Mortgage affordability calculator

How much house can I afford?

Our home affordability calculator estimates the maximum home you can afford – including taxes, PMI, and real-time mortgage rates – based on your income, assets, and monthly debts. Enter your info to find out how much you can afford!

Calculating...

Ready for the next step?

Get pre-approved in as little as 3 minutes

Won’t affect your credit score

Home affordability calculator

Buying a home is an exciting milestone in anyone’s life, but determining how much house you can afford can be a daunting task. With so many factors to consider, it’s crucial to have the right tools and information at your disposal.

That’s where a home affordability calculator comes in handy. This powerful tool takes into account your financial situation, income, debt, and other key factors to help you determine how much you can afford to spend on a new home.

Let’s explore how our home affordability calculator works, what factors determine how much house you can afford, and how lenders evaluate your financial situation. Whether you’re a first-time homebuyer or looking to upgrade, understanding your financial limits is essential to make a smart purchase decision.

When it comes to determining how much house you can afford, using a home affordability calculator is a great place to start. This tool allows you to input information about your income, debt, and expenses to calculate an estimate of how much you can borrow for a home purchase.

How does a home affordability calculator help me?

By using a home affordability calculator, you can understand your estimated housing budget, evaluate different financial scenarios, and plan for homeownership within your means.

What factors determine how much house can I afford?

Determining how much house you can afford involves considering several important factors. These factors include upfront costs, income, debt-to-income ratio, credit score, down payment, and your interest rate. Understanding how these factors impact your affordability can help you make a more informed decision about how much home you can comfortably afford.

