Did you know you can tap into your home's value without getting a new mortgage? Many homeowners want to pull cash from their homes but don't want to mess with their existing loan terms.

Your home's equity serves as one of your most important financial assets. You can use it for big expenses, paying off debt, or handling unexpected costs. The good news? You have several options beyond refinancing. A home equity line of credit (HELOC), home equity loan, or other choices might work better for your needs. This piece explores all the ways to unlock your home's value while keeping your current mortgage. You'll learn which option best fits your unique situation and future money goals.

What is home equity?

Your home's equity represents your financial stake in your property. It equals the difference between your home's current market value and what you still owe on your mortgage. To cite an instance, a home worth $350,000 with a remaining mortgage of $200,000 gives you $150,000 in equity.

You can build equity in two ways. Regular mortgage payments reduce your loan balance and increase your equity. Your equity also grows when your property value goes up. This makes home equity a valuable financial asset that grows throughout your homeownership.

Most people let their equity sit idle, but it's actually a versatile financial tool. You can call it an investment in a relatively liquid asset. You might tap into your equity without changing your existing mortgage terms, which gives you flexibility when you need money.

Understanding what home equity means is significant before you try to access it. You can't just withdraw equity like money from a savings account - you need specific financial tools to turn it into usable funds.

Your home serves as collateral when you access its equity, which comes with risks. Missing payments could lead to foreclosure. Market conditions can also make your equity go up or down.

You should calculate your current equity before you tap into your home's value. This helps you know how much money you can access through different methods. Lenders won't let you borrow all your equity - they usually cap it at 80-85% of your home's value minus your remaining mortgage.

These basics are the foundations for smart decisions about your equity access options.

With Better, you can tap up to 90% of your equity on properties including your primary, secondary, and even investment properties.

....in as little as 3 minutes – no credit impact

How to get equity out of your home without refinancing

You have several ways to tap into your home equity without refinancing. Let's look at these options to help you find the best fit for your financial needs.

Home Equity Line of Credit (HELOC)

