Michael McGinniss, a non-commissioned Loan Consultant at Better Mortgage, highlights what homebuyers should look for when comparing FHA and HomeReady.

Trying to figure out how to buy a home while you're still paying off student loans? Still recovering from a blip on your credit report and wondering if you can qualify for a mortgage? Looking to buy a home for the first time, but sky-high rent has drained your savings?

Many of us face these types of financial obstacles in our journeys to homeownership. Maybe you’ve looked into affordable home financing options to help you overcome these hurdles. If you are one of the many prospective homebuyers who need more flexible options, we have two suggestions that could help you get closer to owning a home: FHA loans and HomeReady.

HomeReady and FHA loans are comparable in that they are both designed to make homeownership more accessible to those who face financial challenges like low down payment funds and limited income. While both types of home loans may appeal to homebuyers looking for affordable financing, there are some clear differences between the two. Let’s break down HomeReady and FHA loans to help you determine which one is right for you.

Credit Score

Our borrowers often have questions about how their credit score may affect their eligibility, especially if their score is on the lower end. In general, lenders use your credit score (and the borrowing history that shaped it) in order to determine your ability to pay back your loans. Having a higher credit score means that you may receive more favorable rates that can save you a considerable amount of money over the life of your loan. Credit score guidelines also apply to affordable lending products like HomeReady and FHA loans.

