What You’ll Learn

The difference between APR and interest rate

How to calculate APR and interest rate

How to get an understanding of your home loan’s true cost

Both interest rate and APR are terms used to describe the cost of borrowing money for your mortgage. While these numbers are related, they’re not the same. Here’s what you need to know about each so you can make an informed decision for your new home or refinance.

Understanding interest rates on a mortgage

A home loan’s interest rate is expressed as a percentage of the principal loan amount that a mortgage lender charges you on an annual basis for borrowing your principal loan amount. This rate doesn't include fees or closing costs and is only based on the amount you borrow for your home loan.

There are two types of mortgages that affect how your interest rate is applied:

Interest rates change daily and are affected by a number of economic factors, including inflation, economic growth, the bond market, and housing conditions. That’s why it’s important to “lock in” a favorable interest rate so you can stay protected from market fluctuations.

The interest rate you’ll qualify for also depends on your financial situation, such as your credit score, down payment, loan amount, and debt-to-income ratio.

Understanding mortgage APR and how it differs from interest rates

A home loan’s annual percentage rate (APR) is also displayed as a percentage, but is higher than the accompanying interest rate. That’s because an APR not only takes your interest rate into account, but also factors in other costs, such as most closing costs and lender fees. The APR provides a more holistic view of your total mortgage cost on an annual basis.

That said: not all costs are represented in APR—such as your lender-required credit report, appraisal, inspection fees, and/or other third-party fees. You’ll want to find out what’s included so you have the most accurate understanding of the cost of the loan and can compare “apples to apples” between different lenders.

Comparing APRs vs interest rate among lenders

The Consumer Finance Protection Bureau (CFPB) requires mortgage lenders to give you a Loan Estimate document within 3 business days of receiving your financial information.

On page 3, you’ll find a section on “Comparisons,” where you’ll be able to see the APR and how much the loan will cost you in total over the first 5 years. It takes multiple factors into account, such as loan cost, interest, principal, and mortgage insurance.

If you’re comparing different lenders, this page can help you decide which lender and home loan are right for you. Once you see each lender's APR, you’ll know how much it will cost to move forward with their respective loan products, inclusive of fees and interest rates.

How closing costs and interest rate affect mortgage APR

While some lenders may advertise a no-closing-cost loan, it’s important to understand that those costs are still there, but instead of paying them upfront, they’re “absorbed” into the loan. A common way to do this is by adjusting the opposing levers on interest rates and APR: in exchange for a higher interest rate, you may be able to lower your upfront closing costs and your total APR.

On the other hand, paying more in closing costs will usually result in a lower loan interest rate and a higher total loan cost, or APR.

As a general rule of thumb, interest rates and APRs have an inverse relationship:

Deciding which is right for you comes down to preference. Are you most concerned with the monthly payment being as low as possible? Or do you prefer to save more money upfront?

Of course, if you’re purchasing a home and your seller is offering a generous amount in closing cost concessions, then you may be able to benefit from both a low rate and low out-of-pocket closing costs.

Consider how long you’ll have your mortgage when deciding between interest rate vs APR

When it comes to evaluating APR, another important factor is how long you plan to live in your home. The APR assumes you will stay in your mortgage for the full term (e.g., 30 years on a 30-year loan). If you plan on moving within a few years, or you’re thinking about refinancing after a certain time (most likely the case if you have an adjustable-rate mortgage, or ARM), then it may make sense to pay fewer upfront fees and get a higher APR. That way, the total cost will be less over the first few years. But, if this is your “forever home,” then it usually makes sense to choose a mortgage that has the lowest APR.

Consider how long it would be before you’d recoup any closing costs paid upfront; it may be worth it to pay a higher APR for a lower interest rate over the life of your loan. To decide between paying a higher interest rate or APR, divide the cost of the points by the monthly amount saved in interest.

For example:

*The example above is based on the following assumptions: $300,000 loan amount; 30-Year fixed rate purchase loan; borrower with a FICO score of 740; maximum loan-to-value ratio of 80%; subject property is in California; 12 payments per year. The loan scenarios displayed above are for illustrative purposes only.

