What You’ll Learn

The major differences between FHA and Conventional loans

Advantages and risks for each loan type

Step-by-step guidance to determine which loan is right for your situation

When it comes to shopping for a mortgage, the two most common loan types you’ll see are FHA loans and Conventional loans. That is, unless you happen to be a veteran or you’re buying property in an agricultural zone.

Both FHA and Conventional loans have advantages and risks, and each is optimized for a specific set of circumstances. Depending on your unique situation, one is likely a better fit than the other.

But how to choose? This article will outline the key differences between the two, and offer step-by-step guidance to help you decide which type of loan is the best fit for you.

How FHA and Conventional loans are different

Loan insurers

The first major difference is who insures the loan. FHA loans are insured by the Federal Housing Administration (hence “FHA”), meaning that the government will step in and reimburse the lender in the event a borrower defaults on the loan. Conventional loans have no such guarantee from the government.

As a result, qualifications for FHA loans tend to be more open than Conventional loans, because lenders know the government stands behind the loan. However, FHA loans tend to carry slightly higher mortgage insurance costs for the borrower. These insurance premiums help to ensure the government is able to continue to provide backing for the loans without drawing too heavily on taxpayer dollars.

Availability

The second differentiator has to do with what lenders are able to issue which types of loans. Most lenders are happy to issue Conventional loans, which are the most straightforward and are considered the “safest” type of loan from the lender’s point of view. Not all lenders, however, offer FHA loans, which require a bit more due diligence and proven track record on the part of the lender. (Better Mortgage is happy to offer both loan types to qualified borrowers).

Property type

A major consideration when choosing between FHA and Conventional is whether or not the property you’re buying is going to be your primary residence. FHA loans are only available for primary residence properties, whereas Conventional loans are available for secondary (or vacation) homes and investment properties (including rentals and pure land holdings).

Qualifications

Because FHA loans are backed by the government and Conventional loans are not, the qualifications for each loan type look different.

Generally, FHA loans are easier to qualify for. They allow for lower income, lower credit scores, and a higher debt-to-income ratio (meaning they allow you to carry more debt relative to your income). The tradeoff for FHA loans is that they therefore carry slightly higher mortgage insurance premiums to offset risks.

Conventional loans, on the other hand, tend to be slightly more strict in their qualifications. They require slightly higher income thresholds, slightly better credit (although Better Mortgage has identical credit minimums of 580 for both FHA and Conventional loans), and slightly lower debt-to-income ratios. The benefit for borrowers who meet these tighter requirements, however, is lower (or, in some cases, no) insurance premiums on the loan.

Mortgage insurance

As mentioned above, mortgage insurance premiums differ significantly between loan types. This is worth unpacking in more detail.

FHA loans require a Mortgage Insurance Premium (MIP). This is broken up into two parts: A single up-front premium (Up-Front Mortgage Insurance Premium, or UFMIP), which is always 1.75% of the loan amount regardless of qualification factors; and an annual MIP payment that is built into your monthly mortgage payment and is based on the amount of your initial down payment. For example, if your down payment was between 3.5% and 5%, your annual MIP would be 0.85% of the loan amount divided into 12 monthly installments; whereas if your down payment was greater than 5%, you would pay 0.80% of the loan amount divided into 12 monthly installments.

Mortgage insurance for Conventional loans is called Private Mortgage Insurance or PMI. Generally, Conventional loans have a broader range of scenarios for mortgage insurance requirements. If you can afford a down payment of 20% (or more), you won’t need to pay any PMI premium on your loan. For anything less than 20% down, you’ll pay PMI at a rate that’s determined by factors like your credit score, loan-to-value (LTV) ratio, and debt-to-income (DTI) ratio. Conventional loans can be issued with down payments as low as 3%, and a major advantage of Conventional is that the PMI premiums go away as soon as the amount you owe is less than 80% of the property’s assessed value, even if your initial down payment was less than 20%. This could happen by paying down your mortgage over time, and/or by your property’s value rising over time to push your LTV over the threshold.