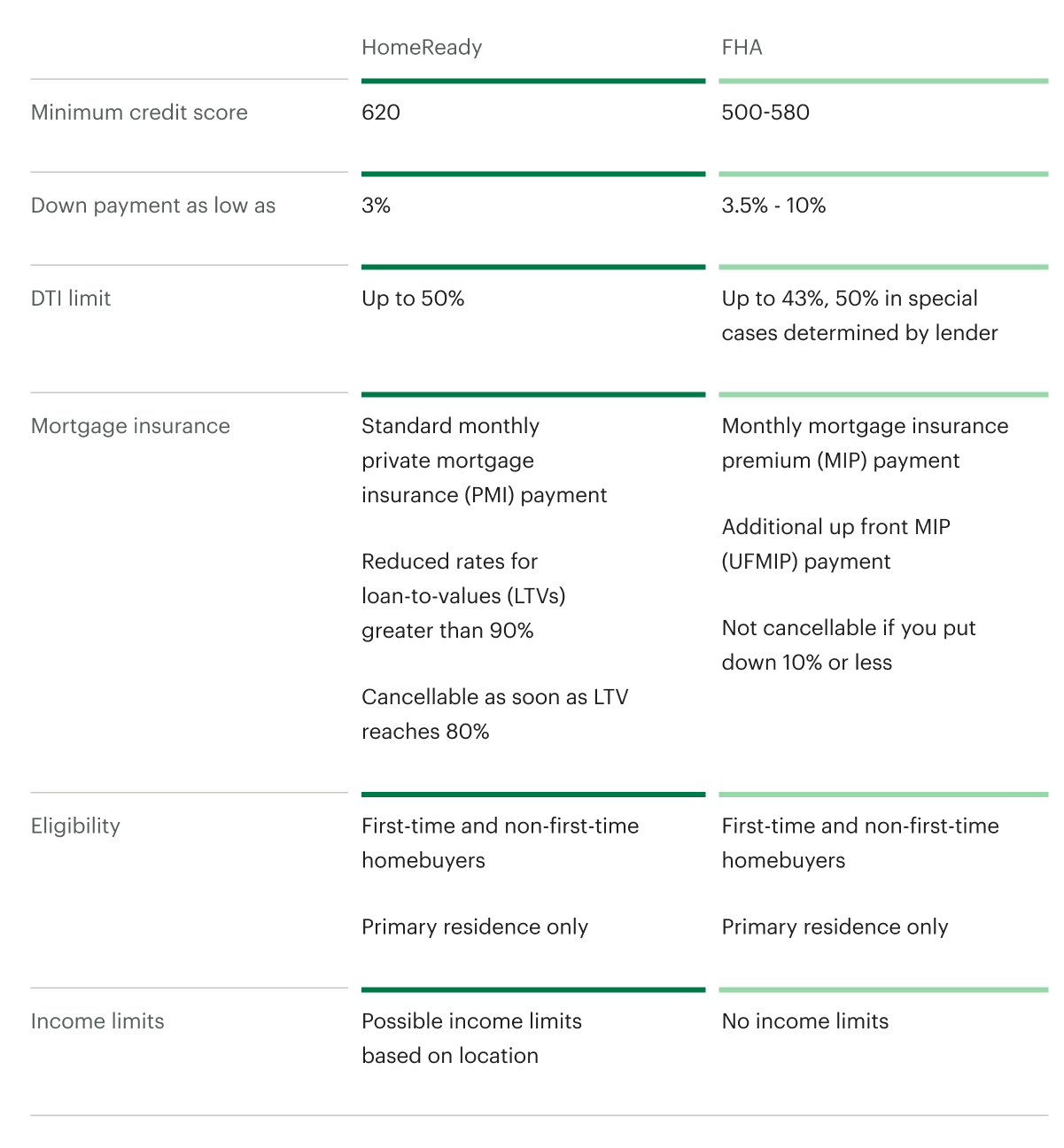

Depending on the details of your loan and financial history, you can qualify for HomeReady with a credit score as low as 620. In order to qualify for the most competitive rates possible, you may need a credit score above 680.

With an FHA loan, your credit score can be as low as 580 if your down payment is at least 3.5% or as low as 500 if your down payment is at least 10%.

Down payment

Saving up for a down payment is challenging for homebuyers across the credit spectrum, but it can seem even more daunting for people with tighter budgets. In fact, having enough money for a down payment is an obstacle for more than half of millennial renters. While you may have heard that 20% is the “magic number” for a down payment, HomeReady and FHA loans offer much lower down payment options.

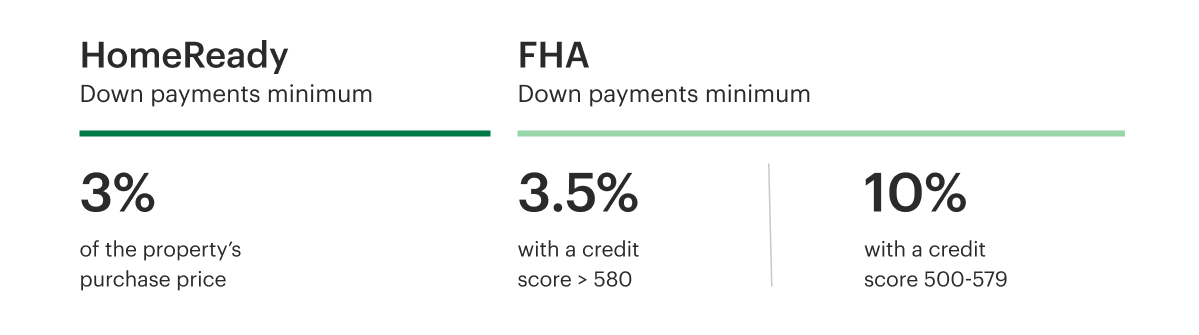

Depending on the specifics of your financial history, HomeReady can allow for down payments as low as 3% of the property’s purchase price. As we previously mentioned, FHA loans accept down payments as low as 10% if your credit score is between 500 and 579 or as low as 3.5% if your credit score is greater than 580.

Debt-to-income (DTI) ratio

Your debt-to-income (DTI) ratio is an important figure for your lender to evaluate when you apply for a loan. You can calculate it by dividing your monthly debt payments by your gross monthly income. DTI shows your lender how much money you have coming in against how much is going out. In general, the lower your DTI, the more financing options will be available to you.

