A Home Equity Line of Credit, popularly known as a HELOC, is a powerful financial tool that can help homeowners unlock the value of their homes and access their home’s value when they need it the most. Whether you're considering your first HELOC or you're a seasoned homeowner looking for a refresher, this comprehensive guide will walk you through everything you need to know.

How do they work?

A HELOC loan, or Home Equity Line of Credit, is a type of loan that allows homeowners to borrow against the equity in their home. It works like a revolving line of credit, where borrowers can withdraw funds as needed and only pay interest on the amount borrowed.

Advantages of a HELOC Loan

There are several advantages to choosing a HELOC loan. They include:

Access to funds

Unlike traditional loans where you receive a lump sum upfront, HELOC's give you ongoing access to funds throughout the draw period. So, you can borrow only what you need when you need it. This gives you the freedom to use the funds for various purposes as they arise, without having to take out a new loan each time. This is why HELOC's are a great option to cover unexpected expenses such as medical bills or providing financial support during times of need.

Lower interest rates

HELOCs typically have lower interest rates than credit cards and personal loans because they are secured by your home.

Flexibility

Homeowners have the flexibility to use the funds for a variety of purposes, such as home renovations, debt consolidation, or even funding education expenses. This flexibility allows borrowers to tailor their loan to meet their specific financial needs.

Interest-only payments

During the draw period, which is usually several years long, you can borrow against your home equity and make interest-only payments. This means that you're only required to pay the interest on the amount borrowed, allowing you to manage your cash flow more effectively. It's important to note that during this period, you have the flexibility to pay down the principal if you choose to do so.

Once the draw period ends, the HELOC loan enters the repayment period. This is when you can no longer borrow against your home equity and must start repaying both the principal and interest on the amount borrowed. The repayment period typically lasts for several years and requires regular monthly payments.

Cash flow management

The interest-only payments during the draw period can significantly assist with managing your cash flow. This is especially beneficial if you have fluctuating income or unexpected expenses that arise. With the ability to pay down the principal during the draw period, you have the opportunity to strategically reduce your debt and potentially save on interest payments in the long run.

Potential tax benefits

Another factor to consider when contemplating a HELOC loan is the potential tax benefits. In some cases, the interest paid on a HELOC loan may be tax-deductible. However, it is essential to consult with a qualified tax professional or financial advisor to determine if you are eligible for these deductions based on your individual circumstances.

Risks of a HELOC Loan

When considering a HELOC loan, it's crucial to understand the potential risks involved. As with any type of loan, there is always the risk of defaulting on payments and potentially losing your home in foreclosure. Therefore, it's essential to assess your financial situation and ensure that you have a stable source of income and the ability to make timely payments before taking on a HELOC loan.

One important consideration when it comes to HELOC loans is the potential impact of changes in the real estate market on your home's value. Since a HELOC loan is secured by your home, if the real estate market takes a dip, it could affect your ability to borrow against your equity or even result in a higher interest rate.

Therefore, it's crucial to carefully assess the real estate market conditions and trends. Additionally, it is wise to have a plan in place for how you will manage the repayment period once it begins.

Before applying for a HELOC loan, it's important to thoroughly research and compare different lenders to ensure you get the best terms and interest rates. Look for reputable financial institutions, like Better, with a track record of providing excellent customer service and transparent lending practices.

In conclusion, a HELOC loan can be a valuable financial tool for those in need of flexible borrowing options. With careful consideration of your financial situation, budgeting, and repayment plan, a HELOC loan can help you manage cash flow, strategically reduce debt, and potentially take advantage of tax benefits.

How Much Can You Borrow with a HELOC Loan?

