Interest-only HELOCs can harness the borrowing power of a home equity loan without charging huge monthly payments right away.

These lines of credit excel at covering large, temporary expenses — like renovating a house you plan to sell or refinance soon.

But interest-only HELOCs cost more as time passes, so homeowners should avoid parking long-term debt on a line of credit.

What is an interest-only HELOC, and how does it work?

Knowing how interest-only HELOCs work can help borrowers tap the strengths of these credit lines without paying their long-term repayment costs. So let’s look under the hood of these specialized credit lines.

HELOC stands for home equity line of credit, and this name reflects how these loans work. HELOCs are revolving lines of credit, much like a credit card, but secured by the equity in a home. This security helps the lender reduce interest rates and increase borrowing power.

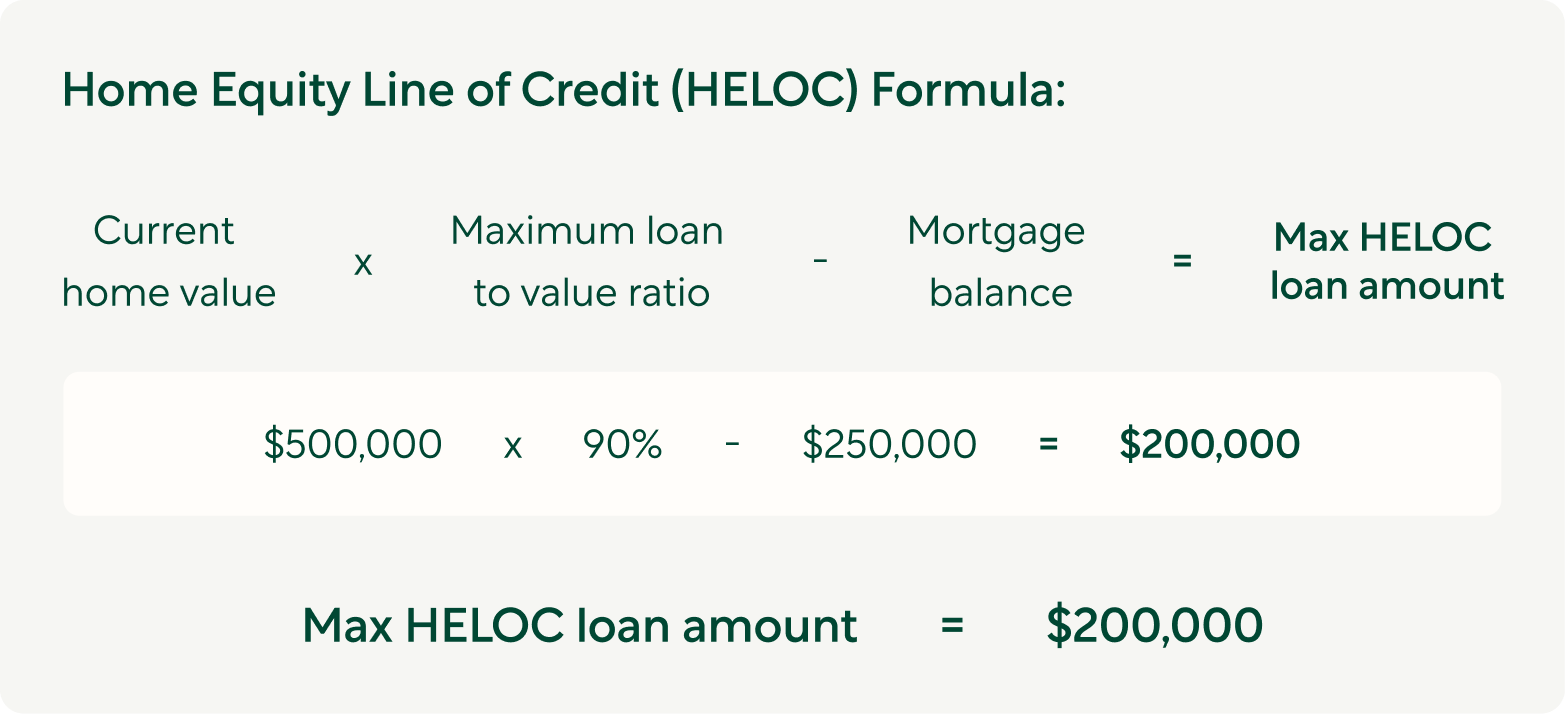

To open a HELOC, a homeowner must first have enough home equity to secure the credit line.

