Rates are daily averages based on Better Mortgage data, not APRs, and vary by borrower.

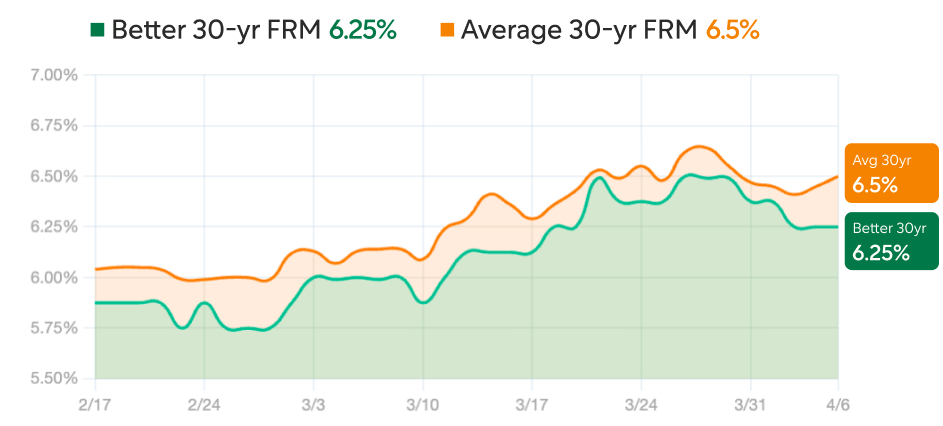

Mortgage rates are moving higher on June 9, 2026, extending a two-day rise that started after Friday’s stronger-than-expected jobs report pushed the 30-year fixed rate sharply upward. Based on current mortgage rates, the 30-year fixed mortgage rate sits at 6.66%, near its highest level in the past nine months. The 15-year fixed rate is at 6.13%, and the 5/1 ARM is running approximately 6.26%.

For homeowners exploring a refinance, the 30-year fixed refinance rate is around 6.72% and the 15-year refinance rate is approximately 6.10%. See today’s refinance rates at Better.

Two forces are driving rates right now: a labor market that keeps outperforming expectations, and ongoing geopolitical uncertainty tied to the Iran conflict, which is creating volatility in the bond market. The next major data point arrives Wednesday morning — the Consumer Price Index report — which could move rates meaningfully in either direction.

Today’s mortgage rate snapshot

Here’s where current mortgage rates stand as of June 9, 2026, based on current market data:

| Loan type | Average rate |

|---|---|

| 30-year fixed | 6.66% |

| 15-year fixed | 6.13% |

| 5/1 ARM | 6.26% |

| 30-year fixed refinance | 6.72% |

| 15-year fixed refinance | 6.10% |

These are national averages — your actual rate depends on your credit score, down payment, loan amount, and lender.

...in as little as 3 minutes — no credit impact

Use Better’s mortgage calculator to see what today’s rates mean for your estimated monthly payment.

What’s moving rates today

Two overlapping pressures have pushed rates to their current level.

The jobs report

May’s employment data came in well above expectations, which typically signals a stronger economy. This is good news for workers, but it puts upward pressure on interest rates. When the economy is running hot, bond investors demand higher yields to offset the risk of inflation, and mortgage rates follow the bond market. Friday’s report added 0.08% to the 30-year fixed rate in a single session; Monday added another 0.02%. The latest industry rate data puts today’s level at the third highest of the past nine months.

Understanding why mortgage rates are going up comes down to the relationship between the labor market, inflation expectations, and the 10-year Treasury yield, the benchmark that most closely tracks 30-year fixed mortgage rates.

The Iran conflict and bond market volatility

Geopolitical uncertainty has been a recurring factor in mortgage rate movements since early 2026. The Iran war has driven periods of oil price spikes and safe-haven flows into Treasury bonds. This tends to pulls rates lower. When those flows reverse, rates bounce back. Today’s rate environment reflects a market still calibrating the risk premium from ongoing conflict. According to recent market commentary, war-related headlines were the primary non-data driver in bond markets this week.

Wednesday: the CPI report

The Consumer Price Index for May will be released Wednesday morning, and it’s the most consequential near-term data point for mortgage rates. A hotter-than-expected inflation reading would likely push rates higher; a softer number could offer some relief. The Federal Open Market Committee meets June 16–17, and Wednesday’s CPI will influence expectations for that meeting. The federal funds rate is currently at 3.50%–3.75%, with the FOMC holding steady at its last meeting in April.

What today’s rates mean for homebuyers

At 6.66%, the 30-year fixed rate is meaningfully higher than it was in late February, when rates briefly touched the mid-5% range. Use Better’s mortgage calculator to estimate how today’s rate affects your monthly payment.

For buyers with a 30-day to 60-day closing timeline, the practical question is whether to lock now or wait to see what Wednesday’s CPI report brings. What determines mortgage rates is complex, but most borrowers benefit more from securing a rate they’re comfortable with than from trying to time the market.

Some lenders offer float-down options that allow you to lock a rate and then move to a lower rate should it drop materially before closing. Understand the terms and any associated fees before factoring this into your decision.

...in as little as 3 minutes — no credit impact

What refinance borrowers should know

The 30-year fixed refinance rate is sitting at 6.72%, and the 15-year refinance rate is at 6.10%. Check today’s refinance rates for real-time figures.