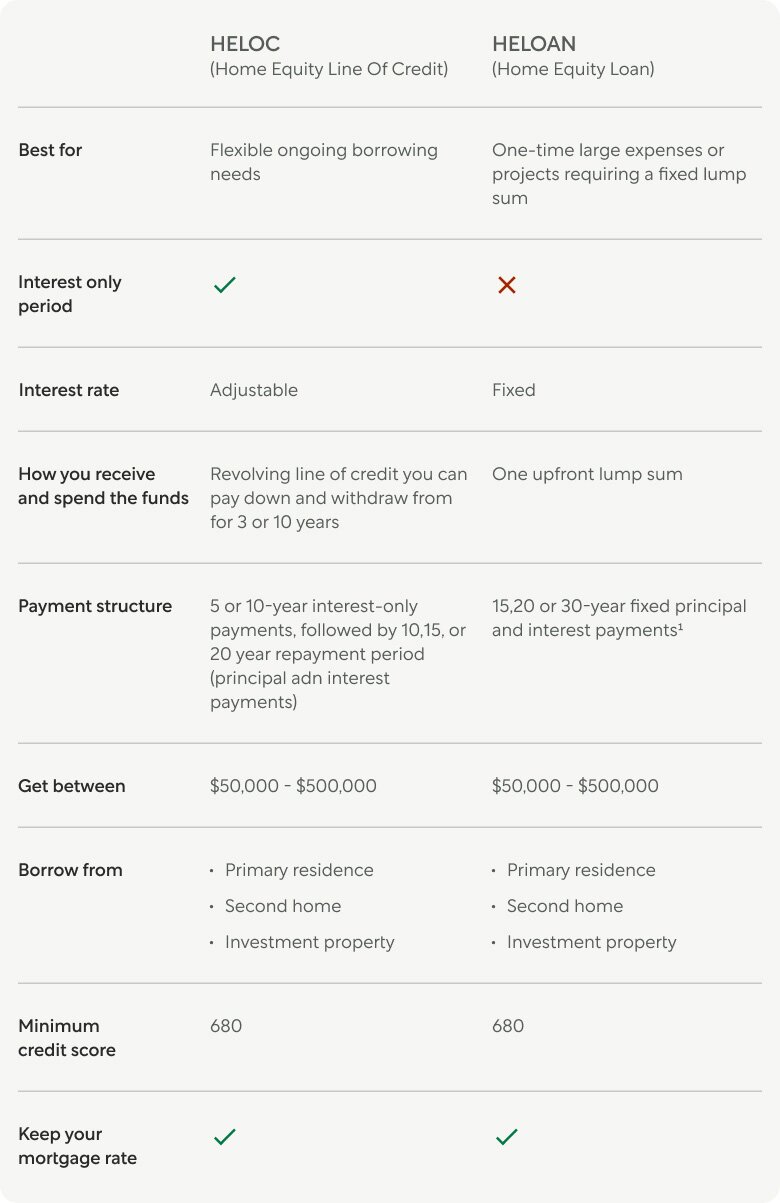

Think of a HELOC as a credit card that uses your home as collateral. This credit line lets you borrow money whenever you need it during a "draw period" of up to 10 years. You'll pay interest only on what you borrow, not your total credit limit. After the draw period ends, you start making full principal and interest payments.

HELOCs come with lower interest rates than credit cards, but these rates can vary.

Most lenders want you to have at least 15-20% equity in your home. You'll also need a credit score of 620 or higher and your debt-to-income ratio should stay below 43%.

See Better's HELOC requirements here.

Home Equity Loan

A home equity loan works differently from a HELOC. You get all the money upfront and make fixed monthly payments over 5-30 years. Your interest rate stays the same, so your payments never change. This makes these loans perfect for big one-time expenses like home improvements or paying off high-interest debt.

Here's a breakdown of the differences between HELOCs and home equity lines of credit.

Reverse Mortgage

Homeowners who are 62 or older can use a reverse mortgage to turn their home equity into cash without monthly payments. The loan only needs to be repaid when you sell your home, move out permanently, or pass away. This option helps provide retirement income while you stay in your home.

Home Equity Investment (HEI)

An HEI lets an investment company buy a share of your property, usually 15-30%. You get cash based on your home's current value and don't make monthly payments. The catch? You must pay the investor their percentage of your home's future value when you sell or the contract ends.

Sale-Leaseback Agreement

This option involves selling your home and then renting it back from the buyer. You get all your equity in cash and can keep living in your home by paying market-rate rent. Remember that you give up ownership and won't benefit if the property value increases.

Personal Loan

A secured personal loan uses your home as collateral and processes faster than traditional equity loans. The interest rates run higher than home equity options, but these loans work well if you have good credit and need quick access to smaller amounts.

What about a Cash-Out Refinance?

A cash-out refinance gives you a brand new loan that replaces your existing mortgage. The new loan amount exceeds your current debt and pays you the difference in cash.

Cash-out refinancing changes your primary mortgage terms, unlike other equity-access methods we discussed earlier. This option works best when today's interest rates fall below your original mortgage rate. You might need substantial funds for long-term investments like major renovations. The process also lets you combine multiple loans into one.

All the same, cash-out refinancing needs careful thought. The higher closing costs range from 2-5% of the new, larger loan amount compared to other ways to access equity. That said, it typically comes with lower interest rates depending on the market.

Many lenders require strong credit profiles with FICO scores of at least 660, (Better requires a credit score of 620). FHA and VA cash out refinance loans offer less strict requirements, but they charge their own mortgage insurance fees.

The biggest impact comes from resetting your loan term. This adds years of interest payments to your timeline. Your mortgage balance grows larger and monthly payments may increase.

You ended up needing to compare a cash-out refinance with alternatives like HELOCs or home equity loans. Each option meets different needs. Cash-out refinancing serves people who need substantial funds at lower rates and don't mind a longer mortgage timeline. The non-refinancing options we discussed might work better for smaller, shorter-term needs or if your current mortgage terms are good.

Check out cash-out refinance rates

....in as little as 3 minutes – no credit impact

Pros and cons of refinancing

You need to understand what refinancing means before accessing your equity options. A refinance completely replaces your existing mortgage loan. This brings clear advantages and drawbacks you should think over.

Pros

— Lower interest rates: Getting a refinance loan with a lower interest rate than your original mortgage may save you money over your loan's life. Most homeowners choose to refinance mainly because of this reason.

