If you’re shopping for a house or considering a refinance, you’ve probably spent time looking at rate tables or getting quotes from lenders. This is a great way to get a general sense of your options, but it’s not entirely accurate. There’s only one accurate way to compare lenders.

A Loan Estimate is a standardized form created by the Consumer Financial Protection Bureau in 2015 to protect homebuyers like you. Loan Estimates share a clear breakdown of the nitty-gritty details and costs associated with your loan. Getting a Loan Estimate doesn’t mean your loan has been approved, but they do make it easier for you to understand the terms of a loan and accurately compare different loan offers. They’re one of the best resources to help you make an informed decision about how to proceed.

What’s included on a loan estimate?

First, to get a Loan Estimate, you’ll need six pieces of information: your name, income, social security number, desired loan amount, desired property address, and its listing price. After you provide these six pieces of information, a lender is legally required to share a Loan Estimate within 3 days. Some aspects of the Loan Estimate, such as points and credits, can fluctuate until the loan is locked.

Other numbers, such as taxes, will change throughout the process as documentation is received and loan estimates are updated. When the loan is locked, the terms of that documentation are binding and valid for a period of 10 days. At Better Mortgage, we provide a Loan Estimate as soon as you create an account, so you can instantly review and decide next steps. Once you receive your Loan Estimate, you should review the terms and evaluate the costs outlined in each section.