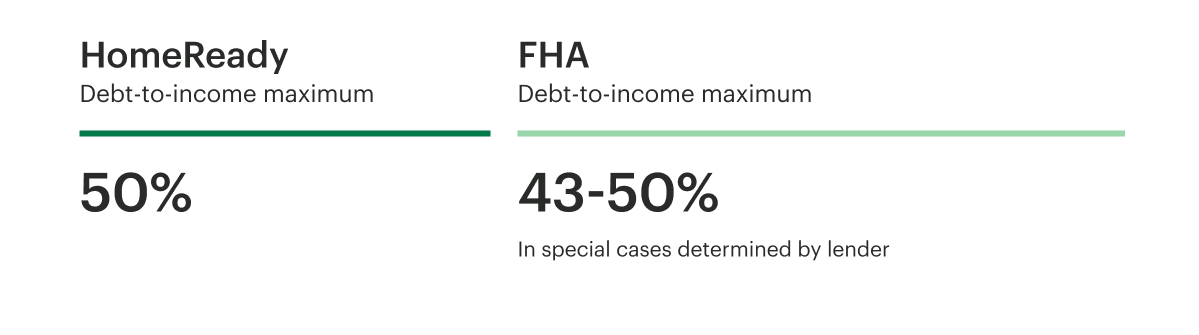

The maximum allowable DTI with HomeReady can be as high as 50%. If your new home has an accessory unit, HomeReady may also consider your future rental income, which may boost your qualifying income and improve your DTI.

The FHA limit for DTI is currently 43%, but your DTI can go up to 50% if your lender provides justification for the added risk of the loan.

Mortgage Insurance

Across the mortgage industry, borrowers are required to pay mortgage insurance for any loan in which their down payment is less than 20%. Mortgage insurance protects the lender in case the borrower defaults and is unable to make their loan payments. The exact amount you’ll pay is based on the type of loan you choose, as well as factors like your loan-to-value (LTV) ratio, which is the number you get when you divide your loan amount by the value of your property. For example, if you put 3% down, your LTV would start at 97%.

Any form of mortgage insurance will increase the amount you’ll pay over the life of your loan, but the big difference between FHA and HomeReady is how mortgage insurance is calculated—and whether or not you can cancel it later on. Let’s take a closer look:

Mortgage insurance with FHA consists of two parts: an annual mortgage insurance premium (MIP) and an upfront mortgage insurance premium (UFMIP). The MIP is a monthly fee built into your mortgage payment. If your LTV is greater than 90% when your loan is originated, you’ll be required to pay mortgage insurance for the life of the loan—there is no option to cancel.

Oftentimes, this means you’ll be paying mortgage insurance even after any real financial risk to the lender has disappeared, which can cost you over the life of your loan. If your LTV is 90% or less (and even if you put more than 20% down making your LTV 80% or less), you’ll be required to pay mortgage insurance for 11 years or the life of the loan, whichever happens first.

In addition to the MIP, you also pay a UFMIP. This is an additional one-time premium payment equal to 1.75% of your loan amount, regardless of your LTV. You’ll pay the UFMIP in addition to your down payment, and you can choose to pay the UFMIP upfront, as the name suggests, or finance it into your monthly mortgage payments.

Like most loans where borrowers put less than 20% down, HomeReady’s private mortgage insurance (PMI) consists of monthly payments that are included in your mortgage bill—there is no additional upfront fee. A benefit of HomeReady is that even if your LTV is above 90% (up to 97%!), the standard PMI coverage requirements can be reduced, and when your LTV reaches 80%, you can request to have your mortgage insurance canceled. It will automatically be canceled when your LTV drops below 78%.

Together, these HomeReady benefits often result in lower mortgage insurance costs compared to FHA. But there are pros and cons to both based on your financial situation.

Additional Requirements

Both FHA and HomeReady programs are available to borrowers regardless of whether or not they are first-time homebuyers. However, they are only available for a primary residence, so you can’t use these loans to fund a second home. If you’re looking to buy a condo, FHA has stricter requirements. Many condo developments are ineligible for FHA but may still qualify for HomeReady.

While there are no income limits to be eligible for an FHA loan, HomeReady may have income limits depending on the location of your property. In order to qualify for a HomeReady loan, you must either purchase a property in a neighborhood with no income limit or have an income below the median income of the neighborhood, as established by census data. Our team can help you determine if your income or your property location qualifies you for the program.

HomeReady also requires borrowers to take an online course that will teach them the principles of homeownership. The course, available in English and Spanish, is designed to help you gain essential knowledge to make you a well-informed homebuyer. Our customers have found the homebuying course valuable and have even recommended it to their friends and family. Better Mortgage pays the $75 course fee for you and sets up your account, so it’s easy to get started.

Start with a pre-approval, and Better Mortgage will help you with the rest

It’s our goal to make homeownership accessible to as many people as possible. If you’re interested in exploring your home loan options start with a pre-approval. Our tech and our team will help you find the right homeownership solution for you and your family.*

*Better Mortgage currently offers FHA loans for homebuyers in all states Better Mortgage is available in.