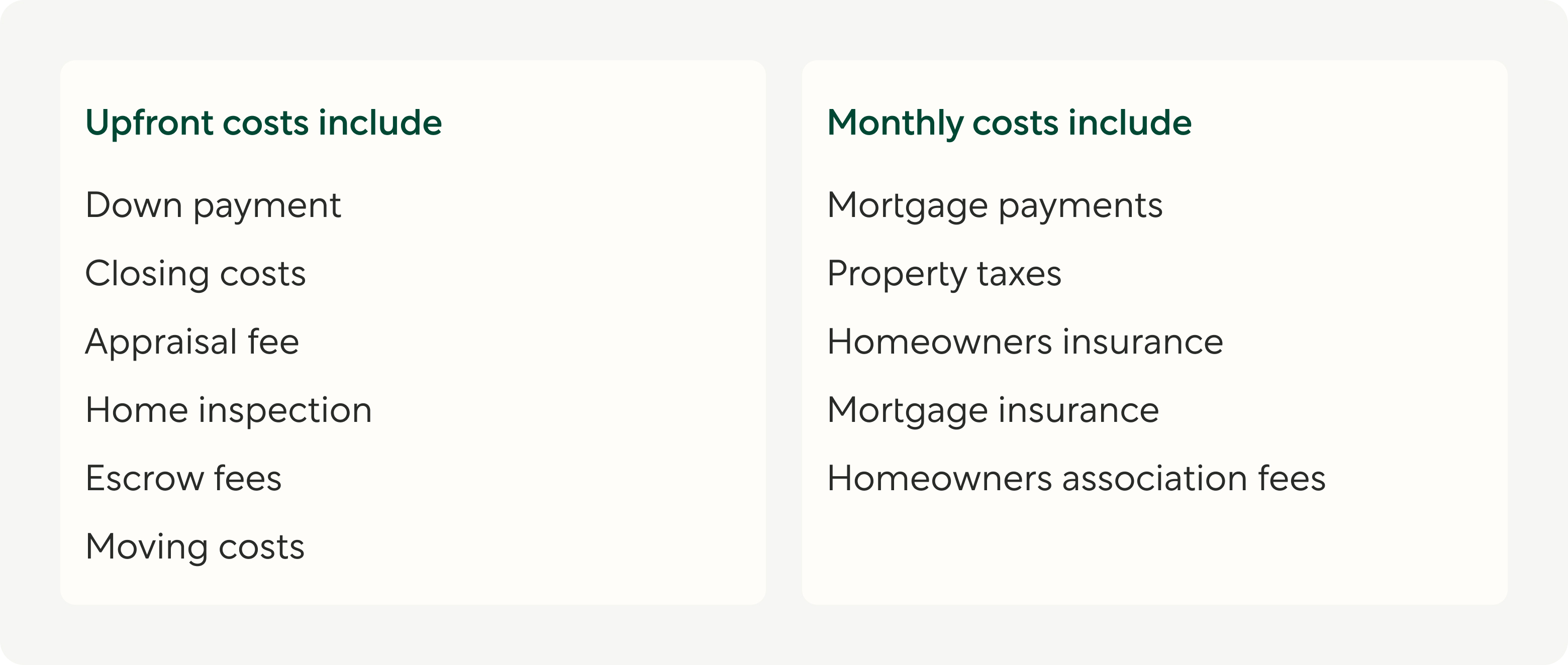

Upfront costs v. monthly costs

When determining how much house you can afford, it’s important to consider both upfront costs and monthly expenses. Upfront costs refer to expenses you pay at the time of purchase, while monthly costs are ongoing expenses that you’ll need to budget for.

Here’s how upfront costs compare to monthly costs:

Balancing upfront costs with monthly expenses is crucial in determining how much house you can afford. While you may be able to cover the upfront costs, ensuring that the monthly expenses fit within your budget is equally important.

Income

Your income plays a significant role in determining how much house you can afford. Lenders figure out your debt-to-income ratio by looking at how much of your income goes towards paying off debts. They use your monthly income, also called gross monthly income. Here’s how income impacts affordability:

Higher income:

- Allows for a higher debt-to-income ratio

- Provides more budgetary flexibility for mortgage payments

- May make it easier to afford a higher-priced home

Lower income:

- Limits the amount you can borrow

- Requires careful budgeting to ensure mortgage payments fit within your budget

Ultimately, having enough income is crucial for comfortably affording a home without financial strain. Lenders evaluate income to ensure mortgage payments are manageable and do not exceed a certain percentage of your monthly income.

