Student loan payments didn't just restart.They collided with a financial system that wasn't built for abrupt resets.

In 2025, more than 9 million Americans have already missed at least one student loan payment, following the end of the pandemic-era repayment pause. What followed wasn't just late fees or stressful phone calls—it was a widespread credit score shock, with many borrowers seeing drops of 100 points or more almost overnight.

For homeowners and families who co-signed student loans, the consequences are showing up fast—and often in unexpected places.

How student loan delinquencies are impacting credit scores in 2025

For years, student loan payments were effectively frozen. Then, within a short window, millions of borrowers were expected to absorb a new monthly bill—at a time when housing, food, insurance,and childcare costs were already elevated.

The result was immediate. Delinquencies surged, and credit scores fell just as quickly, knocking many prime credit score profiles into subprime.

Data from federal agencies and credit bureaus shows that previously prime borrowers are now slipping into subprime territory, not because of reckless borrowing, but because missed student loan payments hit credit reports all at once.

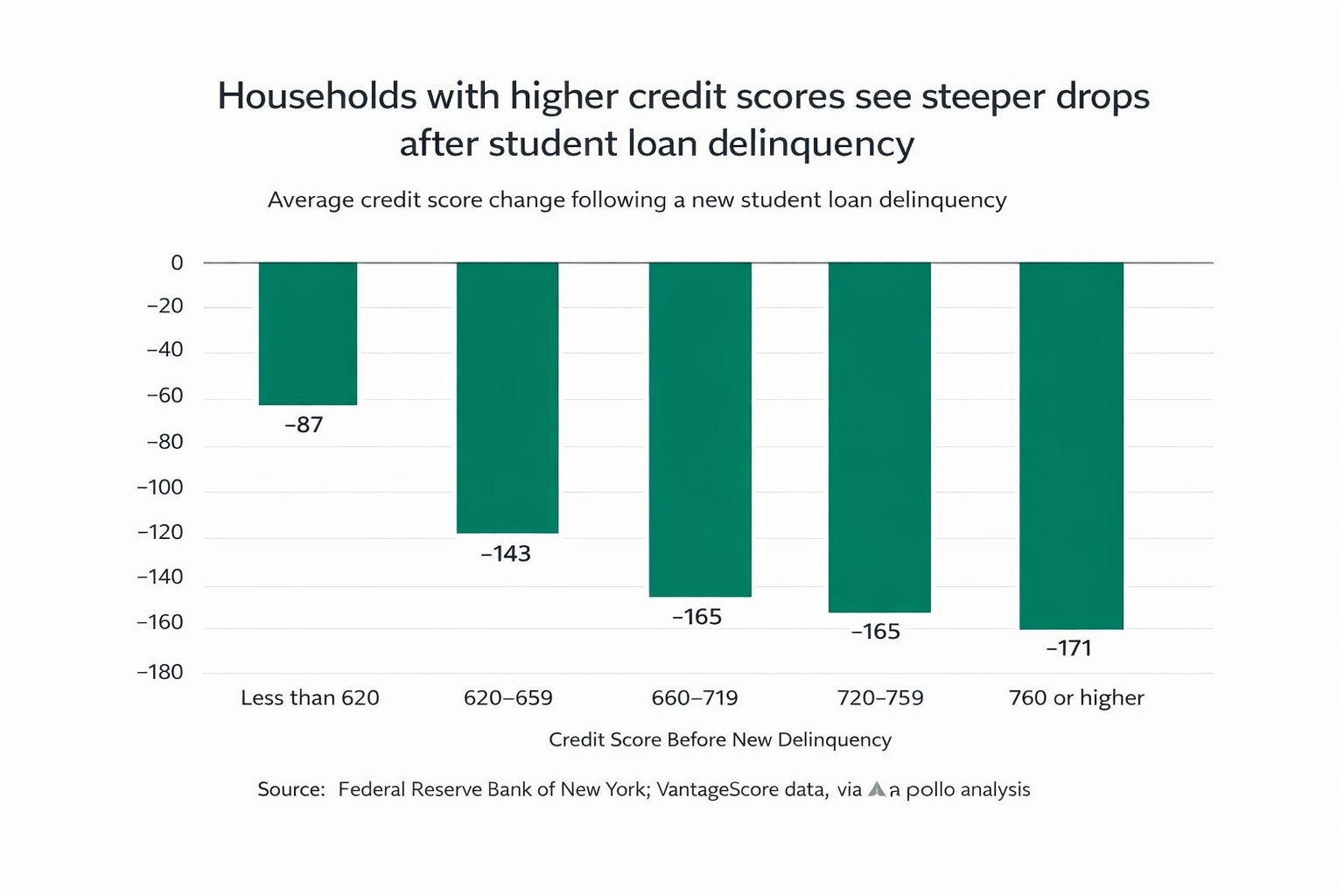

Almost 57% of newly delinquent borrowers now have credit scores below 620—a threshold where access to traditional credit becomes far more limited, and households with the highest FICO scores are getting the biggest hit.