Refinance activity is still elevated compared to last year. Recent industry data shows refi applications up roughly 20% year-over-year, even with rates in the mid-6% range. That’s because a significant share of homeowners locked rates of 7% or higher in 2024 and early 2025 and now have meaningful room to reduce their payment or shorten their term.

Whether a refinance makes financial sense depends primarily on your break-even timeline: How long it takes for the monthly savings to offset the closing costs. Use Better’s refinance calculator to run that math on your specific situation.

How to get the best rate available today

No one can predict exactly where rates go from here. What you can often control is how competitive your own rate quote is when you apply.

Credit score

Your credit score is one of the most significant factors in the rate you’re offered. Borrowers with scores above 740–760 typically qualify for the most favorable pricing. See how credit affects your mortgage options in our guide to what determines mortgage rates.

Shop multiple lenders

Rate quotes vary more than most homebuyers expect. Industry research consistently shows that getting quotes from three to five lenders can result in meaningfully lower rates than going with the first offer. Better’s fully online process lets you get a real rate in minutes without impacting your credit score. Learn more about how to shop around for mortgage rates.

Consider your loan type

A fixed vs adjustable rate mortgage comparison is worth reviewing if you’re considering the 5/1 ARM — particularly since ARM rates today are running close to (not meaningfully below) the 30-year fixed.

Know your negotiating room

Many borrowers don’t realize mortgage rates are negotiable. You can ask lenders to match or beat a competing quote, especially when you’ve done the comparison work upfront.

Ready to see what rate you qualify for? Get pre-approved and lock in your rate when you’re ready.

FAQ

What are mortgage rates today, June 9, 2026?

Based on current market averages, the 30-year fixed mortgage rate is 6.66%, the 15-year fixed is 6.13%, and the 5/1 ARM is approximately 6.26%. The 30-year fixed refinance rate is around 6.72% and the 15-year fixed refinance rate is approximately 6.10%. These are national averages and your individual rate will vary based on your credit score, down payment, loan amount, and lender.

Why are mortgage rates going up right now?

Rates have risen primarily because May’s jobs report came in significantly stronger than expected, which pushed bond yields higher. When the economy shows strong momentum, inflation risk rises in the eyes of investors, and that typically flows through to higher mortgage rates. The ongoing Iran conflict adds a layer of volatility that can push rates in either direction.

Should I lock my mortgage rate today or wait for Wednesday’s CPI report?

If you’re within 30 to 45 days of closing, locking today protects you from further upside. If Wednesday’s CPI report shows inflation cooling, rates could ease modestly. But if it comes in hot, today’s rate may look attractive in hindsight. Many buyers find it easier to make a confident decision once they’ve locked rather than watching daily movement. Talk to your lender about rate lock options.

I have a 30-year mortgage from 2024 at 7.2%. Does it make sense to refinance now?

It may. With the 30-year refinance rate at approximately 6.72%, a borrower with a 7.2% rate has about 50 basis points of potential savings. Whether that pencils out depends on your loan balance and closing costs. Use Better’s refinance calculator to estimate your break-even point. Typically, if you can recoup closing costs within two to three years and you plan to stay in the home, refinancing is worth exploring seriously.

How does a strong jobs report affect mortgage rates?

Mortgage rates track the 10-year Treasury yield closely. When jobs data comes in stronger than expected, it signals that the economy is resilient and inflation may remain elevated which makes bonds less attractive at current yields. To attract buyers, bond yields have to rise, and mortgage rates follow.

What’s the difference between the 30-year fixed and the 5/1 ARM today?

The 30-year fixed rate is 6.66% and the 5/1 ARM is approximately 6.26%, a spread of about 40 basis points. With today’s compressed spread, the ARM is best suited for buyers confident they’ll sell or refinance within five years. Learn more about how to compare a fixed vs adjustable rate mortgage.

Why are refinance rates higher than purchase rates?

Refinance loans carry slightly higher risk in the eyes of lenders. Refinance rates are typically 0.05% to 0.15% higher than purchase rates on comparable loan products. Today’s 30-year refinance rate of approximately 6.72% compared to the purchase rate of 6.66% reflects that standard relationship.

Bottom line

Mortgage rates are elevated on June 9, 2026, driven by a stronger labor market and bond market volatility from the ongoing geopolitical conflict. The 30-year fixed at 6.66% is near its highest level in nine months, and Wednesday’s CPI report will be the next meaningful test for whether rates hold or move further.

If you’re an active buyer, the decision to lock now versus waiting a few more days is a risk-tolerance question, not a market-timing guarantee. If you’re a homeowner with a rate above 7%, the refinance math is worth running today.

Better’s fully online platform lets you check your rate in minutes with no impact to your credit score. Get pre-approved and see exactly where you stand.

...in as little as 3 minutes — no credit impact

Rates shown are daily average interest rates, not APRs, based on Better Mortgage data and are for informational purposes only. Rates are not guaranteed, may include borrower-paid or lender credits, and actual rates and terms vary by borrower and transaction. Comparison to industry average rates may not reflect individual borrower scenarios and is not a guarantee of lower rates or savings.