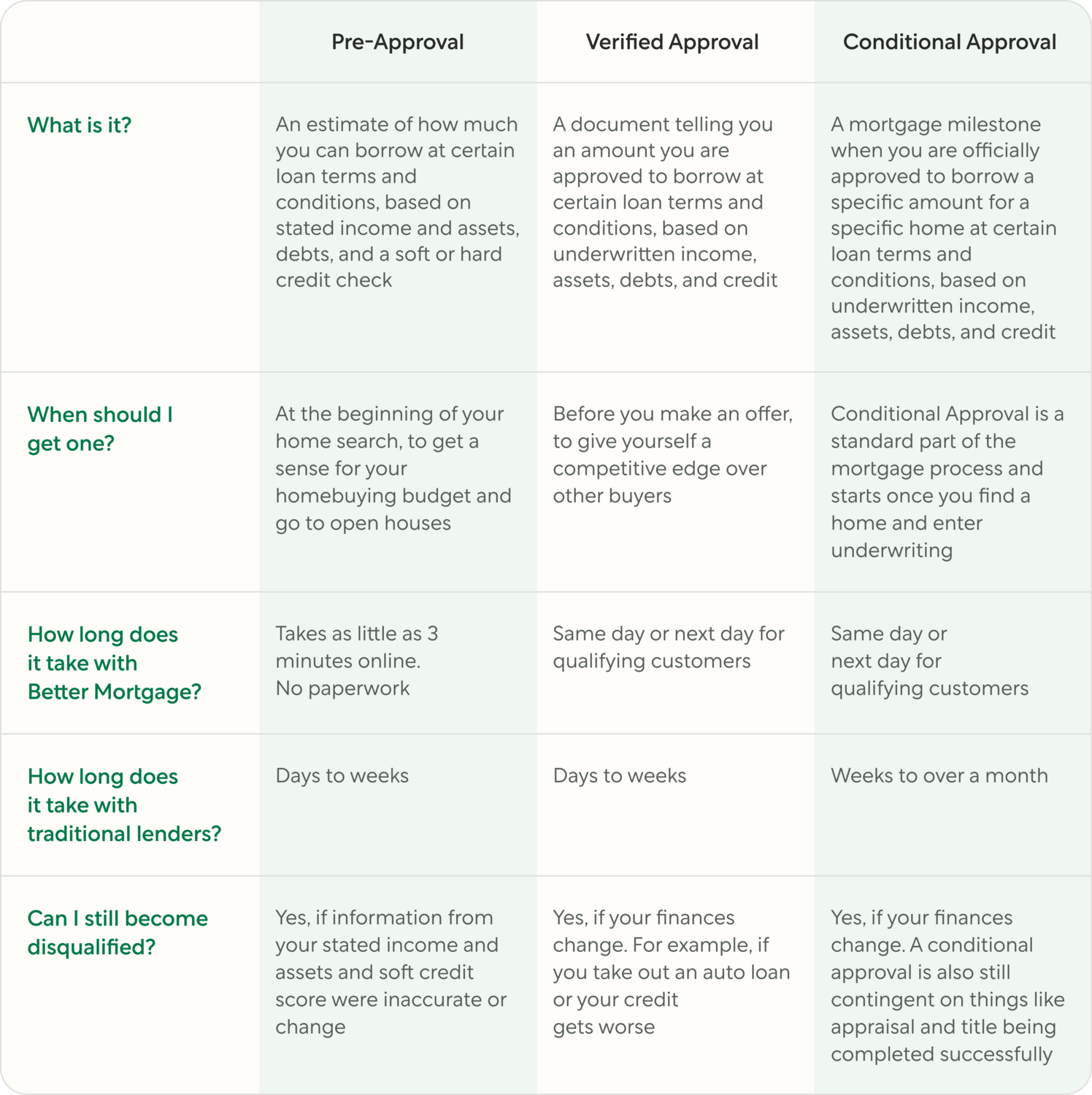

Anyone who’s not one of the lucky few to buy a home with cash will need to get approved by a lender for a mortgage. The first thing to know about a mortgage approval is there’s no single moment of ‘approval’ throughout the process. Instead, there are multiple approvals that increase in verification and certainty as you get closer to buying a home.

The ease and speed of approvals can vary greatly from lender to lender, so keep this in mind as you shop around. As a general rule of thumb, the stronger and faster the approval, the better. Stronger approvals can increase your chances of winning an offer and help give you peace of mind that you’ll get the loan.

In this post, we’ll break down the different types of buyer approvals and when and how to get them.

What is a mortgage approval?

A mortgage approval is the process by which a lender evaluates a borrower's financial and creditworthiness to determine if they are eligible for a mortgage loan for specific terms and conditions of that loan, like rate and loan term length.

Mortgage approval is a crucial part of the homebuying process, as it signifies that the lender is willing to provide the borrower with the funds needed to purchase a home, subject to certain conditions and requirements.

The three main types of mortgage approvals we’ll review here are pre-approval, verified approval, and conditional approval.

What is a mortgage pre-approval?

A mortgage pre-approval is an estimate of what a lender is willing to lend you. It’s based on your income, assets, debts, and credit profile, as well as the loan term, (e.g. 30-year fixed, 15-year fixed), down payment, property type, and estimated interest rate, property taxes, homeowners insurance.

Once you’re pre-approved, lenders will issue you a letter stating the loan amount you are pre-approved for. One thing to keep in mind is that your letter will often show the loan amount that you think you’ll need to borrow instead of your maximum pre-approval amount. This is because you typically include the letter when you submit offers, and it can weaken your negotiating power to show sellers the maximum you can afford.

