When you’re getting ready to buy a home, there’s more to think about than just your down payment. Closing costs typically end up being 2–5% of the loan amount, with one component being your loan origination fee.

An origination fee is a standard part of many mortgages, but it’s not always clear what it actually covers or how it affects your loan terms. Here’s a guide to what mortgage origination fees are, how much you can expect to pay, and the options you have for covering (or even avoiding) them.

What are origination fees?

A mortgage origination fee is what lenders charge to process your loan application. It’s typically 0.5–1% of the total loan amount, with 1% sometimes referred to as an “origination point.” On a $500,000 mortgage, that’s $2,500–$5,000.

Some lenders advertise “no origination fee” mortgages, but these often come with a higher annual percentage rate (APR). That means you might save upfront but end up paying more in interest in the long term. It’s a trade-off, and it’s worth calculating before deciding on a lender.

Not all mortgage lenders use a percentage-based fee. Some cap their origination charges at a flat rate, regardless of loan size. For example, they might charge a maximum of $3,500 for any loan. Others may scale the fee up or down based on factors like loan amount, loan type, or your credit profile. This makes it even more important to compare lenders and read the fine print.

Origination fees are different from discount points. While mortgage origination costs go toward paying the lender for services like processing, underwriting, and document preparation, discount points are optional.

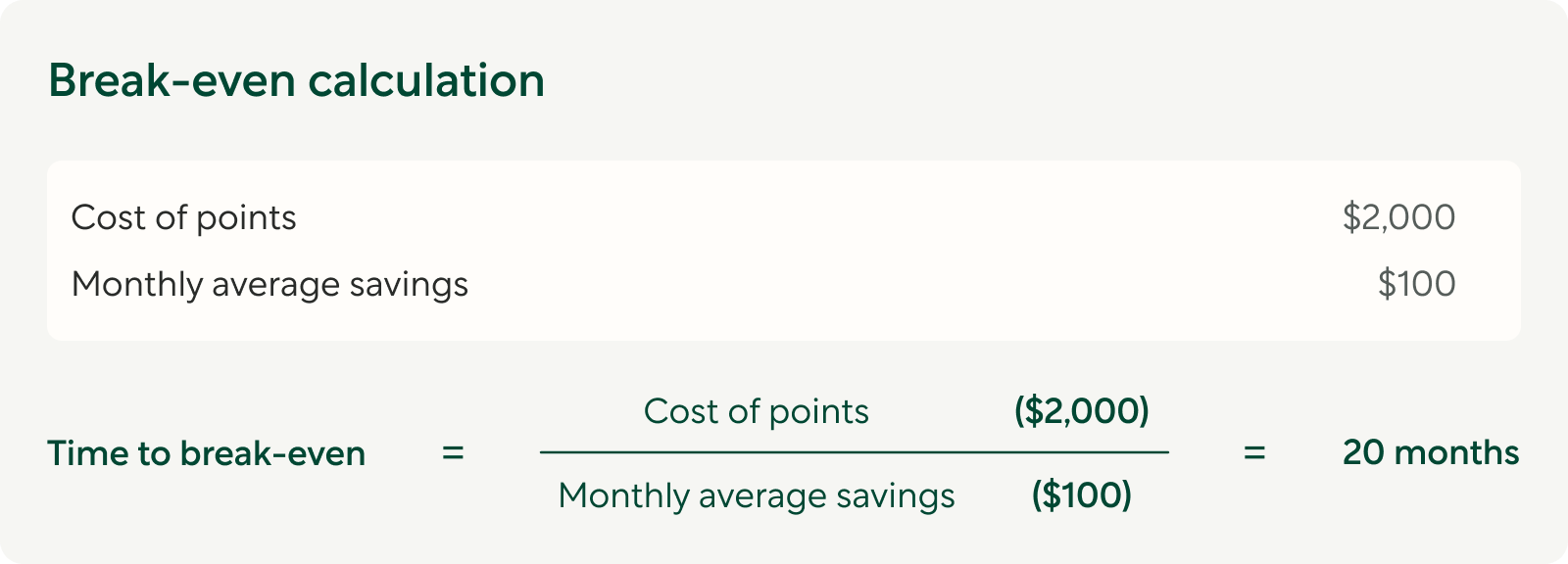

You can choose to buy discount points — usually 1% of the loan amount per point — to lower your interest rate. Each origination point typically reduces your rate by around 0.25%, though the exact impact varies by lender. If you plan to stay in your home for many years, buying points could save you money, but if you expect to move or refinance within a few years, you may not break even.

In the example below, you can see that it would take 20 months to break-even if you purchased $2,000 in points. Note that the specific timeframes will vary, depending on the loan.