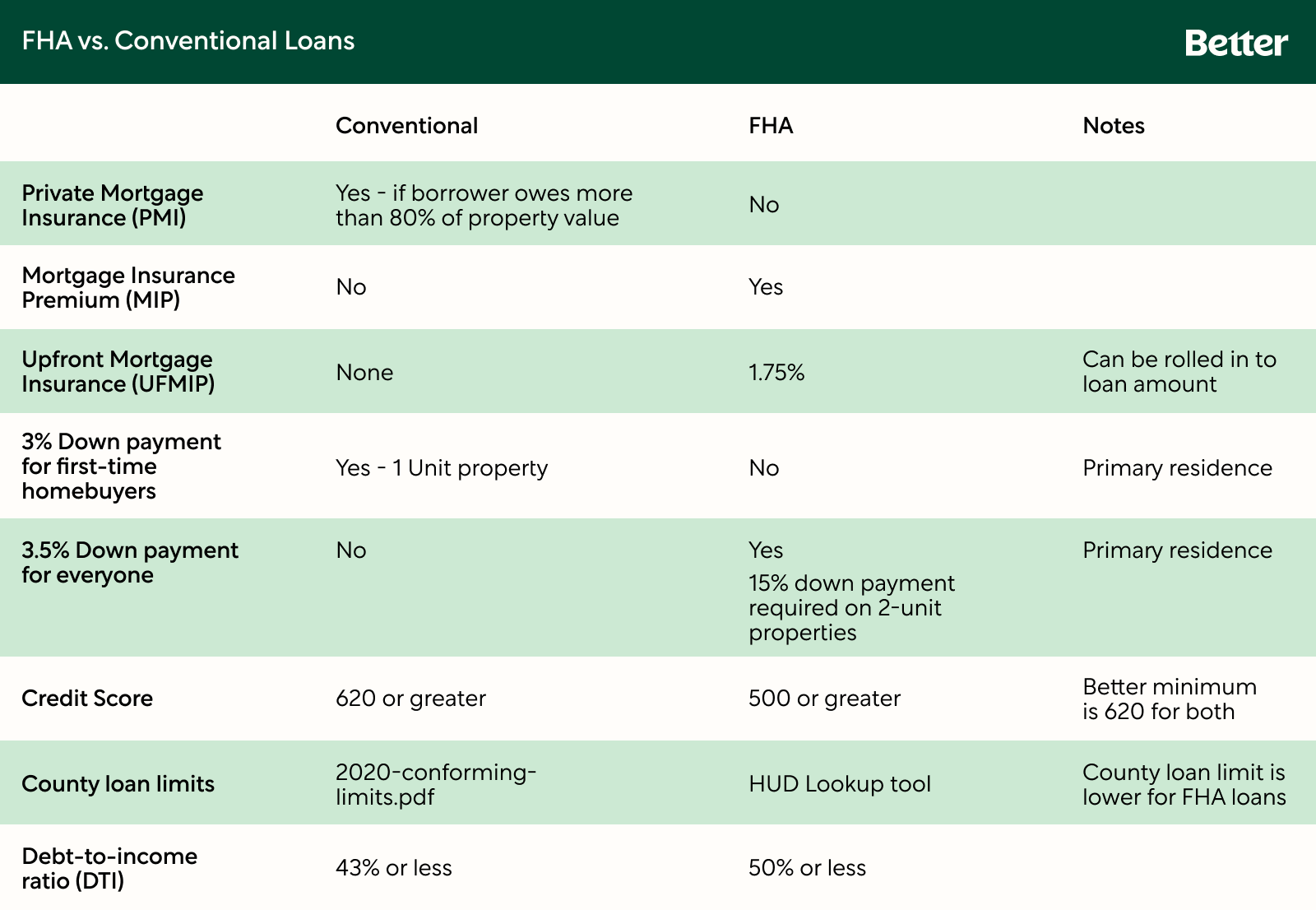

FHA vs. Conventional Comparison Chart

For a quick comparison of features, advantages, and requirements of each loan type, see the comparison chart below:

Step-by-step guide to choosing between FHA and Conventional

Ready to get started with the mortgage process, but still not sure which loan type is right for you? We’ve broken down the decision-making process into a few steps that should help you go the right route for your situation.

Step 1: Determine these three key numbers

First up, get a solid understanding of where you stand with these three things:

Your credit score:

Often, lenders (like Better Mortgage) will run a soft credit check as part of the pre-approval process. This will tell you your score without impacting your credit. Conventional loans require a minimum credit score of 580, while FHA loans have a lower base limit of 500. (Better offers both loan types with the same minimum score of 580.)

Your debt-to-income (DTI) ratio:

This is the proportion of your monthly income that’s already spoken for by payments you owe to creditors. For a deeper dive and how to calculate this number for yourself, read our complete DTI guide.

Your affordability range:

It can be hard to understand exactly how a home’s list price translates to a monthly payment. To get an accurate picture of how much house you can afford, we recommend using an affordability calculator. You’ll plug in your zip code, annual gross income, available assets, and credit score, and the calculator will give you an estimated homebuying budget.

Step 2: Determine your loan amount

Usually, this means finding a home that fits into your homebuying budget as determined above. In some cases, though, you could calculate your loan to include the price of the home plus some renovation expenses. Or, if you have significant assets for a down payment, your loan amount could be well below the home’s list price. In any case, you’ll want to get a solid idea of exactly how much money you’re looking to borrow. This is important because Conventional loans have higher limits on how much you can borrow than FHA loans.

Step 3: Determine your down payment

Based on the amount you’re looking to borrow, calculate how much you can comfortably afford for your down payment. It’s possible to take out a Conventional loan with as little as 3% if you’re buying your first home, but the ideal number to shoot for is 10% or more for a Conventional loan (and keep in mind that 20% or more will waive your mortgage insurance premium). FHA loans offer down payments as low as 3.5%, so if you have less than 10% available, you’ll have an easier time going with FHA.

Step 4: Compare your monthly costs

This will include principal, interest, mortgage insurance premium (if any), homeowner’s insurance premium, and property taxes. If you haven’t already, this could be a good time to get pre-approved, since that will give you the most accurate picture of your exact monthly costs for the loan you want to take out. Since pre-approval doesn’t impact your credit, you can get pre-approved for both loan types (with Better it takes about 3 minutes!) to get a clear comparison.

Step 5: Compare closing costs

Generally, closing costs are similar between FHA and Conventional loans, but an important thing to consider is that FHA loans universally require an upfront Mortgage Insurance Premium payment of 1.75% of the loan amount. On a $300,000 loan, that’s over $5,000—so it’s worth considering. However, closing costs can be rolled into the loan amount for both FHA and Conventional loans, which helps prevent surprise large bills—just make sure you take that into account when you’re calculating your monthly costs (step 4).

Step 6: Get pre-qualified and lock your rate!

Based on the 5 steps so far, you should have a pretty strong leaning toward one loan type over the other. If you still haven’t gotten pre-approved, now may be the time. If you have, it’s as simple as choosing your preferred loan type and taking the process one step further to lock your rate and get your pre-approval letter. Rates generally fluctuate according to the market for both FHA and Conventional, so that usually won’t be a major determining factor.

Ready to take the next step?