What you’ll learn

— What FHA MIP refunds are and why they exist

— How the FHA MIP chart works month by month

— Who qualifies for a refund when refinancing

— How to calculate your potential refund

Wondering how much of your FHA mortgage insurance premium (MIP) you could get back? The FHA MIP refund chart is your roadmap. It breaks down your payments and the amount you can recover.

Read on to learn about how the MIP refund chart works and what factors to consider when calculating your potential return.

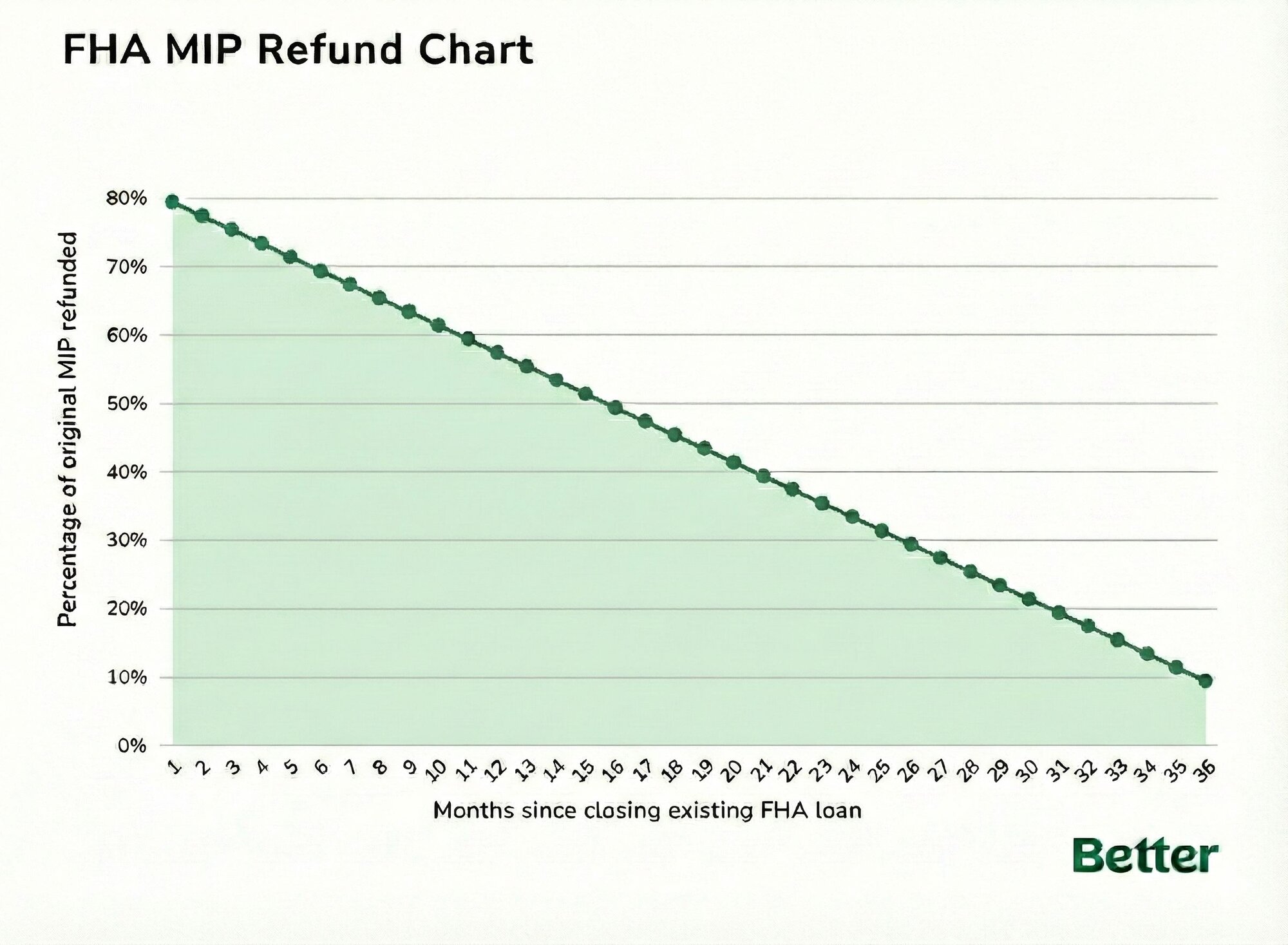

Data from HUD guidelines - My Mortgage Insider

What’s an FHA MIP refund, and how does it work?