Why do lenders charge origination fees?

Mortgages take work to process. Lenders verify your income and credit score, generate legal documents, and coordinate between different people and firms to move your mortgage loan forward. The origination fee covers all that labor. It also helps cover costs that aren’t always visible, like staying compliant with lending regulations. Mortgage lenders are required to meet strict legal and documentation standards, and these administrative tasks add to the overall cost of issuing a loan.

Not every lender charges origination fees the same way. Some might quote a flat-rate fee, while others break it down into individual line items. Mortgage brokers may charge slightly more since they’re acting as the go-between, and online lenders often charge less because they rely on automation and tend to have lower overhead. That’s why it’s important to compare not just the interest rate, but the full fee structure across lenders.

At Better, we’ve built technology to streamline the entire homebuying and mortgage process, making it cheaper for us to make the loan which means we can then pass the savings on to you.

...in as little as 3 minutes – no credit impact

Can you negotiate or avoid mortgage origination fees?

In some cases, you can try asking the seller to cover part or all of your closing costs (sometimes called settlement costs), including the loan origination fee. This might work if it’s a buyer’s market or the seller just wants to close the deal fast.

You can also try negotiating directly with the lender. Here are a few tips to improve your chances:

— Start early: Don’t wait until the end of the process to ask about a lower fee. Once you’re farther along, lenders are less likely to be willing to adjust.

— Get multiple offers: Use quotes from other mortgage lenders as leverage.

— Use your credit profile to your advantage: A high credit score and steady income can work in your favor.

— Ask about lender credits: Some lenders may be willing to offer credits in exchange for a slightly higher rate or roll your fees into the loan in a way that works better for you.

Keep in mind that lenders might reduce origination fees but raise interest rates or shift costs somewhere else. It’s all about finding the right balance for your budget and goals.

With Better’s Better Forever Program, we’ll waive origination fees on your future refinance or purchase loans once you fund a loan with us.

What does the origination fee cover?

Loan origination fees often come as a bundle that includes a mix of behind-the-scenes services. These types of fees include:

— Appraisal fees: Appraisal is having your home professionally valued.

— Credit report fees: These cover the cost of pulling your credit score and full credit report.

— Application processing fees: Processing fees concern the cost of reviewing your financial documents and verifying your information.

— Underwriting fees: Underwriting is evaluating your risk and determining your loan eligibility.

— Document preparation fees: These cover the creation of legal documents, including your loan estimate and closing disclosures.

— Administrative fees: Administrative fees concern tasks like title searches, compliance reviews, and coordinating between everyone involved in the mortgage.

Some lenders itemize these costs separately, while others include them all under a single “origination charge.” Either way, they show up in your loan estimate and closing disclosure.

How much do origination fees cost?

So, how much is a loan origination fee, exactly? Costs vary by lender, but the average loan origination fee falls between 0.5% and 1% of the total loan amount.

After applying for a mortgage, you’ll likely receive a loan estimate within three business days. This document includes your expected closing costs, including the origination fee, so you know what you’re working with from the beginning.

Better’s AI-powered mortgage gives you a full view of your costs upfront — not just your interest rate, but every fee you can expect, clearly laid out with nothing hidden. Then, you can compare offers with confidence and avoid any last-minute surprises at the closing table.

How to pay mortgage origination fees

Borrowers usually handle origination fees in one of several ways:

Upfront payment: Pay the fee directly at closing using funds from your bank account.

Rolling into the mortgage: Add the fee to your loan amount. This spreads the cost out over time but increases your monthly payments slightly.

Lender credits: Accept a higher interest rate in exchange for the lender covering your loan origination fee. This reduces upfront costs but can cost more in the long run.

Developer incentives: If you’re buying a newly constructed home, the builder might offer to cover some or all of your loan origination charges to close the deal.

Closing cost assistance programs: Depending on your income and location, you may qualify for grants or low-interest loans to help with closing costs.

Seller concessions: Try negotiating with the seller to cover part of your closing costs, especially if you’re in a market where buyers have the upper hand.

Negotiation with the lender: Strong financials or competing loan offers can help you negotiate fees down or remove them altogether. Just be sure to compare the overall cost of each offer, not just the fee line.

Better loan terms with no hidden fees

Mortgage origination fees are one of the standard costs that come with getting a home loan, but they don’t have to catch you off guard. When you know what they cover, what’s negotiable, and how they affect your loan terms, you can make smarter choices.

Better helps you navigate the mortgage process with more confidence and no surprises. With no hidden fees, you get a clearer path to closing — and one less thing to worry about along the way. Start your pre-approval today.

...in as little as 3 minutes – no credit impact