What You’ll Learn

What is an escrow account?

The types of escrow accounts in real estate and when they apply

How escrow accounts can protect home buyers, sellers, and owners throughout the real estate and mortgage process

Important rules and regulations regarding escrow accounts

If you’re in the process of buying or selling a house, you’ve probably heard the term “escrow account” pop up a few times. But what is an escrow account, and why do you need one?

What is an escrow account?

The word escrow has French origins (ooh la la) and refers to putting a sales agreement into the trust of a neutral third party until the transaction is completed. In the world of home buying, escrow accounts are still commonly established to protect the financial interests of buyers, sellers, and any other parties involved in a purchase sale or refinance. In many cases, escrow also comes into play after a mortgage is finalized.

Here’s a quick breakdown on what you should know about the escrow process (often simply referred to as “escrow”) if you’re buying or refinancing a home:

Types of escrow accounts and how do they work

When it comes to real estate, there are two main types of escrow accounts: one is used to safely hold money during home purchase and refinance transactions, and the other is used throughout the course of a mortgage to manage payments for things like property taxes, homeowner’s insurance, and mortgage insurance premiums.

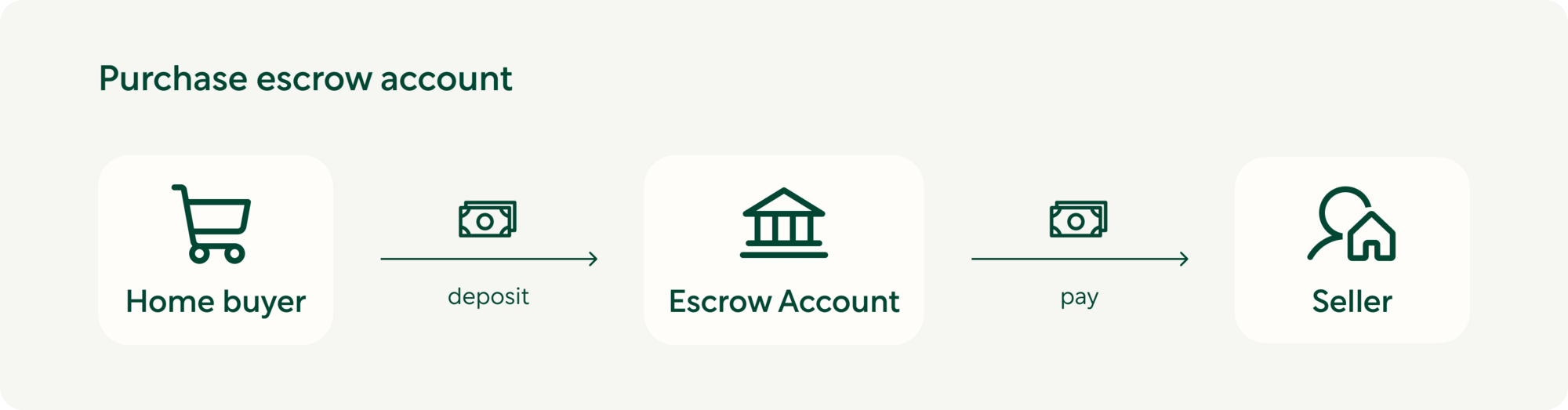

Purchase escrow accounts

You’ll typically first hear about an escrow account after you make an offer on a home and present an earnest money deposit. The purpose of an earnest deposit is to assure the seller that you’re serious about buying their home, so they can feel confident taking it off the market. However, before any money officially changes hands, certain conditions must be met. That’s where the escrow account and escrow agreement comes into play.

To protect all parties involved in the transaction, money will be deposited into an escrow account for safekeeping. This account is created and managed by a neutral third party, known as the escrow agent. Depending on where the home is located, the escrow agent can be a participating broker, a title company, an escrow company, or a real estate attorney.

Beyond the earnest money deposit, escrow accounts may also hold other mortgage-related funds, such as:

— Real estate fees or commissions to agents

— Loan fees to the mortgage lender

— The down payment for the home

— Third-party payments for things like inspections and appraisals

— Seller’s profit from the transaction

— Property tax assessments

— Lienholder payoffs

Not only does this ensure all parties are properly compensated at closing, it also protects buyers and sellers from potential loss which is a good idea for big transactions such as a home purchase. Another key benefit of escrow accounts is that they protect your money until all agreed-upon conditions are fulfilled by both parties; these can range from property inspections to appraisals to repairs. Purchase transactions can fall “out of escrow” if either the buyer or the seller fails to uphold their end of the bargain. Since escrow accounts are maintained by neutral third parties, it’s easier to ensure that large lump sums (such as down payments) will be returned to you without issue. Note: earnest money can sometimes be the exception to this rule, so check the terms of your deposit before putting anything in escrow.

