What is a CEMA loan?

CEMA stands for Consolidation, Extension and Modification Agreement—and is essentially a way to refinance but avoid paying an expensive mortgage recording tax.

CEMAs are used instead of a traditional refinance but they accomplish similar refinancing goals—such as lowering the interest rate, changing the loan term, or accessing cash through the equity in the home (like a cash-out refinance). However, unlike a traditional refinance, the existing debt obligation (the loan you’re refinancing) is not satisfied and replaced with a new loan but rather modified into a new loan or a CEMA.

By opting for a CEMA as opposed to a refinance, you avoid paying the mortgage recording tax on your current loan balance by consolidating the new loan into the existing one. That means you would only pay the recording tax on the difference between the existing principal balance and the new loan amount.

The NY mortgage recording tax

New York State imposes a tax for recording a mortgage on property within the state. The recording tax applies to both purchases and refinances but excludes co-ops. It typically is about 1–2% of your loan amount, which can significantly increase your closing costs.

Homeowners who look to refinance their loans typically have to pay the mortgage recording tax. However, there is an alternative to refinancing that can significantly reduce closing costs and the tax burden—a CEMA loan.

For Example:

Mary owns a home valued at $1,000,000 and owes $200,000 on her mortgage. She wants to access $50,000 of equity from her home and wants to get a cash-out refinance, making her new loan balance $250k. Assuming Mary’s mortgage recording tax is 2%, with a CEMA she will be paying mortgage tax only on the $50k (or $1,000 in taxes). If she does a refinance, she’ll be paying mortgage tax on the entire new loan balance of $250k (or $5,000 in taxes).

How to get a CEMA loan

After you complete a refinance application with Better Mortgage, your application is automatically converted into a CEMA.

Prior to locking your rate, we encourage you to speak with your Loan Officer to confirm that a CEMA is right for you and evaluate your options.

Once you lock your interest rate, Better Mortgage’s bank attorney will reach out to you within ~3 business days to confirm any CEMA savings and determine if you’d like to proceed with a CEMA, thereby beginning the process.

Note: There is no additional cost incurred from switching between a CEMA and a refinance within the first week after locking and no impact to your interest rate depending on the product you choose.

Our bank attorney will send documentation to your current loan servicer for their review and approval, a requirement to obtaining a CEMA

Our bank attorney will be in touch with you once they hear back from your current lender on the CEMA approval status - about 2-6 weeks from submission (depending on your lender)

CEMA versus refinancing

There are two main considerations when deciding between a CEMA and a traditional refinance—cost and time.

Cost

At Better Mortgage, your Loan Officer will work with you to do a preliminary analysis to see if a CEMA or a refinance is more cost effective. Once your loan is locked, our bank attorney will get in touch with you to confirm any savings. If you change your mind after you lock, you’re able to go between CEMA and refinance at no cost.

Dependent on your existing lender fees for obtaining a CEMA, fees average ~$2,000. If the amount of savings on taxes significantly exceeds the cost of the CEMA fees, it may make sense to pursue a CEMA.

In areas where mortgage recording tax is high, such as New York City and the immediate surrounding area, a CEMA is usually more cost effective.

Time

A CEMA also comes with additional requirements, namely getting your current lender’s approval—which means more time is needed to close. A traditional refinance on average takes ~30 days to close whereas a CEMA usually takes ~75 days to close. If you’re in a hurry to refinance, it may make sense to bypass a CEMA.

Understanding the CEMA on your loan estimate

You can apply and lock a rate even if your current lender hasn’t approved your CEMA application. Until your CEMA is fully approved, the mortgage taxes will appear on your Loan Estimate as part of the Transfer Taxes under Section E. We keep the mortgage taxes on your Loan Estimate to ensure transparency on potential incurred costs until a final loan product is confirmed.

As a result, your Loan Estimate will show the full Mortgage Recording Tax (the amount you’d have to pay if you weren’t doing a CEMA) in Section E, p. 2 of your Loan Estimate under “transfer taxes.” This section bundles the mortgage recording tax, as well as other taxes you’re required to pay, regardless if you do a traditional refinance or CEMA.