When should I get a mortgage pre-approval?

It’s recommended that you get pre-approved before you start shopping for homes to get a sense for your home buying budget, view homes within that budget, and show sellers that you’re a serious buyer who can afford the home.

How to get a mortgage pre-approval?

To issue you a pre-approval, lenders will collect information on your income, assets, and debts. Because pre-approvals are not standardized across lenders, the information and documentation you need to provide will also vary by lender.

At Better Mortgage, your pre-approval is based on stated income and assets and a soft credit pull. This will never impact your credit score, so anyone who is curious about their affordability can get a pre-approved estimate at any time.

Is my mortgage pre-approval final?

The more accurate you are with your inputs on income and assets, the more accurate your pre-approval will be, but a pre-approval is not final and is only intended to give you an estimate of how much you can borrow. To get increased certainty around how much you can afford, we recommend getting a verified approval.

Three Minute Pre-Approval

At Better Mortgage, our pre-approval process is 100% digital and takes as little as three minutes. At the end of pre-approval, you’ll see your maximum estimated loan amount. Plus, you can edit your letter 24/7 in your dashboard to reflect any loan amount within your maximum that you need.

What is a mortgage verified approval?

A verified approval also shows how much a lender is willing to lend you for specific loan terms, but unlike a pre-approval, it’s fully underwritten by an underwriter.

When should I get a verified approval?

Verified approvals are not required in the mortgage process, but can be extremely impactful before you start making offers in order to stand out against competing bids.

Verified approvals can increase your likelihood of winning an offer because sellers want confidence that the offer they accept won’t fall through. A verified approval gives a seller certainty that their buyer will get the loan as long as the buyer’s finances don’t change during the mortgage process, and that everything with the house, like appraisal and title, is completed successfully.

How to get a verified approval?

In order to issue a verified approval, lenders will need to verify your income, assets, and credit. This will involve a hard credit check, employment verification, and a review of certain documents. The exact set of documents will vary based on each person’s financial situation, but typically include:

Is my verified approval final?

While a verified approval is an official document telling you how much a lender will let you borrow, your loan is not guaranteed. You can lose your approval if your financial situation changes. For example, your qualification could be impacted if you lose your employment or take out a new loan during the mortgage process that impacts your credit and/or debt-to-income ratio.

Additionally, any approval is conditional upon the home you buy also meeting certain requirements, like appraising at the amount you have placed an offer for, and clearing title to confirm that no one else has an ownership claim to the property. At the time you get a verified approval, you may or may not have a specific home address, and appraisal and title don’t start until after you have an accepted offer, so it is not final.

What is a debt-to-income ratio?

Your debt-to-income ratio (DTI) is your monthly debt payments divided by your gross monthly income. The highest DTI you can have and still get approved for a conforming loan at Better Mortgage is 50%. Let’s say your monthly debt payments are $3,800 and gross monthly income is $8,000, so your DTI is 47.5%. If you take out an auto loan at $300/month, your debt to income ratio would increase to 51.25% ($4,100 / $8,000 = .5125) and potentially make you ineligible for the mortgage.

One Day Verified Approval

While this process can take weeks with traditional lenders, at Better Mortgage we offer verified approvals in 24 hours or less for qualifying borrowers.¹

What is mortgage conditional approval?

Conditional approval is a binding agreement from your lender approving you for specific mortgage terms on the home you are buying. Like a verified approval, it means your finances have been fully underwritten. The key differences are that it is always for a specific home and is issued after you’ve made an offer.

At this point, the steps left until you close are related to verifying that there are no issues with the items like home inspection, appraisal, or title.

When will I get conditional approval?

Conditional approval happens after you have a signed purchase contract if you’re buying, have locked a rate, and your finances have been underwritten by an underwriter.

How to get a conditional approval?

Conditional approval is a standard step in the mortgage underwriting process. In order to get a conditional approval, you will apply for a mortgage, lock a rate, and start underwriting.

Is my conditional approval final?

Same as with a verified approval, a conditional approval is not a guarantee you will get the loan and is still contingent upon a successful appraisal and title search. During this period, it’s crucial that you maintain your finances and avoid taking out any lines of credit or loans.

One Day Conditional Approval

Conditional approval can take weeks with traditional lenders. At Better Mortgage, we deliver you a conditional approval via a commitment letter in as little as 24 hours with One Day Mortgage.²

Pre-approval vs verified approval vs conditional approval

Start the mortgage approval process today

At Better Mortgage, we’ve built technology that no other lender has, to deliver our customers mortgage approvals faster than anyone else we’ve seen.

Disclaimer: This post does not constitute an endorsement or recommendation of Better Mortgage Corporation; Better Real Estate, LLC; Better Cover, LLC; Better Settlement Services, LLC; or their services. Better Cover is solely responsible for homeowners insurance services. Better Mortgage is solely responsible for making all credit and lending decisions with respect to mortgage loans.

¹ See One Day Verified Approval terms and conditions

²Better Mortgage’s One Day Mortgage promotion offers qualified customers who provide certain required financial information/documentation to Better Mortgage within 4 hours of locking a rate on a mortgage loan the opportunity to receive an underwriting determination from Better Mortgage within 24 hours of their rate lock. The underwriting determination is subject to customary terms, including fraud and anti-money laundering checks, that take place pre-closing and which may trigger additional required documentation from the customer. Better Mortgage does not guarantee that initial underwriting approval will result in a final underwriting approval. See One Day Mortgage Terms and Conditions.