Let’s look at a HELOC on a home valued at $500,000. This home’s owner still owes $250,000 on the mortgage, meaning the remaining balance is already paid off equity.

Assuming this homeowner has the credit score and income to qualify, a HELOC could convert some of this equity back into cash. After opening the HELOC, the homeowner could withdraw money from the credit line and use it to pay off other debts, to renovate the home, to pay for college tuition, or for any other need.

....in as little as 3 minutes – no credit impact

HELOC payments

Since equity secures a HELOC, lenders can offer lower interest rates and higher credit limits when compared to unsecured loans.

As with a credit card, the homeowner can use, repay, and reuse the credit line as needed — during the HELOC’s draw period, which usually lasts 10 years.

During the draw period, the HELOC’s monthly payments will be based on the credit line’s revolving balance. After the draw period ends, the repayment period begins. During this repayment period, the homeowner can no longer draw from the credit line, and the outstanding balance at that time must be paid off by making regular principal and interest payments.

Here's an example breakdown:

Interest-only HELOC vs. traditional HELOC

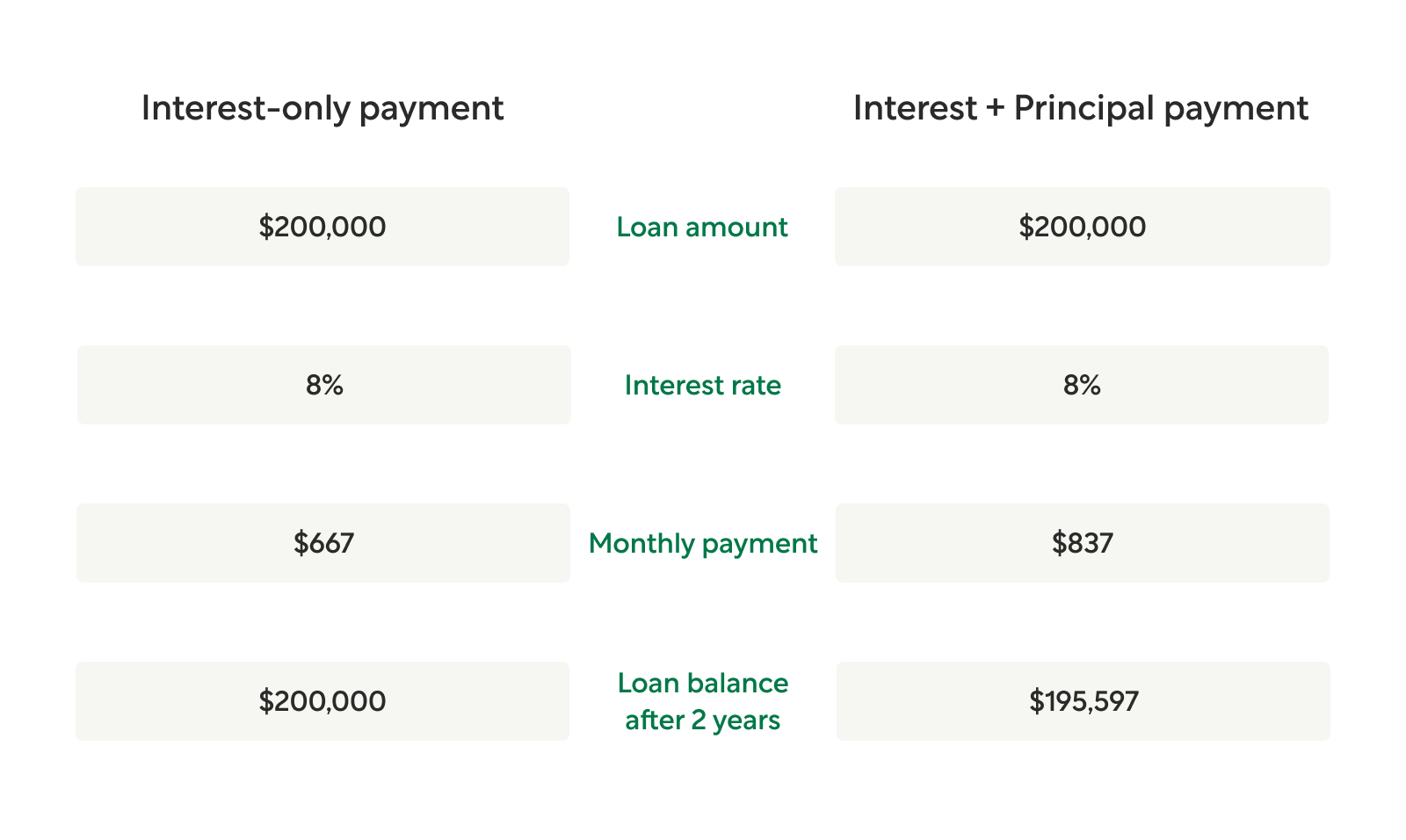

Interest-only HELOCs calculate monthly payments differently than traditional HELOCs. With an interest-only HELOC, the homeowner pays only the interest due on the balance during the draw period. If the borrower makes only the interest payments, the HELOC’s balance will not decrease.

Let’s say the homeowner from the example above got a $60,000 HELOC and immediately used $50,000 of the credit line to renovate a home they planned to sell.

At 8 percent interest, the $50,000 in debt would accrue $4,000 a year in interest. Each year, that $4,000 would be broken into 12 monthly payments of $333.33 per month.

These payments would not reduce the $50,000 principal balance. They would simply keep the interest on the debt serviced.

Interest-only payments are minimum payments

Paying only the interest due keeps minimum payments lower. But as with a credit card, making only the HELOC’s minimum payment stretches out the debt over a longer period of time, giving the lender more time to charge interest.

