What you’ll learn

Benefits and drawbacks of a HELOC for a second home

How to use a HELOC to buy a second home

Other loan options to buy a second home

Dreaming of purchasing a second home for a family getaway or rental? There are several financing options available to help you. One of the most flexible is a home equity line of credit (HELOC), which allows you to tap into your equity. With Better, owner-occupied primary residences, second homes, and investment properties may be eligible for a HELOC.

With a home equity line of credit, you’re approved for a maximum borrowing limit, and during the typical five- to 10-year draw period, you can withdraw funds as needed, borrowing and repaying multiple times. Afterward, you’ll repay what you owe, including interest.

Using a HELOC to buy a second home can make a lot of sense for homeowners who have built significant equity in their primary residence. But that raises some important questions: How much can you borrow using a HELOC to buy another house? What are the benefits and drawbacks of applying HELOC funds to a second home purchase? What steps should you take to apply for a home equity line of credit? And what other financing options, like a home equity loan or cash-out refinance, should you consider? Read on for answers.

Benefits and drawbacks of using a HELOC for a second home

There are several pros and cons to taking out a second mortgage to buy a second home. Let’s explore both in detail.

Pros of using a HELOC for a second home

— You can apply HELOC funds toward virtually anything you want. That means using home equity from your primary residence for a down payment on a second home. You can even use the funds funds from a HELOC for debt consolidation.

— Depending on your home’s equity, you could be approved for a substantial credit line, potentially funding much, if not all, of the second home purchase.

— A HELOC is a flexible, reusable line of credit. During the draw period, which typically lasts five to 10 years, you’ll only pay interest on the amount you actually use, not on your total approved limit. For example, if you borrow $70,000, that’s the amount you’ll pay interest on, rather than the entire available credit.

— Think of a HELOC as a flexible safety net for unexpected costs related to your second home. Beyond the down payment or full purchase, you can draw funds at different times to cover things like renovation expenses.

— HELOCs usually offer lower interest rates compared to unsecured loans. Since your primary residence secures the HELOC, rates may be more favorable than those for personal loans or credit cards.

— You won’t need to refinance your primary mortgage. A HELOC allows you to access your home equity without touching your existing mortgage, which is a major benefit for homeowners who have locked in historically low interest rates on their primary residence.

— Interest paid on a HELOC may be tax-deductible if the second home is a rental property. For example, someone can use a $150,000 HELOC to buy a Florida vacation condo, deducting interest on rental income.

Cons of using a HELOC for a second home

— If you choose a variable-rate HELOC, your monthly payment could rise if interest rates increase. Since it’s hard to predict how rates will change, managing two properties could become financially challenging if rates go up.

— You may end up borrowing more than you initially planned, leading to higher interest payments than expected, especially if you’re approved for a large credit line.

— Remember, your primary residence secures the home equity line of credit, meaning if you don’t repay as agreed, your home could be at risk of foreclosure.

— You’ll need to manage two stages of repayment. During the draw period, you only pay interest on what you borrow. But once the repayment period begins (typically spanning 10 to 20 years), you’ll pay both principal and interest.

— Most HELOCs charge closing costs, which usually range from 2% to 5% of the total credit line.

— If you plan to use the second home as a rental property, qualifying for a HELOC may be more challenging. Many lenders impose stricter credit score requirements or place limits on the equity you can access for investment purposes.

How to use a HELOC to buy a second home

Curious about how to use a HELOC to buy a second home? Here’s a step-by-step guide.

Determine your loan-to-value (LTV) ratio

Your LTV ratio is the amount you owe on your primary mortgage compared to your home’s current value. This is a key metric that lenders use to assess risk. The lower your LTV, the more favorable the interest rate and borrowing terms you’ll likely receive. To calculate the LTV ratio, divide your mortgage balance by the market value of your home, then multiply by 100.