— Fixed interest rate stability: You can switch from a variable to a fixed interest rate through refinancing. Your monthly payments become predictable throughout the loan term. This makes budgeting much easier.

— Extended loan terms: Spreading payments over a longer period reduces your monthly payments. Your budget gets more breathing room.

— Cash-out option: Your home's value might have grown by a lot. A cash-out refinance lets you use this increased value for major expenses or investments.

Cons

— Substantial closing costs: You'll pay costs that match your original mortgage with refinancing—usually 2-5% of the new loan amount. Even a no-closing cost refinance adds these expenses to your loan balance or leads to higher interest rates.

— Resetting the loan clock: Your loan term starts over with a cash-out refinance. This means extra years of interest payments. This is different from other equity access options that don't change your primary mortgage differs from other equity access options.

— Stricter qualification requirements: Cash-out refinancing needs higher credit scores than standard mortgages. Lenders usually want 660+ compared to the basic 620 requirement.

— Foreclosure risk: Your monthly payments increase with a larger mortgage after refinancing. Your home faces foreclosure risk if you can't make these payments.

— Higher interest rates: Lenders may charge more interest on cash-out refinance loans due to increased risk.

Your specific financial situation and goals determine if refinancing makes sense. Compare current refinance rates with HELOC rates and home equity loan options to find what works best for you.

How to choose the right option

You need to review several factors to pick the right equity access method that matches your financial situation and goals. Here's what you should think about to find your best option:

— Get a full picture of your short and long-term needs. HELOCs and home equity loans work well for specific costs like renovations or debt consolidation.

— Review current interest rates. Rates differ by a lot between options. HELOCs usually have lower rates than personal loans, but their variable terms could change over time.

— Know your monthly payment comfort zone. This matters especially when you have HELOCs. Make sure you can handle your original mortgage payments while paying interest-only amounts on what you've borrowed.

— Check your home sale timeline. Sale-leaseback agreements could make things tricky if you plan to sell in the next few years since you won't own the property anymore.

— Know what it takes to qualify. Regular equity loans need good credit scores, income proof, property values, debt-to-income checks, and solid mortgage payment history. Equity investments focus more on minimum home values, where you live, and what type of property you have.

— Look at upfront costs. Each option has different fees for applications, appraisals, title searches, and closing. HELOCs usually cost less upfront than refinancing.

— See what it means for your finances. Think about interest charges, sharing future appreciation with equity investments, how it affects your home sale money, and possible tax effects.

Each option has its sweet spot:

— Home equity loans: Big one-time expenses

— Shared equity arrangements: No extra monthly payments

— Home equity investments: Better debt-to-income ratio

— Personal loans: Quick equity access

The best choice comes down to your current money situation, future plans, and what you need the funds for. Getting several quotes and talking to financial advisors are great ways to figure out which option gives you the best terms.

Conclusion

You can access your home's equity without refinancing, which gives homeowners great flexibility to find financial solutions. This piece explores several ways to tap into your property's value while keeping your original mortgage intact. Each option serves different needs based on your situation - from HELOCs and home equity loans to reverse mortgages and equity investments.

Your financial goals should be clear before you make any decision about your home equity. To cite an instance, a HELOC might be your best choice if you need ongoing access to funds. A home equity loan could better serve your needs if you prefer predictable payments. Older homeowners might find reverse mortgages helpful for retirement planning.

Qualification requirements differ by a lot between these options. Comparing multiple offers helps secure the most favorable terms. The risks need careful consideration - especially the chance of foreclosure if payments become too much to handle.

The choice between accessing equity without refinancing versus getting a cash-out refinance should line up with your long-term financial strategy. You should compare current HELOC rates and home equity loan rates against refinance rates to understand your options fully.

Your home provides both shelter and a chance for financial growth. Tapping into its equity needs thoughtful consideration, with clear purpose and understanding of what it all means. The right choice depends on balancing your immediate needs with future financial security - whether you pick a HELOC for renovation projects or explore a no-closing cost refinance option. Your home isn't just your biggest asset - it's a powerful financial tool that works best when used wisely.

....in as little as 3 minutes – no credit impact