Refinance escrow accounts

When you refinance your mortgage, you’ll use an escrow account to deposit money for things like appraisal fees and attorney fees. In the case of a cash-out refinance, loan proceeds (aka, the money you make from refinancing) will also be held here. If your old loan had an escrow account, it will be closed by your new escrow agent and any remaining funds in there will be returned to you. Once you finalize the terms of your new loan agreement, money will be distributed to the appropriate parties at closing. The distributions may include broker fees or commissions; appraisal, pest and inspection fees; or any cash out to the borrower.

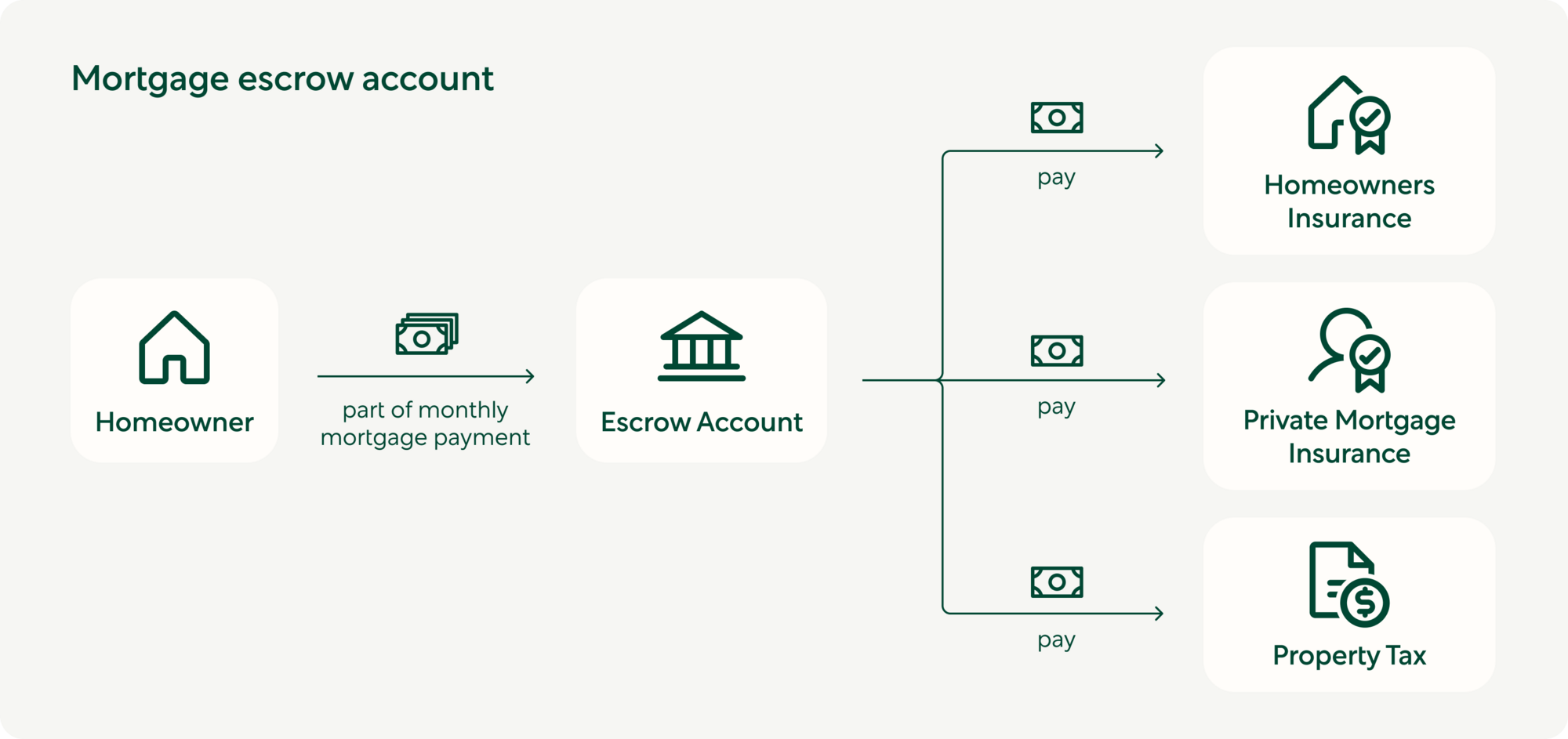

Mortgage escrow accounts

Your servicer may require you to keep an escrow account after closing. Unlike a bank account that's in your name, an escrow account is opened and managed entirely by your mortgage servicer. All you need to do is make your monthly mortgage payments, and a portion will automatically deposit into your escrow account.

The amount that goes into escrow each month depends on the total supplemental costs associated with owning your home, such as your property taxes, homeowner’s insurance, and, if applicable, private mortgage insurance (PMI). Rather than paying these separate costs as they arise, your mortgage servicer can disburse payment on your behalf from your escrow account.