Take this actual scenario using Better.com rates—both of which are for 30-year fixed conforming loans with no mortgage insurance.

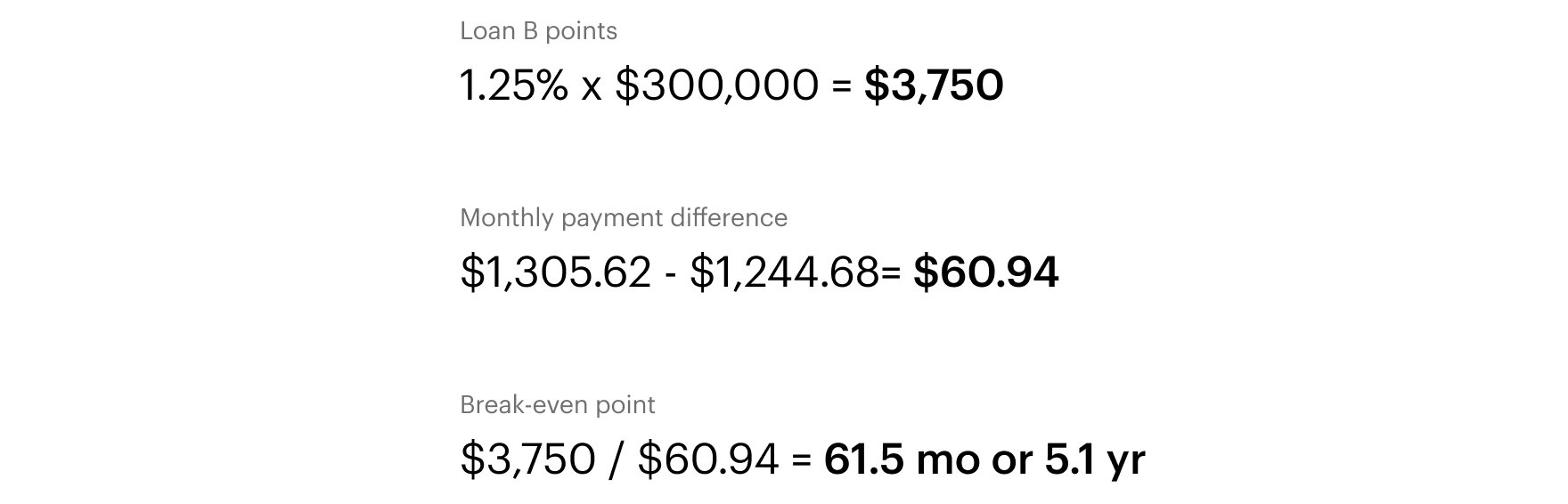

Loan A has an interest rate of 3.25% with no points or fees, meaning the APR is also 3.25%. Loan B has a lower interest rate of 2.875% but pays 1.25% in points upfront pushing its APR to 2.98%.

Let’s say you only want to stay in the home for 8 years, how can you determine which loan option would be more beneficial for you?

This is where we need to calculate the breakeven point, or where the short-term benefit of having no points and fees is superseded by the long-term benefit of the lower interest rate.

This is most easily calculated by dividing the upfront fees of Loan B by the difference in payment between the two scenarios.

So, if you plan to stay in your home for less than 61.5 months (or just over 5 years), then it makes sense to choose Loan A, the higher interest rate and no points. If you plan to live in your home longer without refinancing, then Loan B (with the lower interest rate but more upfront costs) makes more financial sense.

Don’t settle for a mortgage with lender fees

With most mortgage lenders, closing costs comprise lender fees and third-party fees. But at Better Mortgage, we never charge lender fees, so there are no loan officer commissions, lender origination fees, application fees, or underwriting fees.

The competitive interest rate that you get will be accompanied with an APR that isn’t inflated by unnecessary costs, which can equal thousands of dollars over the life of your loan.

Ready to get a Better Mortgage experience? Get your custom rates today.

This blog post is for informational purposes only, and is not intended to provide, and should not be relied upon for tax, legal or accounting advice.