For example, if the homeowner in the scenario above paid only interest for five years on the $50,000 debt, the interest would cost $20,000 and the principal would still be $50,000.

Homeowners can save money by paying on the principal of the loan even though they don’t have to. Paying down principal also returns the equity to the home, recharging the HELOC for further use, either by the same HELOC or a new home equity loan.

Pros and cons of an interest-only HELOC

Do the pros of an interest-only HELOC outweigh the cons? That answer depends, a lot, on how the borrower plans to use the loan.

First, let’s look at the pros and cons:

Interest-only HELOC advantages

— Smaller payments, at first: During the HELOC’s draw period, paying only interest on the principal keeps monthly payments lower. Principal is deferred until the repayment period.

—Lower interest rates: Since home equity secures the credit line, HELOCs charge lower interest rates than unsecured loans such as credit cards and personal loans.

—Higher credit limits: Security from the home’s value also allows higher borrowing limits compared to unsecured loans.

—Flexible payments: Homeowners can make larger monthly payments to reduce principal — or they can make the minimum interest-only payment if necessary.

—Flexible borrowing: HELOC borrowers can draw funds as needed from their home equity instead of borrowing a lump sum and paying interest on that larger amount.

—Easy to open: Compared to primary mortgage loans and fixed-rate second mortgages, HELOCs can be simpler to open. For example, Better offers a fast, all-online application that can be funded in as little as seven days.

....in as little as 3 minutes – no credit impact

Interest-only HELOC disadvantages

—Variable interest rate: Rates on most HELOCs change, from year to year, to match market conditions. If the prime rate or other benchmark increases, the HELOC rate will increase too. (A HELOC rate could also go down with market conditions.)

—Interest-only payments delay payoff: Interest-only payments can save money in the short term, at the expense of long-term interest costs during the repayment period.

—Requires a lien on the home: A HELOC’s high credit limit and low interest rate (compared to unsecured loans) are possible because the lender puts a lien on the home. Failure to repay a HELOC on schedule could lead to foreclosure.