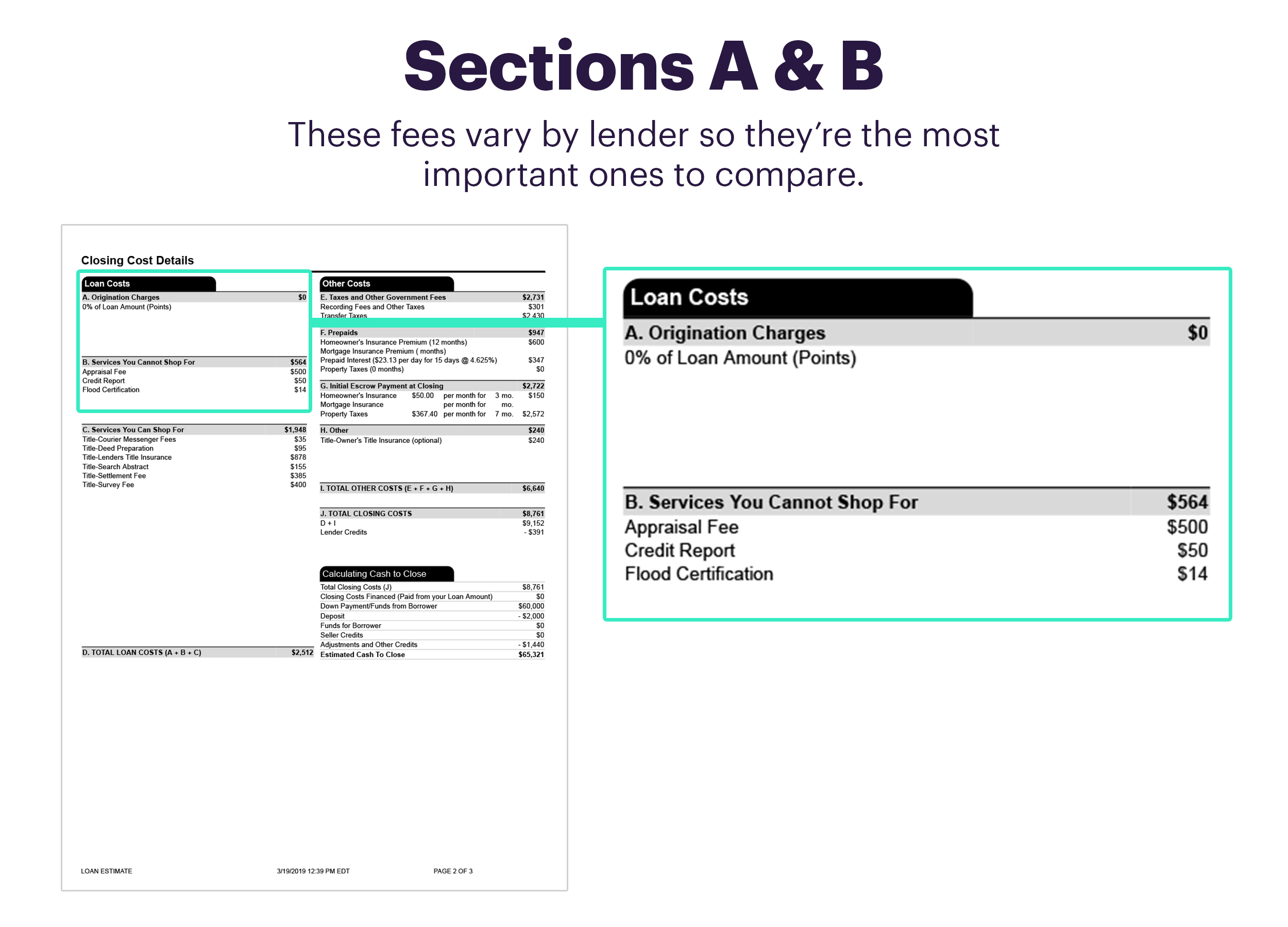

Section A: Origination charges

This is where you’ll see points if you’ve opted to purchase a lower rate. You may also see underwriting, processing, or origination fees.

Section B: Services you cannot shop for

Services you cannot shop for are set by the lender and must be paid by the borrower. The big ticket item here is your appraisal, which makes sure your home is worth what the seller claims it’s worth. The appraisal must be conducted by a licensed third party, and the one-time fee for that process will be reflected here. Other lenders may also charge condo fees or subordination fees.

Condo fees cover the cost of a project questionnaire, which is an additional piece of documentation that lenders will need to review before they can approve any loan for condo properties.

Subordination refers to the practice of prioritizing between multiple loans, subordinating one loan in favor of a new one that will take precedence in payment priority. Lenders may charge a fee for setting this designation in your loan refinance. Better Mortgage chooses to absorb these kinds of costs rather than passing them along to our borrowers, so you won’t see either of them listed in our Loan Estimates.

