming loan serves as the foundation of mortgage options in today's market. These mortgages meet the dollar limits set by the Federal Housing Finance Agency(FHFA) and follow the funding criteria that FreddieMac and FannieMae require.

How Fannie Mae and Freddie Mac define conforming loans

Congress created FannieMae (Federal National Mortgage Association) and FreddieMac (Federal Home Loan Mortgage Corporation) to support the mortgage market. These organizations don't give out mortgages themselves — they buy eligible loans from lenders and package them into mortgage-backed securities to sell to investors. This creates more liquidity in the mortgage market so lenders can issue more loans.

These entities help keep the housing market stable by setting standard rules and guidelines for mortgages. Loans that meet their criteria become "conforming loans" — ready to trade in the secondary market.

Conforming vs. jumbo loans: key differences in rates, down payments, and credit

The loan amount creates the main difference between conforming and non-conforming loans.The FHFA sets these limits each year — most areas had a baseline limit of$806,500 for single-family homes in 2025. Loans above these limits become "jumbo loans".

Jumbo loans come with:

- Interest rates that run 1-2 percentage points higher

- Credit requirements that need 700+ scores versus 620 for conforming loans

- Down payments starting at 10% compared to as low as 3% for conforming loans

- Stricter debt-to-income ratio limits

Benefits of conforming loans for homebuyers andfirst-time buyers

Conforming loans are a smart choice for many homebuyers. These loans typically have lower interest rates than non-conforming options because they're less risky for lenders. Buyers can get started with down payments as low as 3% of the purchase price.

The approval standards are also more flexible with conforming loans. Borrowers need a credit score of just 620 and can have debt-to-income ratios up to 45%(sometimes 50% for refinances). Better Mortgage can go up to a 50% DTI for conforming loans.

Borrowers with excellent credit will find these loans among the most economical financing options in today's market.

...in as little as 3 minutes – no credit impact

How the FHFA sets conforming loan limits each year

The Federal Housing Finance Agency (FHFA) reviews national housing data each year —this helps them set the conforming loan limits for the upcoming year.The process follows guidelines that are 15 years old under the Housing andEconomic Recovery Act of 2008 (HERA).

How home price trends influence annual conforming loan limits

FHFA has a specific way to calculate conforming loan limits based on house price movements. The agency announces updated conforming loan limit values at the end of November — these new values start working from January 1st of the following year. They used the FHFA House Price Index® (FHFA HPI) to track average U.S. home value changes over four quarters, then looked at nominal, seasonally adjusted, expanded-data FHFA HPI between the third quarters of 2024 and 2025 toset 2026 limits.

Why conforming loan limits increase or stayflat each year

The housing market's reality directly affects conforming loan limits. Home prices went up by 3.26% between the third quarters of 2024 and 2025 — this meant the baseline conforming loan limit for 2026 increased by the same percentage. The formula works differently when home prices fall. HERA rules say the baseline loan limit stays the same during market downturns. The market needs to make up any previous drops before the baseline limit can rise again.

Why conforming loan limits help maintain access to affordable financing

These yearly updates to conforming loan limits serve a clear purpose — they make conventional home financing fair and accessible to more people as marketschange. Homebuyers can keep up with rising property values this way. Some areas have higher costs — places where 115% of the local median home value tops the baseline limit get higher limits. These can go up to 150% of the baseline amount. FHFA balances standards with flexibility. This lets the conforming loan program adapt to different regional housing costs while keeping nationwide underwriting standards consistent.

2026 conforming loan limits by location and property type

The Federal Housing Finance Agency (FHFA) has announced the 2026 conforming loan limits for mortgages that Fannie Mae and Freddie Mac can purchase. These new limits reflect how home values have continued to rise in the last year across the United States.

Baseline vs. high-cost area conforming loan limits in 2026

Most areas of the country will have a standard baseline conforming loan limit of $832,750for single-family homes. Higher limits apply to designated high-cost areas where 115% of the local median home value exceeds this baseline. The ceilingreaches $1,249,125 — which equals 150% of the baseline limit.

Alaska,Hawaii, Guam, and the U.S. Virgin Islands have different loan limits due to special statutory provisions. Single-family properties in these areas will have baseline and ceiling limits of $1,249,125 and $1,873,675respectively.

2026 vs. 2025 conforming loan limits: how much more buyers can borrow

The new limits show a 3.26% increase from 2025 — this increase matches the rise in average U.S. home prices between the third quarters of 2024 and 2025, based on FHFA's seasonally adjusted, expanded-data Home Price Index.

