Maybe your kitchen hasn’t been updated since the ’90s, or your child just got into their dream college with a staggering tuition bill. A home equity line of credit (HELOC) might seem like the perfect solution. But it requires research.

While a HELOC is a great option for many homeowners, some don’t realize that every step of the HELOC process, from application to use, leaves fingerprints on your credit report.

So, does a HELOC affect your credit score? Below, you’ll get a complete answer to this perennial question. Plus, learn how to make sure your HELOC doesn’t hurt your credit profile in the long term.

What is a HELOC?

A home equity line of credit, or HELOC, is a type of second mortgage that gives you a spending limit you can use and pay back repeatedly, also known as a revolving line of credit. Your home is the collateral, which means lenders typically offer much lower interest rates than you’d get with other types of credit.

While a traditional home equity loan gives you a lump sum upfront, a HELOC works in two phases. During the “draw period,” which is usually 5-10 years, you can borrow money as needed up to your credit limit, similar to how you’d use a credit card. You only pay interest on what you actually use — not on the entire line of credit. After the draw period ends, you enter the “repayment period,” where you pay back both the principal and the interest over a set timeframe (which could be up to 20 years).

HELOCs have some significant advantages over other mortgages that have made them a popular choice for homeowners who need to tap into their equity:

Benefits of a HELOC

— Flexible funds for any project: Whether you’re renovating your kitchen, consolidating high-interest debt, or even buying a second home, a HELOC gives you the flexibility to use your equity however you see fit. There are no restrictions on how you can spend the money.

— Lower interest rates: Since your home acts as collateral, lenders view HELOCs as less risky than unsecured debt like credit cards or personal loans. This often translates to lower interest rates, potentially saving you thousands in interest payments.

— Building credit with consistent payments: If you have a limited credit history or want to strengthen your credit profile, making on-time HELOC payments can boost your credit score. Each monthly payment gets reported to the credit bureaus, demonstrating your ability to manage different types of credit responsibly.

— Potential tax benefits: The interest you pay on your HELOC might be tax-deductible if you use the funds to buy, build, or substantially improve the home that secures the loan.

Traditional HELOC applications can drag on for weeks, leaving you waiting when you need funds most. Better’s One Day HELOC™ fast-tracks the process, getting you pre-approved in as little as 3 minutes, and the cash you need in as little as 7 days.

Does applying for a HELOC affect your credit score?

Yes, applying for a HELOC usually affects your credit score, but the impact is generally small.

The relationship between HELOCs and credit scores is simple: When you submit your application, lenders need to evaluate how responsible a borrower you’ll be, which means they’ll request your credit report from one or more credit bureaus. This shows up as a “hard inquiry” or “hard pull” on your credit report. While “soft inquiries” like checking your own credit or getting pre-approved offers have no effect, hard inquiries can temporarily lower your credit score.

Luckily, the impact from a single hard inquiry is usually minimal, and your credit score should bounce back quickly. Plus, credit scoring models are designed to accommodate consumers shopping around for the best rates and terms, so they count credit checks made close together as a single inquiry.

If you want to get a sense of your borrowing power without any credit impact, Better’s 3-minute pre-approval can give you a cash estimate and custom rates with no effect on your score. This gives you the freedom to explore your options before committing to the formal application process.

How using a HELOC affects your credit

Once you’ve been approved and start using your HELOC, it becomes an active part of your credit profile. That means it influences your credit score in a variety of ways.

The biggest impact of a home equity line of credit on your credit score comes from your payment patterns. Consistently making monthly payments will increase your credit score over time, since lenders report this payment history to the credit bureaus. But, similar to other debts,missing a HELOC payment can seriously damage your credit score — especially if it happens repeatedly.

On top of that, opening a new HELOC lowers the average age of your credit accounts. If you’ve had your oldest credit card for 15 years and your mortgage for 10 years, adding a brand-new HELOC to the mix brings down that average account age. While this factor carries less weight than payment history, it can still give your credit score a temporary hit, especially if you don’t have many other established accounts.

A HELOC can also improve your credit mix. Credit scoring models favor borrowers who can successfully manage different types of credit. If you primarily have installment debt — like auto or personal loans — and add a HELOC as your first revolving credit account, the added diversity could increase your credit score slightly.

How closing a HELOC impacts your credit

When you’re ready to close a HELOC, you might wonder what happens to all that positive credit history you’ve built up. If you close it in good standing — meaning you’ve paid everything back and stayed current on payments — that account doesn’t just disappear from your credit reports. You continue to benefit from it for up to 10 years.

But closing your line of credit can create changes in other areas. If your HELOC was your only revolving credit account and you don’t have any credit cards open, you’ve suddenly lost the credit mix that scoring models like to see, which could hurt your score. The impact depends on the other accounts you have open and how long you’ve had them. Closing your HELOC also cuts into your total available credit, which can push your credit utilization ratio up on other accounts.

Let’s say you close a HELOC with a $40,000 credit limit and still have a $2,000 balance on a credit card with a $10,000 limit. Before closing the HELOC, your total available credit was $50,000, and your utilization was just 4%. After closing the HELOC, your available credit drops to $10,000, and your utilization jumps to 20%. Even though you didn’t take on any new debt, the higher utilization ratio could affect your credit score.

How Better HELOCs improve families’ finances

At Better, we’ve seen firsthand how tapping into home equity can be a turning point for families’ financial health. On average, our customers save $1,100 every month when they use a HELOC or home equity loan to consolidate higher-interest debt or lower their monthly payments.

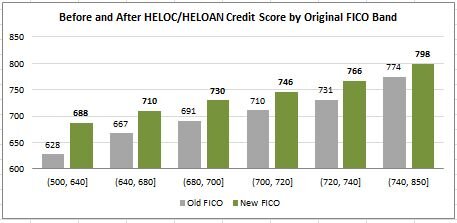

But the impact doesn’t stop there—credit scores also improve significantly. Based on our internal data, families’ credit scores rise by an average of 39 points after taking out a HELOC or home equity loan with Better. And the benefits are most dramatic for those starting with lower credit scores.

As you can see, homeowners with credit scores on the lower end of the spectrum see the largest improvement, giving them more financial breathing room and access to better credit opportunities in the future.

...in as little as 3 minutes – no credit impact

Final tips: Keep your credit score safe when opening a HELOC

Before you apply for a HELOC, take a close look at your existing debt situation. If you’re carrying high balances on credit cards, those can hurt your credit utilization ratio — and your credit score along with it.

When you’re ready to explore home equity loan and HELOC rates, timing matters. Since FICO and other credit scoring models lump hard inquiries in a short period of time into one, you can apply with different lenders to compare rates and terms without worrying about multiple hits to your credit score. Shopping around is a smart financial move that can save you a lot of money, so don’t let fear of credit inquiries keep you from finding the best deal.

With Better, you can see what you’re pre-approved for in as little as three minutes — with no impact on your credit score — to decide what option is best for you.

Check your HELOC eligibility without hurting your credit

Better makes tapping into your home’s equity transparent. Access tools that keep you informed, like the HELOC calculator that lets you see how much equity you can access and what your monthly payments might look like with a few clicks.

Once you’ve made your decision, spend just 3 minutes filling out the pre-approval application — with no effect on your credit score. You can get up to $750,000 with no hidden fees.

...in as little as 3 minutes – no credit impact