A mortgage insurance refund comes from the up-front mortgage insurance premium (UFMIP) you paid when you first took out your FHA loan.

A mortgage insurance refund comes from the UFMIP you paid when you first took out your FHA loan. It equals 1.75% of your base loan amount. Borrowers cover this cost at closing or roll it into the loan balance.

Part of this premium may be refundable if you refinance into another FHA mortgage. You generally need to refinance within three years to receive the full refund. If you switch loans within the first 12 months, though, you could get back roughly 58% of your up-front premium. The refund gradually decreases as the years go on, dropping to 10% by the three-year mark.

That’s why acting so quickly can make a real difference. With Better, you can take advantage of government-backed loan options and a fast pre-approval process. This makes it easier to see your rate and plan your FHA refinance quickly.

...in as little as 3 minutes – no credit impact

What is the FHA MIP chart? 2026 numbers

FHA uses a standard refund schedule nationwide. The following percentages show how the credit changes month over month:

— Month 1: 80% refund

— Month 6: 70% refund

— Month 12: 58% refund

— Month 24: 34% refund

— Month 30: 22% refund

— Month 36: 10% refund

FHA MIP eligibility requirements

Not every borrower can get a refund. To qualify, your current FHA mortgage must:

— Be less than 36 months old at refinancing

— Have no foreclosures or serious delinquencies on record

— Not be an assumed FHA loan

Keep in mind that you must refinance into another FHA loan to receive the refund. Refinancing into a conventional mortgage, for instance, won’t unlock an FHA MIP refund.

...in as little as 3 minutes – no credit impact

How to calculate your FHA MIP refund

The MIP refund calculation is simple to do once you understand three factors:

— Your original UFMIP amount (typically 1.75% of the loan you closed on)

— Months elapsed since your closing date

— Refund percentage from the FHA chart for that month (applies only to the up-front MIP)

From there, you can figure out your refund by multiplying:

Refund amount = Original UFMIP x Refund percentage

Refund example

If you borrowed $200,000 on your original FHA mortgage, the original UFMIP was:

$200,000 x 1.75% = $3,500

Refinancing in month 25 qualifies for an approximate 32% refund. That gives you:

$3,500 x 32% = $1,120

This $1,120 works as your up-front mortgage insurance premium refund. This is then credited toward the MIP owed on your new FHA mortgage.

Requesting FHA MIP refunds

You don’t need a separate form or request to get this benefit. If you stay with the same lender, they will automatically apply your FHA insurance refund to your new up-front MIP. Switching? The new company will calculate the refund using your FHA-insured loan, so it still counts toward your mortgage.

What to consider with FHA mortgage insurance premium refunds

Before figuring out your refund, consider these key factors:

— Mind the timing: Each month that passes reduces your refund, so even a small delay in your refinance timeline can make a difference.

— Check your up-front MIP: The refund offsets it, but doesn’t remove it entirely.

— Refinance to conventional wisely: Switching to a conventional loan won’t trigger an FHA refund, but it can help you remove mortgage insurance faster if you have enough equity.

— Weigh total savings: The refund helps, but your interest rate, closing costs, and long-term plans also impact whether the refinance makes financial sense.

Make your refinance work for you with Better

An MIP refund can lower the FHA up-front fee of your new FHA loan. Timing, the age of your current loan, and your eligibility are the biggest factors. Understanding the refund chart — and how much of your up-front MIP might carry over — helps you compare refinance paths.

Better’s digital tools make that process simple. You can check refinance rates, run the numbers with our refinance calculator, and get pre-approved in as little as three minutes.

Try Better today and see how much you could save.

...in as little as 3 minutes – no credit impact

FAQ

Can you get your up-front MIP back when moving from an FHA loan to a conventional loan?

You won’t qualify for a refund if you switch from an FHA to a conventional loan. Up-front MIP is only refundable when you refinance into another FHA loan within 36 months.

How is an up-front mortgage insurance premium refund calculated?

Your refund depends on the up-front MIP you paid and how many months have passed since closing your FHA loan. The chart assigns a percentage for each month from one through 36. Lenders apply that number to your original loan amount to determine the refund amount.

Who qualifies for an FHA MIP refund when refinancing FHA to FHA?

Borrowers refinancing an existing FHA loan to a new FHA loan qualify. You must have paid the up-front MIP on the original loan. The lender automatically applies the refund to your new loan.

How can I calculate my FHA MIP refund when I refinance?

Start with your original loan amount and upfront MIP. Apply the refund percentage based on how many months you’ve held the loan. Subtract that amount from the new loan’s upfront MIP.