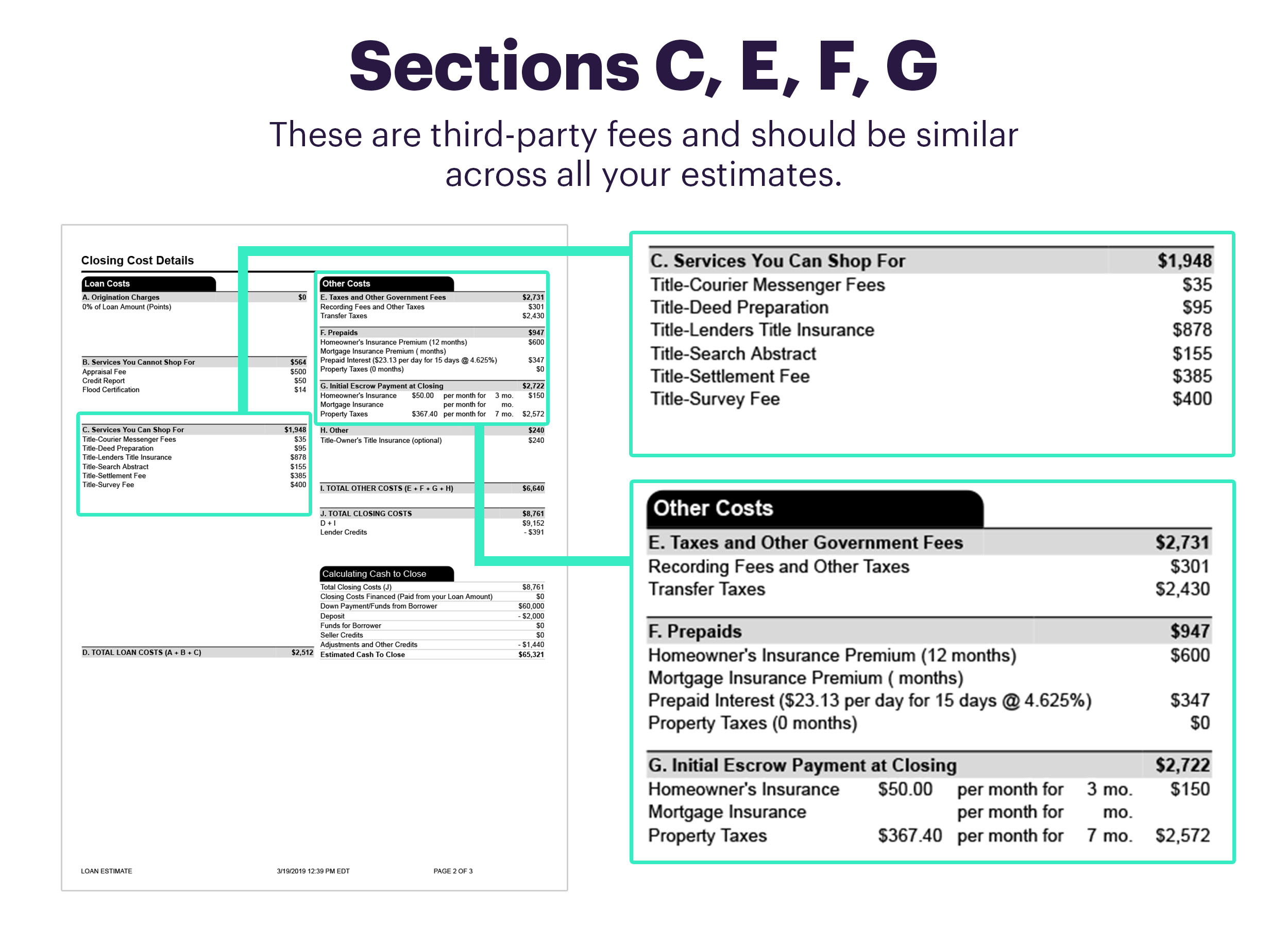

Section C: Services you can shop for

This section in your Loan Estimate outlines the costs of required third-party actions ranging from inspections to property surveys to title services, all of which need to happen before closing.

Home inspections are meant to identify issues or damages to the home. They offer an opportunity to document any outstanding repairs or maintenance that may be required should you decide to purchase the home; they can also give you a chance to walk away from the seller if you decide the issues are too extensive.

Property surveys explicitly outline the boundaries of your lot and even evaluate topographical risk factors such as slope or ground incline.

Title services verify that the seller legally owns the property in question and can legitimately transfer the deed to you.

As the name on the section header suggests, you have an opportunity to “shop” more competitive rates for all these fees if you’re unsatisfied with the prices quoted here. Lenders are required to share a list of approved service providers for borrowers to choose from, but you can also select other vendors not found on this list. Ultimately, they are still subject to approval by the lender, but there is an opportunity to save money if you’re unsatisfied with the initial fees. (Just make sure to get confirmation from your lender before committing to any agreements with third parties.)

Sections E, F, G: Taxes, prepaids, and escrow payment

These sections of the Loan Estimate also contain third-party fees ranging from property taxes to homeowners insurance or mortgage insurance costs depending on the type of loan you have. These costs will be the same no matter which lender you go with because they’re determined by external entities. You may also see discrepancies in this section because these numbers are based on estimates. Double check with tax authorities or insurance companies if you’re concerned about the accuracy of the quotes.

How to compare Loan Estimates

Loan Estimates are essential tools that help borrowers compare available lending options. Understanding these key costs associated with your loan can empower borrowers to make an informed decision and ultimately save money. The first page of your estimate outlines the general terms of your loan. You should make sure the interest rate and loan amount listed match what you selected or discussed with the lender. Page 2 of your estimate is where things get a bit trickier. If you’re buying a home, some of the most important numbers to compare are in Sections A and B: origination charges and services you cannot shop for. If you’re refinancing a home, you should also compare title service fees in Section C. Some of these figures will vary by lender and impact your monthly payment and cash due at closing. At Better Mortgage, we’re committed to eliminating unnecessary fees wherever possible and not passing costs on to our customers. Ready to start the process and get your Loan Estimate today?