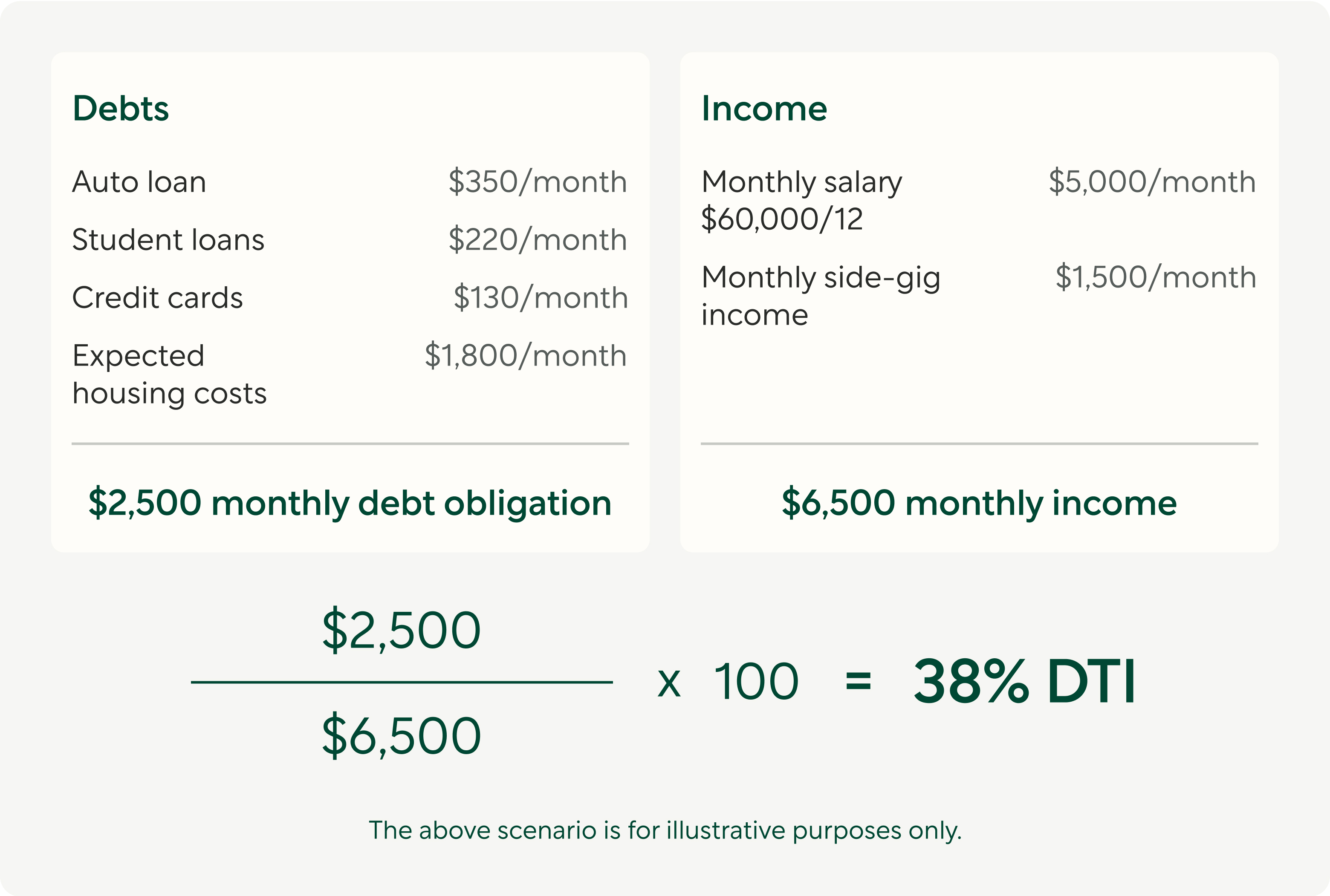

Debt-to-income ratio

Debt-to-income ratio, a crucial factor in determining your home affordability, compares your total monthly debt to your gross income. This ratio is used by mortgage lenders to assess your ability to manage monthly payments. By including all monthly debt obligations like credit card payments, car payments, and student loans, this ratio provides a clear picture of your financial situation.

A lower debt-to-income ratio indicates a healthier financial position, increasing the likelihood of qualifying for a mortgage with favorable terms.The maximum DTI you can have in order to qualify for most mortgage loans is often between 45-50%, with your anticipated housing costs included.

To calculate your DTI ratio, divide your monthly debt payments by your monthly gross income and multiply by 100. For example, if you pay $2,400 toward your debt and earn $8,000 each month, your DTI ratio is 30%.

Understanding and managing your debt-to-income ratio is essential in estimating how much mortgage you can comfortably afford within your price range.

Credit

When considering how much home you can afford, your credit score plays a crucial role. Lenders will assess your credit history, including credit card payments and total monthly debt, to determine your creditworthiness. A good credit score not only opens up more options for loan programs and lower mortgage rates but also helps you qualify for a higher purchase price.

On the other hand, a lower credit score may result in the need for a larger down payment, higher interest rate, or private mortgage insurance. Therefore, understanding your credit and taking steps to improve it can significantly impact your ability to afford the home of your choice.

Down payment

Your down payment is the amount of money you pay upfront toward purchasing your home on closing day. Saving for a down payment is crucial when buying a home, as it impacts the purchase price and loan amount.

Lenders typically require a minimum down payment to secure a mortgage loan. Depending on the type of mortgage you take out, down payments typically range from 3% to 20% of the sale price. For example, if you buy a $300,000 house and need to put 3% down, your down payment will be $9,000 (and at 20% down, it would be $60,000).

Your down payment reduces the principal balance of your mortgage, which lowers your required monthly payment. As a result, you may be able to afford a more expensive home if a large down payment brings your monthly housing expense in line with your budget. Plus, making a significant down payment could result in a lower interest rate, which may also allow you to buy a higher-priced property.

There are options for those making lower down payments, such as Federal Housing Administration (FHA) loans or Veterans Affairs (VA) loans. These alternatives can help buyers with limited funds achieve homeownership.