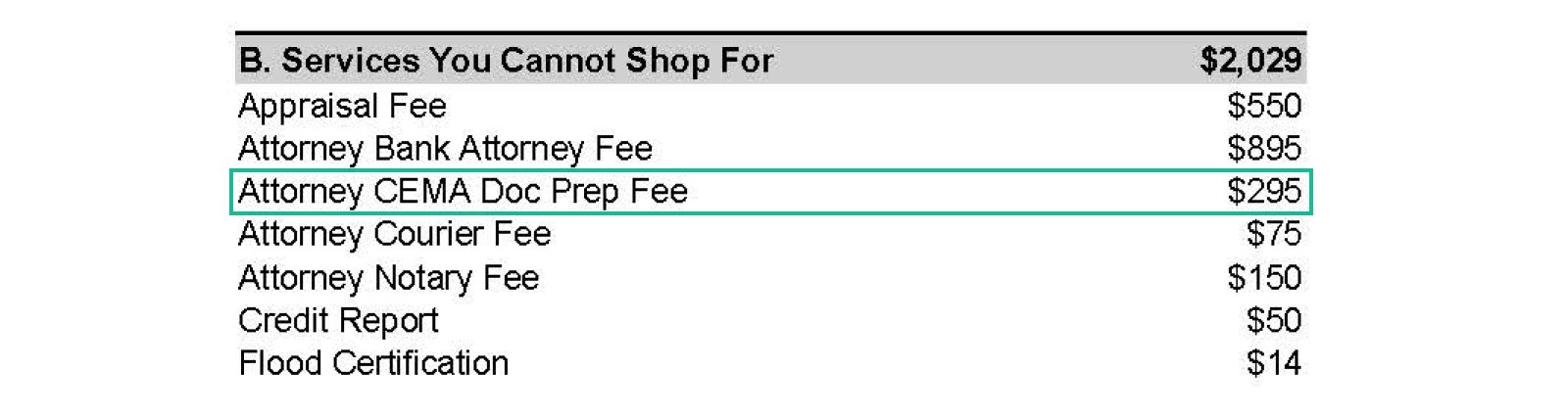

In addition to the mortgage recording tax, we also include the fixed CEMA fee under Section B, which represents the cost to execute the CEMA. You’ll see that the fee is not reflective of the total average amount (~$2,000) since a large portion will be paid directly to your lender—by you. A Better Mortgage bank attorney will help facilitate the payment to ensure a smooth and transparent process, but it will not be included on your Loan Estimate.

The Loan Estimates displayed above are for illustrative purposes only.

This means your Loan Estimate currently reflects some of the costs of the CEMA but does not reflect the benefits of a CEMA. You will not pay this cost if you do not end up getting a CEMA loan (and the associated reduction in your mortgage tax).

As soon as we confirm your CEMA has been approved, we will remove the mortgage recording tax from Section E, and your closing costs will reduce by that amount. Please note there are other fees bundled into “transfer taxes” so the entire “transfer tax” line item does not represent your potential savings. If you would like a better understanding of your potential CEMA savings, your Loan Officer will be able to provide a preliminary estimate, which will be confirmed by our bank attorney after you lock.

If your CEMA is not approved, Section E will remain the same but the CEMA fees from Section B will be removed, reducing your closing costs.

What happens if the CEMA is not approved?

In the event your CEMA is not approved, our team will help you achieve your refinancing goals via a traditional refinance. Our Loan Officers are here to walk you through this decision.

Why does Better Mortgage automatically opt me into a CEMA?

Better Mortgage is constantly looking for ways we can benefit our borrowers. Because CEMAs are typically more cost effective for borrowers than a traditional refinance, we automatically opt you in. As a result, we’re able to start the approval process with your existing lender quicker to determine the savings potential and give you a clear sense of time to close.

Can I opt out of a CEMA?

Yes, if you’d prefer to opt out, let your Loan Officer know.

Ready to find your perfect home in New York?

Get pre-approved in as little as 3 minutes when you apply for a loan on better.com. And if you’re on the hunt for the right property, Better Real Estate is here to help—plus, you can save on closing costs when you work with one of our agents.

This publication is designed to provide general information. It is not intended to provide, and should not be relied upon, for tax, legal or other financial advice.