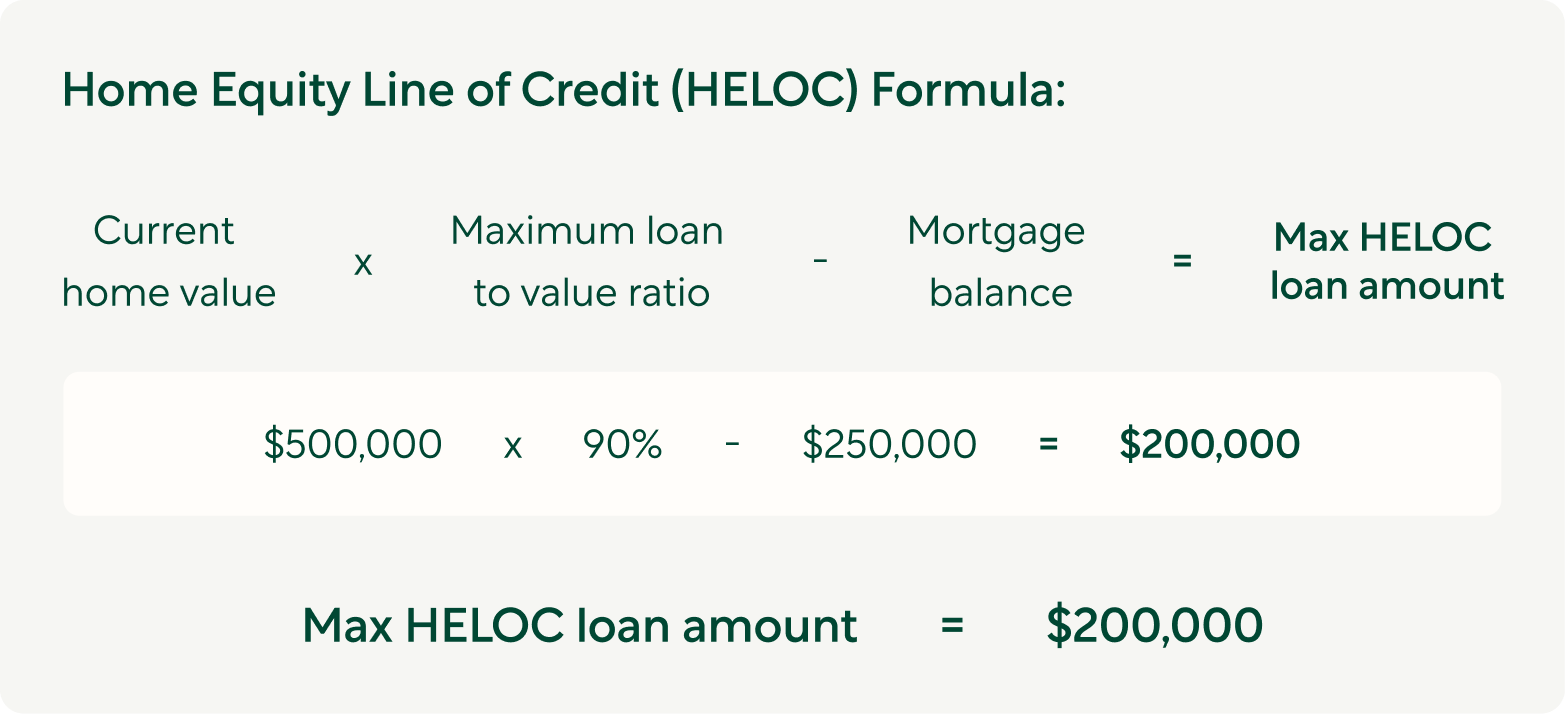

Check your equity

You’ll need to evaluate your home’s equity to determine how much you can borrow. To do this, subtract your existing mortgage balance from your property’s current market value. While many lenders will allow you to borrow up to 85% of your home’s value, Better allows up to borrow up to 90%, or $750,000.

Here's a guide:

Otherwise, to quickly see how much equity you can borrow from your home, use Better's HELOC calculator.

Set a budget

Create a detailed budget that factors in your second home purchase. Include the amount you plan to borrow through the HELOC, any down payment, and other financial commitments related to the new property.

Shop for a HELOC

When shopping for a HELOC, compare different lenders, including banks, credit unions, and online lenders. Look for the best rates, fees, and terms.

| Feature | Better HELOC | Other Lenders |

|---|---|---|

| Appraisal fees | Appraisal may be waived | Often required ($500-$700) |

| Cash access | Up to 90% of your property’s value, up to $750,000 | Typically 80-85% |

| Availability | Available for primary, secondary, and investment homes | Typically available only on primary residences |

| Closing speed | One Day HELOC: Decision in 24 hours, cash in 7 days | Typically 30-45 days |

| Transparency | No hidden fees | Often unclear fees |

| Interest rates | Competitive, low rates | Varies |

| Customer experience | 24/7 customer service across phone, chat, or Better's AI assistant, Betsy | Limited hours |

How to apply for a HELOC

Once you’ve chosen a lender, submit an application for a HELOC. With Better, you can get your cash estimate in as little as 3 minutes, with no impact for your credit score.

Search for your second home

Start looking for a second home, making sure to apply your HELOC funds toward the down payment, closing costs, or the full purchase price. Once you find a property and make an offer, you’ll finalize the deal and close on your new home.

