What You’ll Learn

Pros and cons of conventional loans

How to qualify for a conventional loan

Why the conventional loan interest rates you’re offered may be different from a friends

What is a conventional loan and why do you need to know

Banks and lenders typically offer conventional loans to borrowers. According to census data, they are the most common type of mortgage in the US. They’re not part of a specific US government program which can make them more challenging to qualify for than government-backed loans, which the federal government insures. FHA loans, VA loans, and USDA loans are examples of government-backed loans.

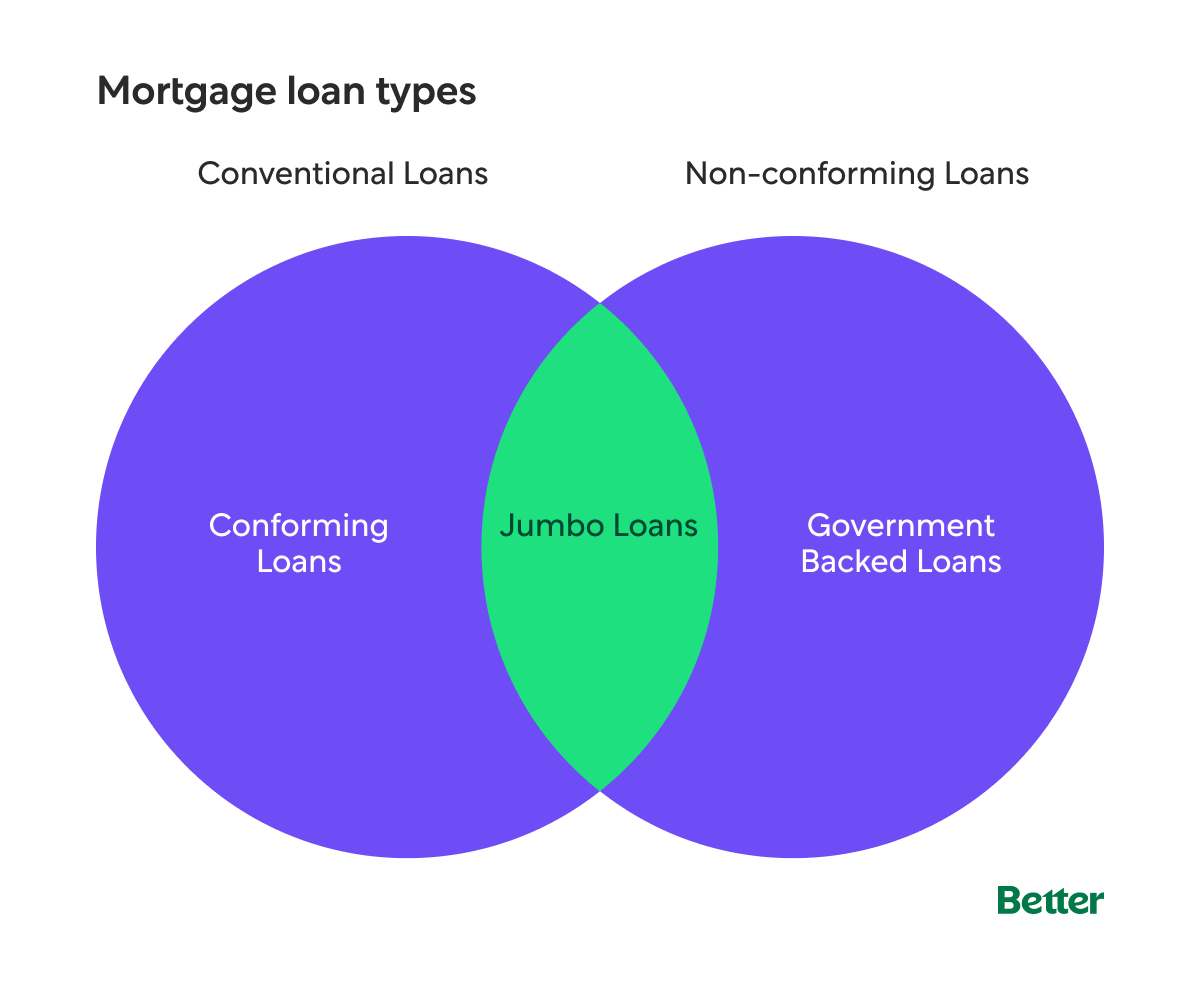

There are 2 categories of conventional loans: conforming and non-conforming. Conforming loans follow lending guidelines set by Fannie Mae and Freddie Mac. Jumbo loans are the only non-conforming conventional loans because they are for amounts higher than the conforming loan limits that Fannie Mae and Freddie Mac set each year. Government-backed loans are also non-conforming loans because, like jumbo loans, they don’t follow Fannie and Freddie’s lending guidelines. In 2022, the conforming loan limit for most areas in the US is $625,000.

Conforming loans typically cost less than FHA loans. So, if you want to explore a wide variety of mortgage options and have a credit score above 620, a conventional loan may be right for you.