Why student loan co-signers are seeing credit damage too

One of the least understood consequences of rising student loan delinquencies is how aggressively they affect co-signers.

Parents and grandparents who co-signed years ago—often to help a child qualify for school—are now discovering that a missed payment can impact their credit, even if every other bill is paid on time.

For older homeowners nearing retirement, that credit damage can feel especially destabilizing. A lower score can affect refinancing options, insurance pricing, and access to emergency liquidity at the exact moment flexibility matters most.

This is where many families start asking a different question: If unsecured credit is no longer an option, what is?

What happens when access to traditional credit disappears

Once credit scores fall, most borrowers learn quickly that credit cards and personal loans are no longer realistic solutions. Even when approvals exist, interest rates are often high enough to worsen financial stress rather than relieve it—with the average credit card interest rate (APR) currently hovering around 21% to 23%.

Homeowners, however, are in a different position.

Unlike unsecured debt, home equity is backed by an asset you already own. That distinction allows home equity products to remain accessible even during short-term credit disruption—and often at materially lower interest rates.

This is why many homeowners begin exploring options like a HELOC, a home equity loan, or a cash-out refinance.

...in as little as 3 minutes – no credit impact

Using home equity to pay off student loans

It's important to be clear: this isn't about turning student debt into housing debt. For most households, it's about financial triage.

Used strategically, home equity can help families:

- Replace high-risk, high-interest debt with a more manageable structure

- Reduce the chance of repeated delinquencies

- Stabilize monthly cash flow during a credit recovery period

This is especially true for homeowners who don't want to refinance a low-rate first mortgage just to access cash.

How Better HELOCs are improving families' financial health

At Better, we've seen firsthand how tapping into home equity can be a turning point—not just emotionally, but financially.

On average, Better customers save $1,279 per month when they use a HELOC or home equity loan to consolidate higher-interest debt or lower their monthly payments.

But the impact doesn't stop with cash flow.

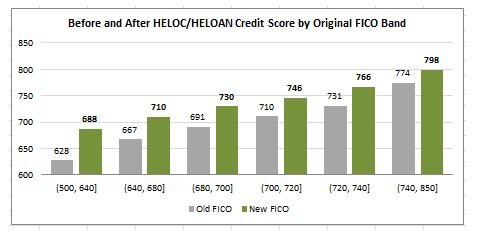

Based on Better's internal data, customers' credit scores increase by an average of 39 points after taking out a HELOC or home equity loan. The improvement is even more pronounced for homeowners who start with lower credit scores.

Average credit score improvement after HELOC or home equity loan (Better internal data)

As the chart shows, homeowners with lower starting credit scores tend to see the largest gains, giving them more breathing room and access to better financial options going forward.

This doesn't mean a HELOC is right for everyone—but it does show how asset-backed solutions can help stabilize households when unsecured credit fails them.

The bigger picture: This is about credit protection.

The rise in student loan delinquencies isn't a story about overspending. It's about a system shock that arrived quickly and unevenly.

For homeowners and co-signers, the goal isn't to borrow more—it's to protect credit, preserve flexibility, and prevent temporary setbacks from becoming long-term barriers.

Home equity isn't the right solution for every situation. But in a moment when traditional credit has become far less forgiving, it has quietly become one of the few tools still offering control.

What to do if student loans have hurt your credit

If missed student loan payments have already affected your credit, understanding how far your score has shifted—and which options remain—can help prevent rushed decisions driven by fear.

For many homeowners, the best place to start is to understand what your options are. For example, you could check today's rates for HELOCsand HomeEquity loans, or use a tool like Better's HELOC Calculator to estimate monthly payments if you decide to consolidate debts, like student loans, using your home's equity

If you're ready to get your cash estimate and custom rate, you apply for a pre-approval. It takes as little as 3 minutes, and you can get your cash in hand in as little as 7 days.

...in as little as 3 minutes – no credit impact