Here’s a look at the latest developments in the homebuying market this week.

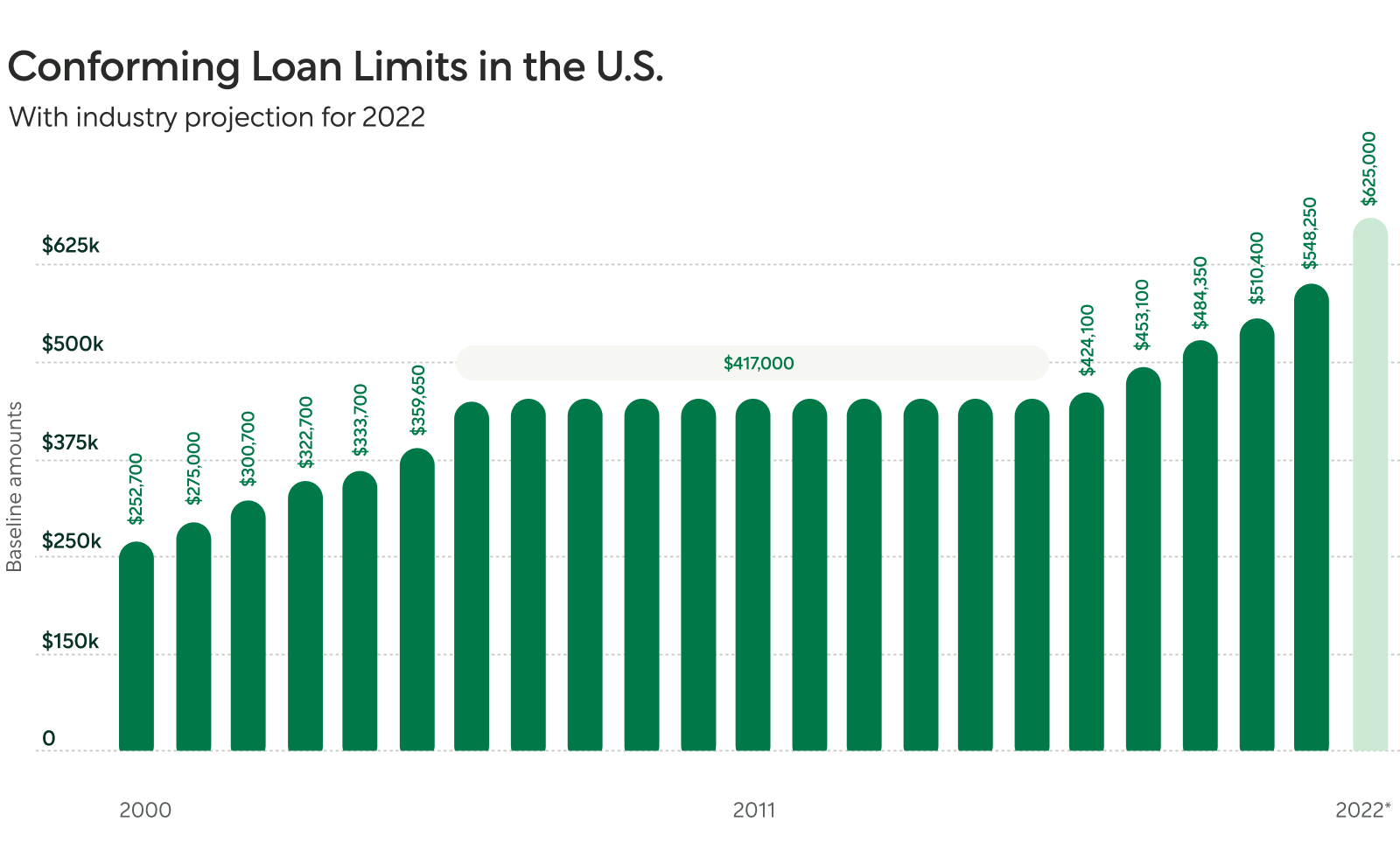

The ceiling on conforming loans is going up, and it can help you save on a new home

Source: Federal Housing Finance Agency via Inman

Fannie Mae and Freddie Mac are expected to raise the limit on conforming loans next month. This should make it easier for homeowners to borrow higher amounts when they refinance, without potentially spending more on the price of a jumbo loan.

Conforming loan limits are the maximum amount you can borrow for a conforming loan in each county. They’re decided by the Federal Housing Finance Agency (FHFA) in order to keep the market stable, and determined according to national average home prices. In August, the national median listing price was $380,000, and the U.S. Home Price Index rose by its highest gain in 45 years.

If you want to borrow more than today’s most common conforming loan limit of $548,250, you would likely need a jumbo loan. Those can come with tougher eligibility requirements, higher down payment minimums, and often, higher interest rates. The new conforming loan limit is expected to rise by at least $75,000, to $625,000—its highest increase since 1970. That means more opportunity for homeowners to save on a conforming loan and its options.

The change would officially take effect after January 1, 2022, but Better Mortgage plans to implement the new limit once it’s announced. Until then, learn more about the differences between a conforming loan and a jumbo loan.

Bidding wars are slowing down but inventory remains low

Home prices continue to rise and inventory remains historically low, but there are some bright spots on the market that show competition may be slowing down.

Bidding wars have dropped in frequency, down to a rate of 59% of homes rather than 74% this past spring. On top of that, a smaller share of homes are selling over asking price, and the number of homes selling within two weeks has dropped nearly 10% from its peak in March. Plus, more listings are popping up from owners coming out of forbearance relief plans.

While these are positive signs, demand continues to outpace supply by as much as five million homes. Standing out as a buyer is key to landing the home you want, and making an all-cash offer can help. By working with Better Real Estate and Better Mortgage, you may qualify for a Better Cash Offer. That means making a bid using Better’s cash at no extra cost. Find out more about the Better Cash Offer program and whether it’s the right move for you.

Considering a home loan?

Get your custom rates in minutes with Better Mortgage. Their team is here to keep you informed and on track from pre-approval to closing.