—Closing costs and fees: These types of loans usually require the borrower to pay closing costs that cover a new home appraisal, lender fees, and title fees. Closing costs vary by lender. Some HELOCs charge annual fees.

When is an interest-only HELOC a good idea?

Savvy borrowers can benefit from an interest-only HELOC’s lower monthly payments without getting stuck with the credit line’s long term costs.

Here how that can look:

Flipping a home to earn income

A property investor could use money from an interest-only HELOC, taken out on their primary residence, to help finance a new investment project. For example, HELOC funds could pay to fix up a dilapidated home, restoring the home to its full value.

While the renovation project is under way, the interest-only HELOC’s lower monthly payments help keep renovation costs lower. Then, once renovations are complete and the home sells, the investor could repay the HELOC, avoiding its long-term costs.

Renovating a home to help with a refinance

A homeowner could use funds from an interest-only home equity line of credit to remodel or renovate their home. Some renovations, such as updating the kitchen and the bathrooms, can add more value to a home — and homes with increased value are easier to refinance.

When the renovations are complete and the home has been reappraised at its higher value, the homeowner could take out a new refinance loan to pay off the HELOC, avoiding the interest-only HELOC’s long-term costs.

Plus, since the HELOC funds renovated the home, all the interest paid can be tax deductible.

Making a down payment on a second home

Borrowers who want to buy a second home could use an interest-only HELOC on their primary residence to generate a down payment for the second home. The lower, interest-only payments on the HELOC could help keep their debt-to-income ratio lower, helping them qualify for the primary mortgage on the second home.

Then, once there’s enough equity built up in the second home, the borrower could refinance the second home and pay off the HELOC.

Covering temporary new construction costs

Someone who’s building a new primary residence and planning to sell their current home once the new construction is complete could gain extra budget room with an interest-only HELOC.

Funds from the HELOC could help furnish the new home, for example. Then, when the current home sells, the homeowner could pay off the HELOC along with the primary mortgage. Meanwhile, the HELOC’s lower payments helped keep costs low during the construction process.

Creating budget flexibility

Someone whose income fluctuates from month to month might like the budget flexibility an interest-only HELOC can offer. During lean months, these types of homeowners can make the HELOC’s interest-only minimum payment. In months when they earn more, they can pay more to reduce the credit line’s principal balance, repaying the line of credit faster.

What these scenarios have in common

In these types of scenarios, the homeowner uses the interest-only payments strategically but does not intend to leave the principal debt on the credit line indefinitely. They use the credit line’s convenience for a specific purpose and then pay off — or start paying down — the principal soon after.

HELOCs are also convenient to open. Better’s all-online application process for interest-only HELOCs can check borrower eligibility within three minutes.

Alternatives to an Interest-Only HELOC

Interest-only HELOCs excel especially when they’re used intentionally. Homeowners who worry they might not pay off the HELOC within a couple years should also consider other types of loans, including:

—A home equity loan: These loans also leverage home equity, but they come with a fixed rate and fixed payments that include principal and interest. They’re usually scheduled to be paid off within five to 10 years.

—A fixed-rate HELOC: Some lenders offer HELOCs with fixed rates and payments that include principal and interest. Having principal built into the payments helps some borrowers pay off the loan sooner and avoid sticker shock during the repayment period.

—A cash-out refinance: Cash-out refinancing bundles a home’s existing mortgage debt with cash borrowed against the home’s equity. The end result: Paying on one larger primary mortgage instead of adding a second mortgage payment.

—Unsecured borrowing: Borrowing rates will be higher and loan amounts will be smaller, but unsecured borrowing leaves home equity untouched.

Conclusion

Interest-only HELOCs keep initial borrowing costs low, but borrowers should avoid the catch: paying more interest in the repayment period.

If keeping initial payments low on a home equity loan can help you achieve a specific goal, an interest-only HELOC from Better can start working for you within days.

Better also has a full array of other mortgage products to meet borrowers’ needs.

....in as little as 3 minutes – no credit impact