That said, a higher down payment can result in a lower loan amount, which may lead to more favorable mortgage rates and eliminate the need for private mortgage insurance

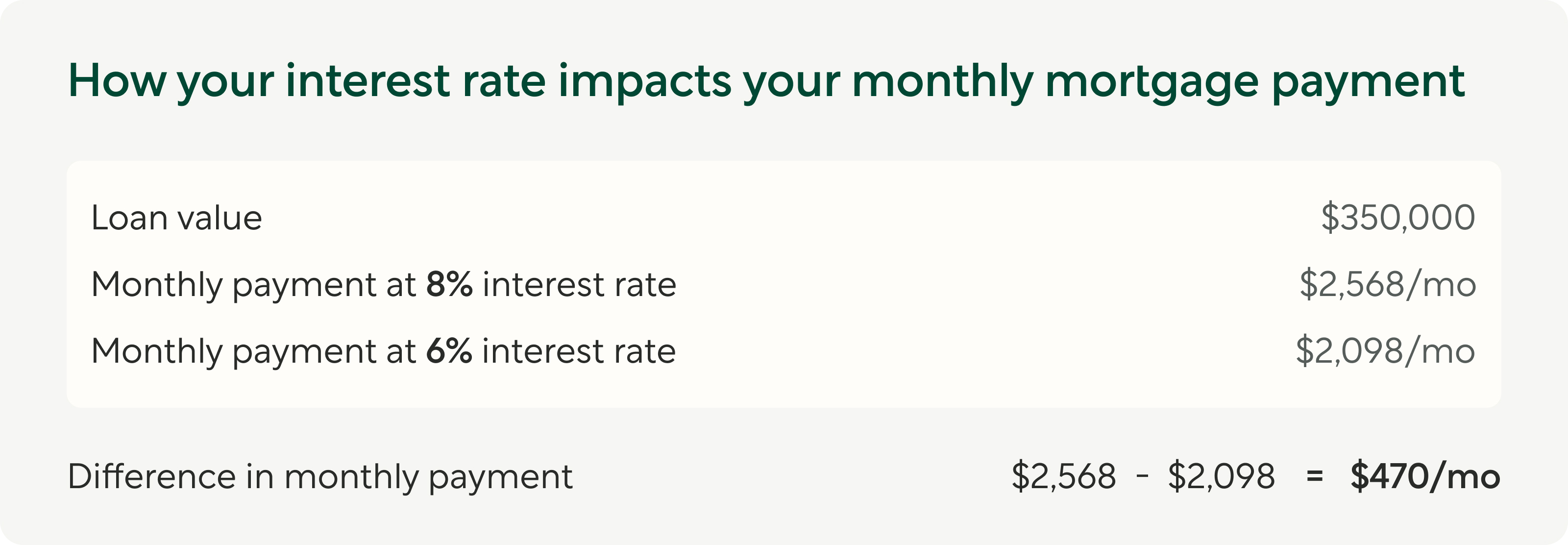

Your interest rate

When considering how much home you can afford, your interest rate plays a crucial role in determining your monthly mortgage payments. A higher interest rate can significantly increase your total monthly debt, affecting your budget and affordability.

Understanding the impact of your interest rate is essential, as it influences the overall cost of your real estate purchase. The market, as well as your credit score, loan amount, and loan term can affect the interest rate offered by your mortgage lender. Therefore, being aware of how your interest rate affects your mortgage payments can help you make informed decisions when exploring homes within your price range.

How does my income impact how much house I can afford?

Your income plays a crucial role in determining how much house you can afford. Lenders use your income to calculate your debt-to-income ratio, which helps them assess your ability to make monthly mortgage payments. The higher your income, the more home you may be able to afford.

How does my debt-to-income ratio impact how much house I can afford?

Your debt-to-income ratio (DTI) plays a crucial role in determining how much house you can afford. Lenders calculate your DTI to assess your ability to handle additional debt. A lower DTI indicates more room in your budget for a mortgage, while a higher DTI suggests potential difficulty in making payments. It’s important to keep your DTI within the acceptable range set by lenders.