Start paying your HELOC

During the draw period, you’ll only pay interest on what you borrow. Once the repayment period begins, you’ll pay both principal and interest.

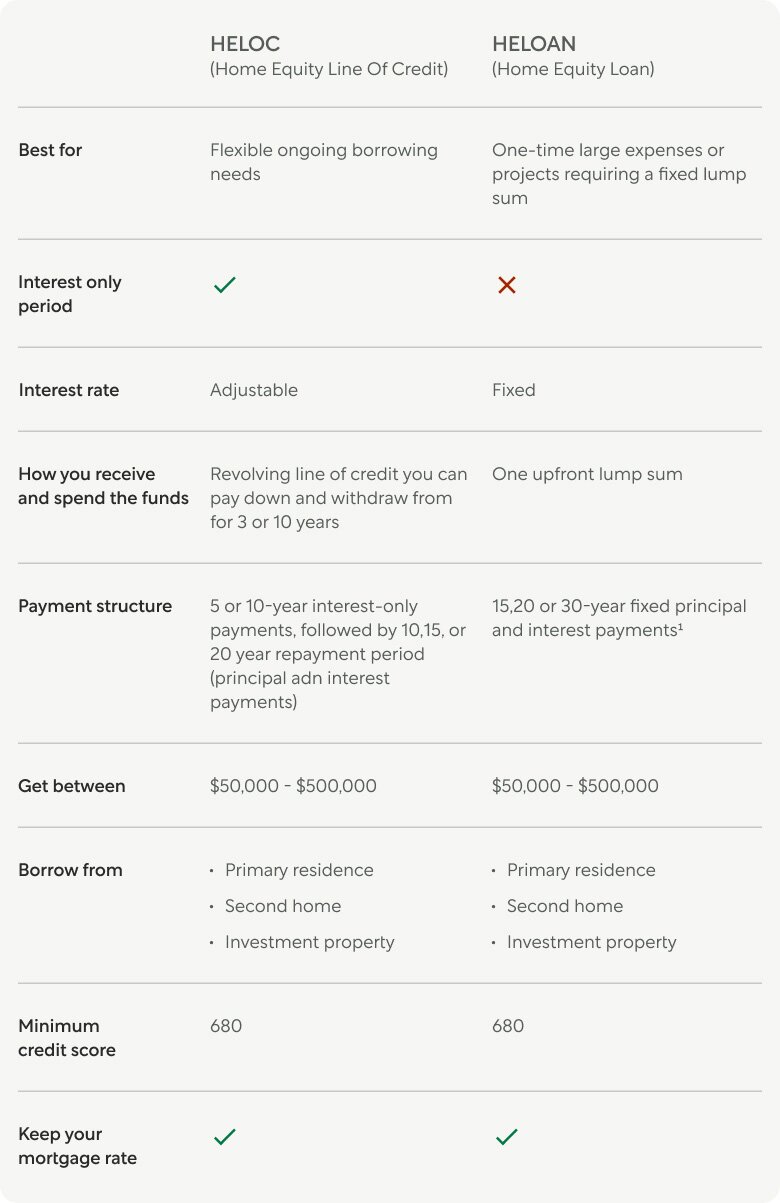

Other loan options for buying a second home

A HELOC isn’t the only financing option available for purchasing a second home. Consider other alternatives, such as a home equity loan or cash-out refinance and compare the costs and terms carefully.

Home equity loan

Like a HELOC, a home equity loan allows you to borrow against your home’s equity. However, a home equity loan provides a lump sum of cash at closing, and you’ll typically pay a fixed interest rate. This predictability can be beneficial, as you’ll know exactly how much you owe each month. However, you’ll start repaying the principal right away.

Cash-out refinance

A cash-out refinance involves refinancing your primary mortgage for more than you owe and taking the difference in cash. While this option may offer a lower interest rate than a HELOC or home equity loan, it resets your mortgage term, which could increase your monthly payments. It’s ideal if current interest rates are lower than your existing mortgage rate.

Personal loan

A personal loan is an unsecured loan that doesn’t require using your home as collateral. While personal loans are easy to qualify for and can provide quick cash, they come with higher interest rates, typically 15% or more.

The bottom line

Using a HELOC to buy a second home can be a smart move for homeowners who have substantial equity in their primary residence, good credit, and steady income. It’s particularly helpful for those who want to finance a second home without refinancing their primary mortgage.

Just be sure to calculate the total cost of financing, including interest, and compare your options carefully, whether you’re considering a home equity loan, cash-out refinance, or HELOC. And don’t hesitate to ask your lender any questions to ensure you fully understand the terms before committing.