What you'll learn ✅

- The hidden costs of 401(k) hardship withdrawals (taxes, penalties, and lost growth)

- Two ways to access your home equity: HELOCs vs. home equity loans

- A head-to-head comparison showing why home equity can save you thousands

- The qualification requirements and timeline for getting a HELOC or home equity loan

- Smart strategies for using home equity without putting your home at risk

These are challenging financial times for many Americans. For proof, consider that hardship withdrawals among 401(k) participants jumped to 6% in 2025, up from 5% a year earlier, according to recent findings from Vanguard.

"There's a perfect storm of persistent inflation and depleted emergency savings causing this higher rate of hardship withdrawals right now," says personal finance expert Yehuda Tropper, with Beca Life Settlements. "This makes sense, given that consumer prices in the United States have risen about 23% since 2019."

Although the IRS permits these hardship withdrawals for specific emergencies – such as preventing foreclosure or funding costly medical bills – the rising frequency of these withdrawals underscores a deepening reliance on long-term assets to solve immediate liquidity problems. The big problem with this strategy is that Americans are quietly sabotaging their retirement to solve short-term problems.

But if you own a home, there's a smarter alternative you may be overlooking if you need money in an emergency.

See your options in as little as 3 minutes — no credit impact

The real cost of a 401(k) hardship withdrawal

Consider a hardship withdrawal a "break glass" type of emergency option involving your retirement savings. Whether you are allowed to pursue a hardship withdrawal from your retirement account will depend completely on your specific retirement plan's rules. According to the IRS, for most workplace plans like a 401(k), you can typically only take a "hardship distribution" if you have an urgent financial emergency that you can't afford to pay by any other means.

The IRS limits these distributions to particular situations, such as paying for certain medical bills, covering funeral costs, or preventing eviction and foreclosure. You are only permitted to withdraw the exact amount needed to cover the bill (plus any taxes the withdrawal triggers). But unlike a loan, you don't pay this money back to yourself.

Note that this technically counts as taking your retirement early, so you'll have to pay regular income taxes on it, and you'll likely be hit with an extra 10% penalty fee if you're under age 59½. Also, after taking a hardship withdrawal, you can't put any new funds into your retirement account for at least six months, which can further slow down your long-term savings.

Truth is, a hardship withdrawal from your retirement account will cost you now – in the form of higher taxes and penalty fees – and in the future when you consider lost compound growth on the withdrawn amount.

Case in point: Let's say you took a $30,000 hardship withdrawal from your 401(k) and you are 57 (younger than age 59½) and in a 22% tax bracket. If so, you count on paying $6,600 extra in federal income taxes and $3,000 (the 10% penalty) to the IRS. That leaves you with merely $20,400 in actual cash.

Now, imagine if you had left that money untouched in your account instead. If that $30,000 was able to grow at a typical 7% annual return over 10 years, it would have blossomed into more than $59,000 by the time you reached age 67. Missing out on $59,000 in potential growth equates to sacrificing roughly $2,360 in annual retirement income for the rest of your life based on a 4% safe withdrawal rate.

The benefit of compound growth is that each extra dollar added grows exponentially. Instead of taking money out of retirement, most Americans would be better off just limiting or stopping retirement contributions to handle an emergency or pay off debt.

The key point here is that this hardship withdrawal from your retirement funds isn't a loan: It's a permanent leak from your net worth.

What is home equity, and how can you access it?

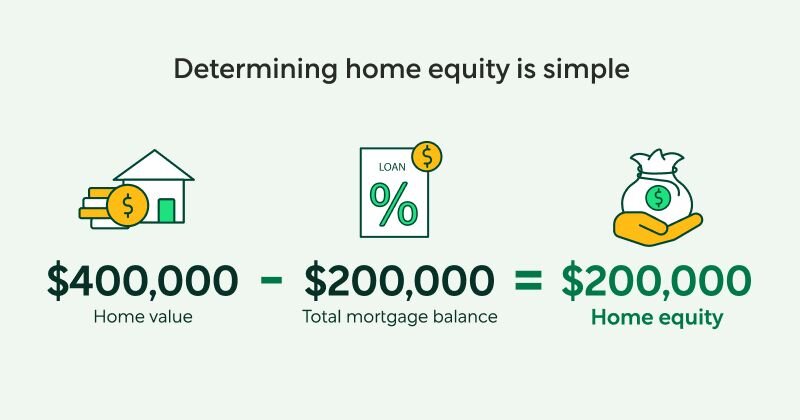

Home equity is the difference between your mortgage balance and the current market value of the property. It measures how much of your home is truly yours versus what mortgage lender owns. As you make payments toward the principal on your mortgage, your home equity grows by lowering the remaining debt you owe and chipping away at your lender's financial interest.

There are two main home equity products that homeowners can use to tap their accrued equity:

A home equity loan. This is a popular way to access a lump sum of cash by borrowing against the value you've built in your property without replacing your current mortgage. Often called a second mortgage, this loan "stacks" on top of your existing monthly payment and typically features a fixed interest rate with a set repayment term, much like a traditional mortgage. Because your home serves as collateral, it offers a way to get the funds you need all at once while keeping your original low-interest rate locked in on your primary loan.

A home equity line of credit (HELOC). This works more like a credit card tied to your home's value, allowing you to withdraw funds as needed rather than taking a single lump sum. For the first three to five years, known as the draw period, you typically only have to pay interest on the amount you actually use. Once that period ends, the repayment phase begins – often lasting up to 30 years – during which you must pay back the balance, including principal and interest.