Formula for calculating your debt-to-income (DTI) ratio

Here’s an example of what calculating your DTI might look like:

How does my credit score impact how much house I can afford?

Your credit score indicates your creditworthiness to lenders and affects the interest rate you may be offered. A higher score can lead to lower interest rates, potentially allowing you to afford a more expensive property. Conversely, a low credit score may result in higher interest rates or even mortgage application denial.

How does my down payment impact how much house I can afford?

Your down payment plays a significant role in determining how much house you can afford. It is the upfront amount you pay on closing day and can range from 3% to 20% of the sale price. A larger down payment reduces your mortgage balance, lowers your monthly payment, and may even result in a lower interest rate, allowing you to potentially afford a more expensive home.

How does my mortgage interest rate impact how much house I can afford?

Your mortgage interest rate plays a significant role in determining how much house you can afford. A higher interest rate means higher monthly payments, which can reduce the amount of mortgage you qualify for.

On the other hand, a lower interest rate can increase your purchasing power and allow you to afford a more expensive home. Your mortgage rate directly impacts your monthly budget and potential homeownership options.

How do lenders determine how much house I can afford?

Lenders assess various factors such as income, debt, expenses, credit score, and payment history to determine the amount of house you can afford. They use financial ratios to evaluate your loan repayment capabilities and consider your financial stability and creditworthiness.

How much monthly mortgage payment can I afford?

To determine your monthly mortgage payment, consider your debt-to-income ratio (DTI) as a maximum. Ideally, you don’t want a mortgage payment – alongside any other recurring debts – to be more than 50% of your monthly income.It is also wise to have some cushion and have 3-6 months worth of savings to cover unexpected expenses or changes in income.

How is our home affordability calculator different?

Other online calculators use general rules of thumb to estimate how much house you can afford, like "you should never spend more than 43% of your income on a mortgage".

We take a different approach. Our home affordability calculator takes your information, checks the latest interest rates, and runs a quick automated underwriting process based on the thousands of combinations of loan products and rates that are available to our borrowers. This allows us to provide accurate estimations to give you the best insight into your buying power.

6 tips for buying an affordable home

You’ll need to go through several steps before buying a house. But, if you want to walk away with a mortgage that fits into your budget, here are six tips for buying an affordable home:

#1: Check your cash flow

You should first determine how a new mortgage would fit into your budget. So, take a close (and honest!) look at your current income and expenses. Then, if needed, brainstorm ways to earn more money or reduce your spending.

#2: Consider all mortgage and housing-related costs

Getting a mortgage means more than just a new monthly payment. You’ll want to consider all the upfront and ongoing costs that are associated with your mortgage and housing costs, too. When budgeting, you should factor in your down payment, closing costs, principal payment, interest on your loan, property taxes, and homeowner’s insurance. You may also have to factor in private mortgage insurance (PMI) or a homeowner’s association membership, depending on your situation.

#3: Improve your financial profile

It’s a good idea to strengthen your financial position as much as possible before applying for a mortgage. You can pay off debt, boost your credit score, or save more for a down payment. Taking a first-time homebuyer course may help you develop a strategy to improve your finances.

#4: Explore all of your mortgage options

Believe it or not, there are several types of mortgage loans available to homebuyers. You may want to explore conventional mortgages, FHA loans, and other government-backed financing options, like VA or USDA loans, to help determine which may be right for your situation. There are also many first-time homebuyer resources, which could reduce your upfront costs or help you more easily qualify.

#5: Choose a house you can handle

Being a homeowner means you can’t call a landlord to fix a broken water heater or bust pipe. Beyond the upfront costs and monthly mortgage payments, be prepared to cover home repairs and upgrades. You may also have to open up your wallet for furniture and decor. So, be sure to buy a house that you can afford to furnish and maintain.

#6: Stick to your budget

Buying a property might be a very emotional process for you. You may fall in love with a home, only to get outbid by another buyer. As much as it hurts, stay strong and stick to your budget. Otherwise, you could end up with a mortgage payment that you struggle to make. Our mortgage calculator can help you avoid borrowing too much.