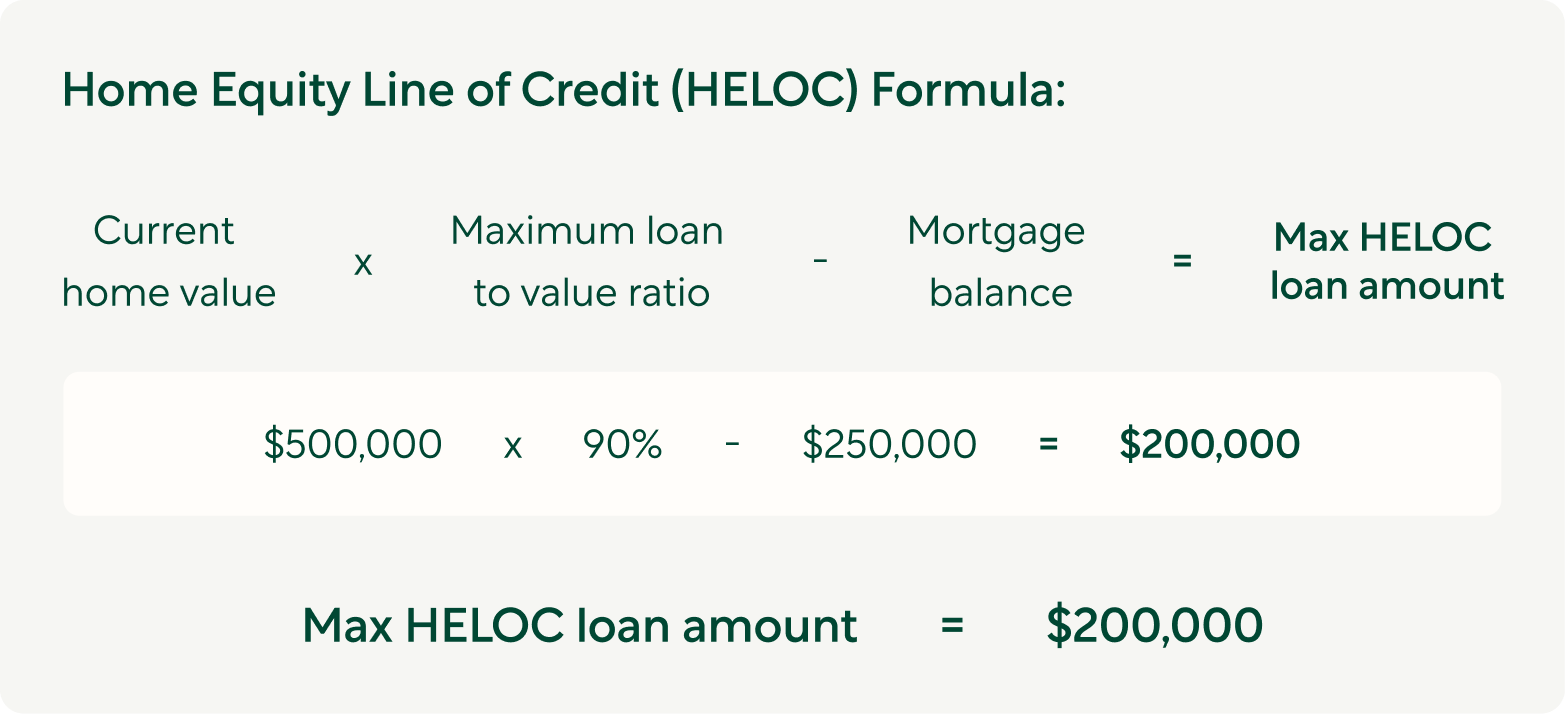

The borrowing limit for a HELOC, also known as a home equity line of credit, is typically set by the lender and depends on several factors such as the value of your home, your credit score, and your debt-to-income ratio.

Lenders like Better allow you to borrow up to 90% of your home's appraised value, minus the amount you owe on your mortgage. For example, if your home is worth $500,000 and you still owe $250,000 on your mortgage, then you may qualify for a HELOC up to $200,000.

Use our Home Equity Line of Credit (HELOC) calculator to see how much you could borrow.

HELOC rates: what you need to know

Understanding HELOC interest rates is crucial to managing your loan effectively. These rates are often variable and influenced by several factors, such as your credit score and the loan-to-value ratio. It's essential to compare average HELOC rates from different lenders to ensure you're getting the best deal and a competitive rate.

Look at today's HELOC rates here.

HELOC loan vs home equity loan: which is better for you?

Choosing between a HELOC and a home equity loan depends on your specific needs. While a HELOC offers flexibility and typically has a variable interest rate, a home equity loan provides a lump sum of money with a fixed interest rate. Your decision should be guided by your financial goals, borrowing needs, and risk tolerance.

If you’re unsure what option is best for you, compare different loan types, such as a cash-out refinance or home equity loan types. Learn more here.

How to qualify for a HELOC loan

Like a mortgage, qualifying for a HELOC requires meeting certain criteria. Lenders typically look at your credit score, the amount of equity you have in your home, and your debt-to-income ratio, among other criteria.

You can check if you’re approved for a Better HELOC in as little as 3 minutes with no impact to your credit score with our simple, online experience here.

Frequently Asked Questions about HELOC Loans

HELOCs often come with a lot of questions.

Can you pay off a HELOC early?

Unlike some loans that may have prepayment penalties, HELOCs generally allow borrowers to repay the outstanding balance at any time without incurring additional fees. Early repayment can be beneficial for borrowers as it helps save on interest costs over the life of the loan.

However, it's advisable to check the terms and conditions of your specific HELOC agreement, as some lenders may have certain stipulations or fees associated with early repayment.

Always consult with your lender to fully understand the terms of your HELOC and to ensure a smooth and hassle-free early repayment process.

What happens if you can't pay back a HELOC?

If you find yourself unable to pay back a Home Equity Line of Credit (HELOC), there are potential consequences that may vary depending on the terms of your agreement and your lender's policies. Failure to make payments could result in late fees, increased interest rates, and damage to your credit score. In more severe cases, the lender may initiate foreclosure proceedings if the HELOC is secured by your home.

It is crucial to communicate with your lender as soon as you anticipate financial difficulties. Many lenders offer assistance programs or may be willing to work with you to find a solution, such as modifying the repayment terms. Seeking professional financial advice and exploring available options early on is essential to mitigate the impact of financial challenges and avoid more serious consequences associated with non-payment.

Is the interest on a HELOC loan tax deductible?

Historically, interest on a HELOC used for home improvements has been tax-deductible, subject to certain limitations imposed by tax laws. However, changes in tax regulations can impact these deductions, so it's crucial to consult with a tax professional or financial advisor to get the most accurate and up-to-date information.

Also, it's important to keep detailed records of how the HELOC funds are used, as this information is crucial for determining the tax deductibility of the interest.

Alternatives to a HELOC Loan

While a HELOC can be a great tool, it's not the only option for leveraging your home's equity. Other options include home equity loans and cash-out refinances. It's important to compare these options to ensure you're making the best decision for your financial situation.

What makes Better's HELOC...better?

All digital. Unlike other lenders, you can finish your application, appraisal, and notary closing from the convenience of home.

- Get cash in as little as 7 days.

- Available on investment, primary, and secondary properties.

- Choose between a 3-year, 5-year and 10-year draw period, and loan terms of 15-, 20-, 25-, or 30-years, letting you find the loan for your cash needs

You can check if you’re approved for a Better HELOC in as little as 3 minutes with no impact to your credit score with our simple, online experience here.

Better Mortgage's HELOC product is available in all states other than TX and UT.

Please note that you are required to draw at least $50,000 or 75% of your credit limit, whichever is greater, at the time of funding (ex. if your credit limit is $200,000, you must draw $150,000 or more at funding). If you would like to draw less at funding, you may lower your credit limit. HELOC Important Terms