Escrow accounts are useful because they guarantee that you’ll allocate money each month to cover tax and insurance costs throughout the year. They also make it possible for you to spread these large expenses out over time—rather than in inconvenient lump sums. For instance, instead of paying a large property tax bill 4 times per year, it will be incorporated into your mortgage payments and divided over the course of 12 months. This way, you can set it and forget it!

How does an escrow account work?

Before you close on your mortgage, you will receive your Closing Disclosure, which will detail the full cost of your home loan—including the terms, projected monthly payments, fees, and cash to close. As part of your projected payments, you’ll see your monthly escrow charges for taxes, insurance, and other costs required.

In Section G of this document, you will also find your initial escrow payments. Your lender will collect this amount as part of your closing costs and use it to establish your escrow account. It’s usually enough to cover the first few months of payments. but your exact initial escrow costs may vary depending on the time of month you close and when your first property tax and insurance bills are due.

Each time you make a mortgage payment, a portion earmarked for taxes and insurance will be funneled into the escrow account for your upcoming bills. These costs will be a separate line item on your mortgage statements. When your property taxes or insurance payments come due, the loan servicer will use that cash reserve to pay those bills on your behalf.

Is escrow required for my mortgage?

An escrow account is required when closing on a home purchase or refinance to protect the buyer, seller, and all other third parties during the transaction. However, a mortgage escrow account may be optional—it depends on your loan-to-value ratio (LTV) and the type of loan you obtain. For example, FHA loans require a mortgage escrow account for the life of the loan, but the rules for conventional loans are different.

Mortgage escrow accounts are also usually mandatory for homebuyers with LTVs greater than 80%. If you put less than 20% down on your home, then this will likely apply to you. However, when your ratio falls below that 80% LTV threshold (either because you paid down your mortgage, your property value increased, or both) keeping your escrow account becomes optional. At that time, you could contact your lender or loan servicer to request the escrow account be eliminated.

Should you escrow taxes and insurance?

Some homeowners prefer to keep an escrow account for the convenience it offers—it doesn’t get much easier than automatic payments handled by other people. If you’d rather not worry about having to pay extra bills, or if you’re unsure whether you have the financial discipline to set aside money to pay these larger expenses when they come due, then it might make sense to let your mortgage servicer continue making the payments for you.

If your loan permits it and you choose to make insurance and property tax payments on your own, you may have to pay a fee (around .25% of your loan amount) to waive escrow at closing. Remember, escrow gives your lender peace of mind that your home is always insured and your property tax payments stay up-to-date. The waiver fee offsets the additional risk your lender takes on when they don’t have visibility on those payments.

Escrow account rules and requirements you need to know

The Truth in Lending Act and the Real Estate Settlement Procedures Act guide many of the regulations around escrow accounts, specifically those that are used to hold insurance and tax payments for homeowners. These rules give transparency into the management of escrow accounts and protect homeowners from being charged excessively.

Escrow cushion

Some loan servicers may require you to maintain an escrow cushion. This means they’ll ask you to keep extra money in your account to cover unanticipated payment fluctuations such as tax spikes or insurance premium increases that can arise throughout the year. However, the cushion can’t exceed more than one-sixth of the total amount paid out of the account each year (roughly equivalent to 2 months of payments.)

Annual escrow statements and adjustments

Your loan servicer is required to send you an annual escrow statement that details your account history and activity for the year. The servicer must also conduct an account analysis to determine if a surplus, shortage, or deficiency exists, and notify you of its findings. If the servicer determines they’ve collected too much on your behalf, they’ll either have to issue you a refund or lower the escrow payments for the following year to offset the extra funds. If your escrow balance isn’t enough to cover upcoming tax and insurance costs, you might need to make a one-time payment or increase your future mortgage payments to make up for the difference.

Escrow account closure

As a general rule, you can request that your escrow account be closed after you hit 80% LTV. (Some states have a different threshold—for example, in California you can choose to waive escrow if your LTV is 90% or lower.) Higher-priced mortgage loans (HPMLs) are an exception to the rule. If you have a HPML, it means the annual percentage rate (APR) on your loan significantly exceeds the average prime offer rate (APOR). In other words, the cost of borrowing the money for your loan is higher than the industry average. HPMLs are subject to Regulation Z, which requires an escrow account remain active for at least 5 years or until the loan is paid off.

More questions about escrow? We can help.

Whether you're buying a home, refinancing, or already in the process of paying your mortgage, escrow accounts are meant to offer you financial protection. Understanding how they work and what benefits they offer can give you peace of mind during the closing process and when you start making your first loan payments.

At Better, we’re here to streamline the process from beginning to end. Get pre-approved in as little as 3 minutes with Better Mortgage.

This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.