The Fed’s late October rate cut should lower borrowing costs and make houses more affordable.

But will rates fall low enough to get more buyers off the fence and back into the market?

Or are we settling into a long period of lower rates, encouraging buyers to wait for rates to drop even more?

Here’s what we know:

The late October rate cut: What happened?

The Fed’s much anticipated October decision shaved another 0.25 percent off the Central Bank’s benchmark rate. The decision was not a surprise. Most economists predicted a 0.25 percent cut identical to the Fed’s 0.25 percent cut in September.

The Fed doesn’t set mortgage rates, but its decisions affect the overall economy, including rates buyers and refinancing homeowners pay for new home loans. When the Fed cuts its rates, the cost of consumer borrowing, including for home buying, often goes down, too.

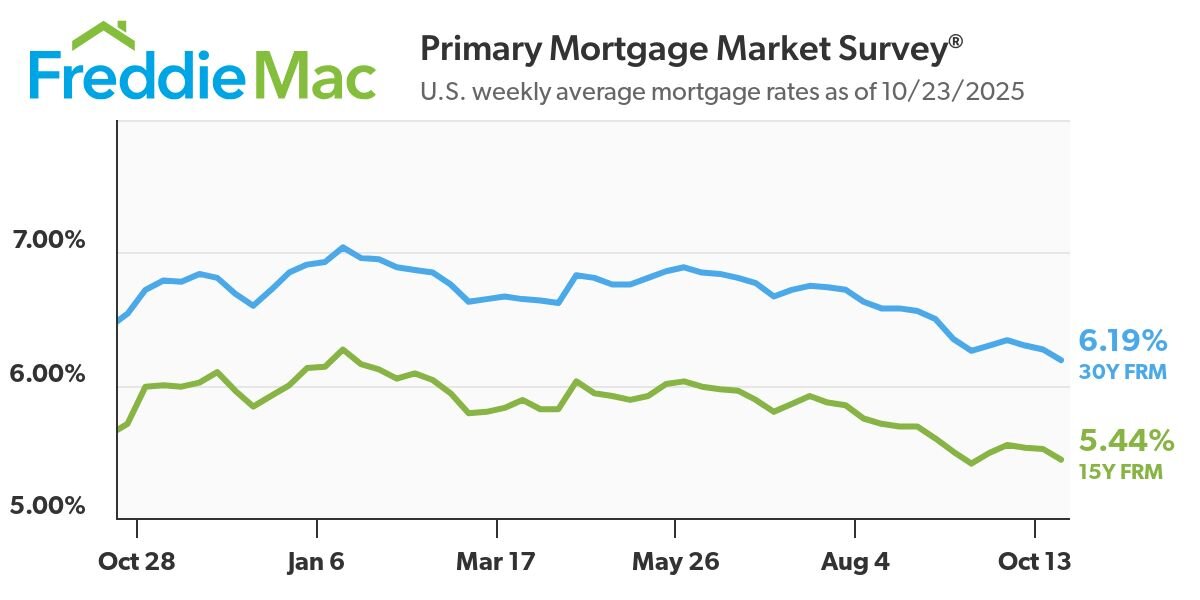

For example, 15- and 30-year fixed mortgage rates have already been trending downward in anticipation of the Fed’s cut:

Falling mortgage rates are great news for home shoppers and for existing homeowners who want to refinance to a lower rate. In fact, we’re already seeing another uptick in applications for refinances.

But will these lower rates get renters who are thinking about buying their own home off the fence? Or could lower rates backfire and make houses cost more?

Should I renew my lease or buy a home now?

This is the big question, and there’s no one-size-fits-all answer. Let’s break it down.

If your lease is ending soon and you’re wondering whether to keep renting or finally take the plunge into homeownership, here are a few points to consider:

The case for waiting: Borrowing costs have been gradually declining all year

Even small drops in average mortgage rates can create a noticeable difference in a new home’s monthly payment. For example, on a $400,000 loan, a rate that’s just 0.25 percent lower can save $70 to $100 per month. Over the course of a 30-year loan, that’s up to $36,000 in savings.

That money could go toward savings, home improvements, or future investments. Or it could help a borrower afford a more expensive home.

If rates stay on this downward trend, waiting to buy a home later, after the next Federal Reserve meeting, could save even more money.

The case for buying now: Housing inventory is still tight, and lower rates could make it tighter

While higher rates over the past two years have cooled housing demand in many markets, inventory is still tight. A fresh wave of new buyers, inspired by today’s lower rates, could ratchet up the competition for listings, and more competition usually means higher sales prices.

For some buyers, higher sales prices can cancel out gains from lower mortgage rates.

So, renters who have their eye on an affordable local listing may want to act now to avoid a new buying rush.

The reality: Your personal timeline matters most

For most home shoppers, buying a home now means locking in today’s mortgage rates and today’s home prices for the next 30 years. This shields buyers from ongoing market fluctuations.

On the other hand, for most renters, signing a new lease locks in a rent payment for only a year.

So, buying a home now, while rates are dropping and before house prices go up more, can be a smart move for renters who want to become homeowners.

But a lot depends on how long you’ll keep the home. For the upfront costs of getting into a home to pay off, the new homeowner usually needs to keep the home for a few years. Someone who plans to move within a year or two should probably keep renting.

What the rate cut means for the economy

Cutting interest rates is the Fed’s way of trying to boost economic activity. It’s all part of a broader economic cycle:

- When the economy gets too hot, as shown by employment data and inflation, the Fed raises rates to let off some steam.

- When the economy starts to lag, the Fed cuts rates to generate more economic momentum.

In normal economic times, a series of rate cuts, like the ones we’re now seeing, shows the economy is starting to slow.

But economic conditions have been far from normal during this decade. Average rates so far in the 2020s have set historic lows below 3 percent (in 2022) and have also soared above 7 percent (in 2024) for the first time since 2001.

Will rates keep going down?

Why has our economy been so volatile over the past few years, and when will it calm down?

A number of factors make this question hard to answer:

– Tariffs and the ever-present threat of more tariffs adds a layer of uncertainty about future prices and supply chain stability.

– Ongoing geopolitical crises in Russia and Ukraine as well as the Middle East could, at any moment, affect energy supplies and prices which reverberates throughout the economy. Also, the threat of instability in Venezuela, another player in the energy market, adds even more concern for long-term investors.

– The advancement of AI is affecting the job market. Employment levels factor into the Fed’s decisions about rates.

– The ongoing government shutdown has made jobs and inflation data more scarce, limiting the Fed’s ability to analyze these important economic indicators.

On top of all this, the Fed is thinning its Covid-era bond surplus. By selling fewer bonds, the Fed creates more demand for bonds which raises their prices and lowers their yield.

And, the Fed will appoint a new chair in May. The new appointment will likely align the Fed’s actions with the Trump Administration’s desire to push down rates.

What lower rates mean for individual borrowers

The Fed’s actions help shape average mortgage rates, and average rates show overall market trends.

But the borrower’s personal finances, the size of the loan, the lender’s costs, and other unique factors affect borrowers’ actual rates.

To see how all these variables translate into your new monthly payment, get a mortgage preapproval. Better’s preapproval process can show results in as little as three minutes with no credit impact.

Find out in as little as 3 minutes – no credit impact