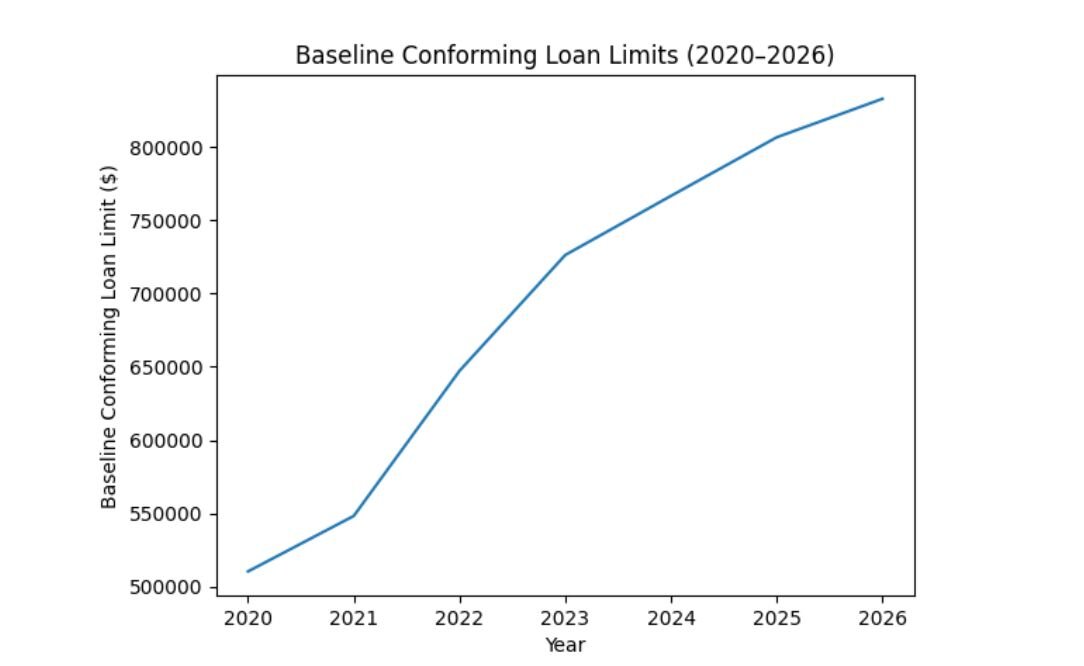

While the 2026 conforming loan limit increase is smaller than the sharp jumps seen in recent years, it continues a multi-year trend tied closely to rising home prices. The chart below shows how conforming loan limits have increased since 2020 — highlighting how conventional loan borrowing power has expanded over time as the housing market has changed.

How conforming loan limits have increased since 2020

In just six years, the baseline conforming loan limit has increased by $322,350,reflecting how rising home prices have steadily expanded the amount buyers can borrow while still qualifying for conventional financing.

Conforming loan limits by property type (1–4 units)

The conforming loan limits vary based on property units:

- 2-unit properties**: $1,066,250 (baseline) / $1,599,375 (high-cost areas)

- 3-unit properties**: $1,288,800 (baseline) / $1,933,200 (high-cost areas)

- 4-unit properties**: $1,601,750 (baseline) / $2,402,625 (high-cost areas)

Borrowers can access these new limits for loans delivered to Fannie Mae and Freddie Mac starting January 1, 2026 — regardless of when the loan originated. This change gives borrowers more purchasing power without needing jumbo financing.

What the 2026 conforming loan limits mean for homebuyers

The new conforming loan limits for 2026 offer solid advantages to homebuyers across the country. These changes will determine who can get conventional financing and what choices they have when they need larger loans.

How higher conforming loan limits affect mortgage eligibility

More mortgages will now qualify as conforming instead of jumbo loans — this change gives borrowers better benefits. They can get lower interest rates, more flexible underwriting standards, and smaller down payments (as low as 3%compared to the 10-20% they typically need for jumbo loans).

...in as little as 3 minutes – no credit impact

What to do if your mortgage exceeds the conforming loan limit

Borrowers who need amounts above their county's limit have several choices:

- Jumbo loan options** (which typically require credit scores of at least 700)

- Making larger down payments to keep the loan amount under the limit

- Using piggyback or second-lien strategies to stay within conforming limits

Using conforming loans for second homes and investment properties

Conforming loan programs cover more than primary homes — they include second homes and investment properties. Vacation home buyers should expect tougher requirements — they typically need a minimum 10% down payment and possibly higher credit scores. Investment properties come with stricter rules and might require credit scores of 720 or higher.

How to check your county’s 2026 conforming loan limit

Loan limits vary significantly based on location. You can find your area's specific limit on the FHFA's interactive map of conforming loan limit values. A mortgage lender can also check your county or ZIP code's official limit.

Final takeaway: how 2026 conforming loan limits expand homebuyer options

The 2026 conforming loan limits bring expanded opportunities to homebuyers nationwide.This piece shows how a 3.26% increase pushes the baseline limit to $832,750 forsingle-family homes — giving buyers $26,250 more purchasing power than 2025.Buyers in high-cost areas can now access ceiling limits up to $1,249,125, which reflects the housing market's price variations across the country.

These new limits reshape what many potential homeowners can achieve. First-time buyers get the most benefits from conforming loans through lower interest rates,smaller down payments, and easier credit requirements. Qualifying for a conforming loan instead of a jumbo loan saves thousands over your mortgage's lifetime.

Smart buyers should check their county's specific limits on the FHFA's interactive map. A qualified mortgage professional can then help chart your best course forward. The new limits offer greater flexibility whether you're buying your first home, need more space for a growing family, or want to invest in rental properties.

The 2026 conforming loan changes bring good news to the housing market. Buying a home remains a major financial step — but these higher limits make conventional financing available to more Americans. We'll keep tracking how these changes affect homebuyers and alter the real estate landscape as 2026 approaches.

...in as little as 3 minutes – no credit impact

Not ready to take the leap? Check out today's rates or play with our mortgage calculator to start understanding what you can afford.