Typical rates for both products average between 7% and 8% currently, making a HELOC or home equity loan a better strategy than using credit cards (rates average north of 20%) and personal loans (average rates exceed 12%). Plus, homeowners with sufficient equity and credit scores can access funds quickly via a home equity loan or HELOC.

Get clarity in as little as 3 minutes — no credit impact

The head-to-head math

To compare the pros and cons of a 401(k) hardship withdrawal to liquidating your equity via a HELOC or home equity loan instead, let's take a closer look at the numbers.

Let's assume you need $30,000 in emergency funds:

| 401(k) hardship withdrawal | HELOC/home equity loan | |

|---|---|---|

| Immediate taxes + penalties | $9,600: $6,600 tax + $3,000 penalty | $0: Loans are not taxable income |

| Actual cash received | $20,400: You must withdraw approximately $44,000 to net $30,000 | $30,000 |

| Repayment required | None: The funds are gone forever | Monthly, interest only first for HELOC, then principal + interest |

| Estimated monthly cost | $0 | $350 - $425 (assuming a 10-year term) |

| Total interest/cost paid | $9,600 in immediate lost cash (paid to IRS) | $11,800 - $13,600 over 10 years |

| Future opportunity cost | $29,015 in forgone earnings | $0: Your retirement stays invested |

| Impact on retirement | $2,360 less annual income for life | No impact on retirement income |

| Illustrative example only. Actual costs, returns, and loan terms will vary based on your financial situation, market conditions, and lender. |

The key takeaway here is that tapping your equity via a home equity loan or HELOC should cost far less than if you had withdrawn those same funds from your retirement account. While HELOC and home equity loan rates vary based on market conditions and borrower qualifications, they are often lower than credit cards and personal loans.

When home equity makes sense — and when it doesn't

Good candidates for a home equity loan or HELOC at a time of urgency include homeowners with job security and reliable earnings, sufficient equity, and the discipline to repay your debt on time.

"It makes sense to tap your home equity when you have stable income to service the debt, meaningful equity built up, and a specific short-term need you can realistically pay off," says personal finance professional Josh Katz, CPA. "It doesn't make sense when your income is already shaky, when you are borrowing against the house for discretionary spending, or when you are so close to retirement that a new debt obligation creates cash flow problems."

Proceed with caution, especially if you have non-traditional employment or variable income and you are already stretched on housing costs. Remember that both home equity products require using your home as collateral. That means you risk foreclosure if you can't repay what you borrow.

Ultimately, a HELOC or home equity loan should be regarded as a strategic tool that can come in handy in a pinch. But these products are not intended to be magic solutions to problems.

How to access your home equity quickly

Eager to pursue a home equity loan or HELOC? Here are the typical steps involved:

Check your equity. Determine your home's equity position and current value. To calculate your equity, you subtract your existing mortgage balance from your property's current market value; the latter can be estimated by checking recent home sales numbers in your area and/or getting a fresh appraisal from a professional if your chosen HELOC lender requires it.

Determine your LTV ratio. The sum you owe on your mortgage loan versus your property's current market value is expressed as a loan-to-value (LTV) ratio percentage. To calculate it, divide your existing mortgage balance by your property's value, and multiply by 100.

Shop for a HELOC or home equity loan. Shop around for lenders among local banks, online lenders, credit unions, and other financial sources, and also consider Better.com. Carefully compare rates, fees, and draw periods.

Apply and get approved for a HELOC or home equity loan. After choosing a lender, submit a formal application for the financing. Prepare to furnish paystubs and proof of income, bank statements, credit history, tax returns, and other requested documentation. The underwriting process can take a few weeks before you are finally approved for a HELOC.

Close on the loan or line of credit. After underwriting approves, you'll proceed to closing, where you'll sign the necessary loan documents and receive your funds if it's a home equity loan. If it's a HELOC, you can withdraw your approved funds whenever you are ready.

Expect this entire process, from applying to closing, to take between two and six weeks (although some lenders offer expedited processing), so plan ahead if possible.

Better expedites this process. Our AI technology does the shopping for you, evaluating 21,600 loan scenarios to find your best rate¹. You can get pre-approved in as little as 3 minutes without impacting your credit. And, if you decide to move forward, Better offers a One Day HELOC, where you can get your cash in as little as 7 days².

Get a personalized estimate in minutes — no credit impact

Conclusion

The bottom line is that eligible homeowners can pursue a smarter path to emergency funds than raiding their retirement savings. Remember that your 401(k) is a long-term compounding machine designed to build significant savings over time; avoid diminishing this superpower by withdrawing funds prematurely, if at all possible.

Want clarity? Start by getting pre-approved with Better so you can decide the right strategy for you.

See if a HELOC or home equity loan is right for you

*Disclaimer: This article is not intended as personalized financial advice.

¹ Betsy evaluates loan scenarios using currently available data across participating investors, product types, loan terms, and rate assumptions. The stated number of scenarios reflects a mathematical combination of these inputs (including multiple investors, product categories, loan terms, and rate variations) and does not represent a guarantee that all scenarios are available to every borrower or that any specific rate or loan will be offered. Actual loan options, rates, and terms depend on individual borrower qualifications, credit profile, property characteristics, loan amount, market conditions, and lender requirements at the time of application.

² Better Mortgage’s One Day HELOC promotion offers qualified customers who provide certain required financial information/documentation to Better Mortgage within 4 hours of locking a rate on a HELOC loan the opportunity to receive an underwriting determination from Better Mortgage within 24 hours of their rate lock. The underwriting determination is subject to customary terms, including fraud and anti-money laundering checks, that take place pre-closing and which may trigger additional required documentation from the customer. Better Mortgage does not guarantee that initial underwriting approval will result in final underwriting approval. See One Day Heloc Terms and Conditions.