How does a conventional loan work

At its most straightforward, a loan is an amount of money you borrow to buy a home. In exchange for lending the money, you agree to pay interest (and fees) to the lender while you pay the loan back over a set period. If you plan to use a conventional loan to help you buy a home, you’ll need to make a down payment. If you’re a first-time homebuyer or haven’t owned property within the last 3 years, you can make a down payment as low as 3%. If you have owned property within the last 3 years, you’ll need to make at least 5% down payment. However, if your down payment is less than 20% you’ll likely need to pay for private mortgage insurance (PMI).

Your bank or lender will show you the interest rate and the types of mortgages you qualify for when you apply for a conventional loan, based on your unique financial situation. Naturally, you would select the mortgage that works with your long-term financial goals and has a monthly mortgage payment that you’re comfortable with.

This mortgage calculator will show you how interest rates, home costs, and down payments affect your monthly mortgage payment.

Pros and cons of conventional loans

Pros: Why you should consider a conventional mortgage

- You have more choices in mortgages Conventional mortgages either come with fixed-interest rates for the full term of the loan, or Adjustable-rate mortgages (ARMs) which have an initial low fixed-interest rate and once the initial period is over, the interest rate will adjust every 6 months. Fixed-interest rate mortgages commonly come with 15-, 20-, and 30-year loan terms. This means your interest rate will remain the same for the length of the mortgage, and you’ll have to pay off the mortgage over the agreed-upon time. Adjustable-rate mortgages (ARMs) have an initial low fixed-interest rate during the introductory period of the loan. Once this introductory period is over, the interest rate will adjust every 6 months.

Fund fact: Your credit score impacts the interest rate lenders will offer you.

- You have more control over mortgage insurance If you have to pay PMI, your PMI payments will automatically stop once your home equity reaches 22%. Home equity is the difference between the amount you owe on a property and the property’s current market value. To save even more on PMI payments, when your home equity reaches 20%, you can ask your lender to remove PMI from your mortgage fees. In contrast, If you get an FHA loan and make a down payment of less than 20%, you would be required to pay a mortgage insurance premium (MIP) for the entire length of your loan.

- You can borrow more money If your credit score is over 700 and you meet the other jumbo loan qualifying criteria, you can borrow up to $1.5M. If your credit score is above 740 and you meet the other jumbo loan qualifying criteria, you can borrow up to $3M.

Cons: Why a conventional mortgage may not be right for you

- Your credit score is below 620. The eligibility requirements for conventional loans are more stringent than government-backed loans. Conforming loans are sold to Fannie Mae or Freddie Mac soon after being created to help keep mortgages affordable for homebuyers. Once a Fannie or Freddie buys a loan, the lender can use the money from the sale to fund more mortgages. While this is for the greater good of all homebuyers, on an individual level, if your credit score is low, you may find it challenging to qualify for a conventional loan.

- You have a high debt-to-income ratio (DTI). Debt-to-income ratio is the difference between your gross monthly income and the total amount you need to pay toward debt each month. If you spent half your monthly income on bills and debt, your DTI would be 50%. Many mortgage lenders will not approve a conventional mortgage for homebuyers with a DTI higher than 43%. On the other hand, FHA loans can be approved for homebuyers with DTIs up to 50%.

Fund Fact: Homebuyers with DTIs up to 50% may also be eligible for a conventional loan with Better Mortgage.

- You have had past bankruptcies and foreclosures. The eligibility criteria for government-backed mortgages are more relaxed. As a result, past bankruptcies and foreclosures are forgiven much faster. Homebuyers with recent bankruptcies or foreclosures which would otherwise be approved may need to wait longer before a lender approves them for a conventional loan. And in some cases, the homebuyer's loan may not be approved at all.

How to qualify for a conventional loan

You’ll typically need to meet the following criteria to be eligible for a conventional loan with Better Mortgage.

| Conventional (conforming) loans* | Jumbo loans* | |

|---|---|---|

| Credit Score | ≥620 | >700 |

| Debt-to-income (DTI) | ≤50% | ≤43% |

| Down payment required | >3% of the purchase price for first-time homebuyers**; ≥5% of the purchase price | >10.01% of the purchase price. (Most jumbo loans require a down payment of at least 20%) |

| Employment history | At least 2 years | At least 2 years |

| Asset reserves | At least enough to cover your down payment and closing costs | Depending on the loan amount, 6–24 months asset reserves |

| Maximum loan amount | $625,000 in most areas | Up to $3M |

*There may be some exceptions to these requirements for certain transactions. A Better Mortgage Home Advisor can give more detailed information tailored to your unique financing needs.

**Homebuyers who haven’t owned a home in 3 years or more, are also able to make a 3% down payment to buy a single family property for their primary residence.

If you’d like a more detailed explanation about conventional loan requirements, read this article.

Explore conventional loan rates from Better Mortgage

Interest rates from all lenders are affected by the economy. The type of property you’re buying, where it’s located, and your unique financial situation also impact the rates lenders offer. This is why you might notice a difference in the rate you’re offered compared to the rate provided to a friend. Often it’s an individual’s credit score that makes the difference. Lenders are more likely to offer a lower interest rate to homebuyers with good credit who want to borrow more money. Another thing lenders take into account is how likely and how soon a borrower will refinance their mortgage.

The most accurate way to know your personalized conventional loan rates is to do a mortgage pre-approval. With Better Mortgage, a pre-approval takes just 3-minutes and won’t impact your credit score.