If you refinance or sell your home in the average time frame, taking lender credits to offset your closing costs (a.k.a. a no-cost mortgage) will save you money in comparison to paying points.

“Taking credits” refers to the practice of accepting a higher interest rate (and therefore higher monthly payments) in exchange for cash to offset your closing costs. If you take enough credits to offset all closing costs, this results in a “no-cost mortgage.”

The flip side of taking credits is “paying points,” which means paying a percentage of your mortgage balance upfront in exchange for a lower interest rate and lower monthly payments.

The typical cost of changing your rate by 0.125% is 0.625% of your loan amount. So on a $400,000 loan, if you took a rate increase of 0.125%, you would receive $2,500 in credits. If you reduced the rate by 0.125%, you would pay $2,500 in points.

There are many factors that determine whether paying points or taking credits is right for you. However, perhaps the most important one is how long you keep your mortgage without fully repaying it by selling your home or refinancing.

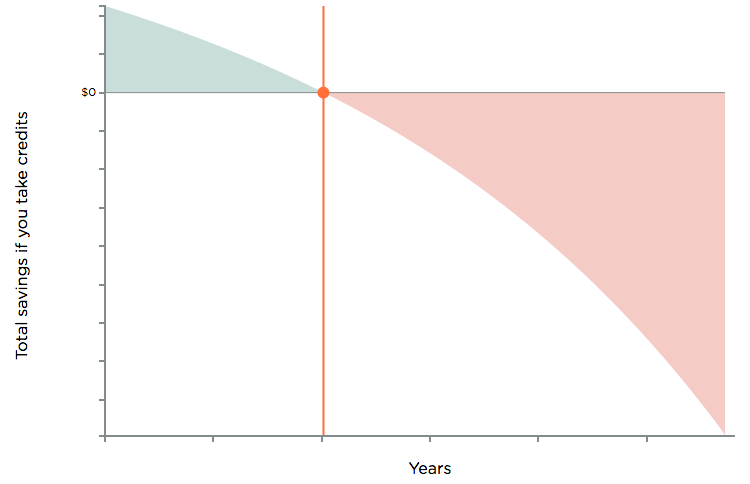

By taking credits, you will save money early on by reducing your closing costs. But there will be a time in the future when you will lose money (compared to paying points) by paying the higher interest rate. The gamble is whether you get out of your mortgage before the time when you break even.

Figure: If you take credits, you will save money early in your mortgage term by offsetting closing costs.

This graph illustrates the concept of taking credits.

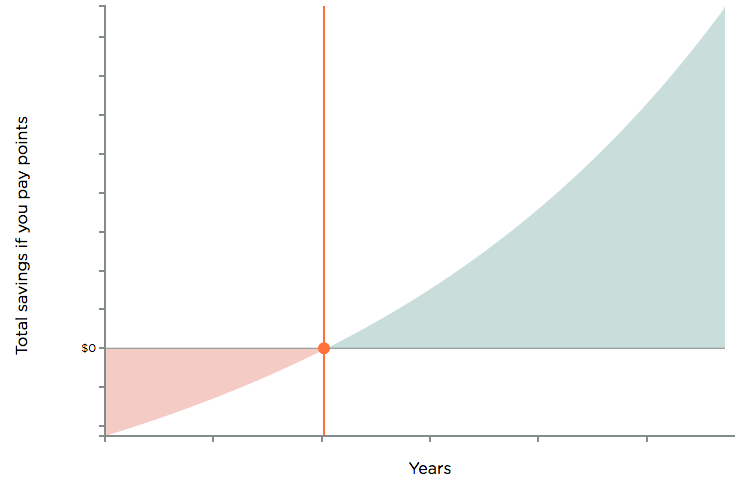

By paying points, you will lose money at the start by paying the closing costs. But there will be a time in the future when you break even and start to save money by paying the lower interest rate. If you leave your mortgage before that time, you lose money. The gamble is whether you will stay in your mortgage long enough to reach the time when you break even.

Figure: If you pay points upfront, you will lose money early in your mortgage term.

This graph illustrates the concept of paying points.

Paying points was the wrong decision for most borrowers

Historical data tells us that for most borrowers in the last 25 years, paying points has been a bad decision. Recent research using data from 1990-2015 found that on average, borrowers have kept their mortgages only five years (Agarwal, Ben-David, and Yao (2016), Journal of Financial Economics).

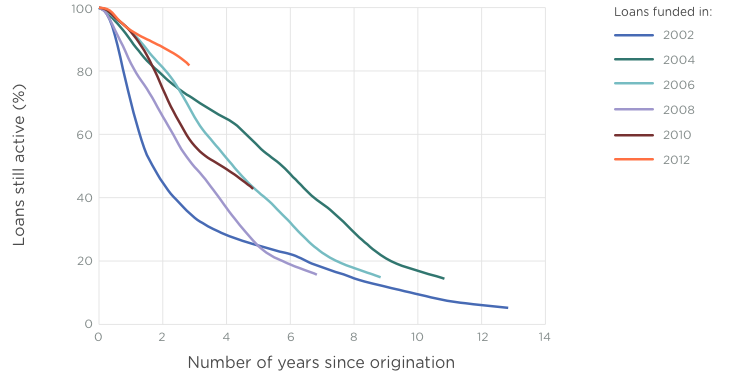

Historical data from Freddie Mac is consistent, showing the majority of borrowers have refinanced, sold, or otherwise closed their mortgage within six years.

Figure: the majority of loans in the Freddie Mac dataset have been active less than six years

Fraction of loans still active out of the cohort originated in any given year. For instance: out of the loans originated in 2008, less than 40% were still active four years later. The other 60+% had refinanced, foreclosed, or sold.

What this means is that those who paid points usually left their mortgages before the break-even line, and therefore lost money. Had they taken credits (or a no-cost mortgage) instead, they would have saved money.

While you might think this finding is due to the time-period studied and interest rate trends over that time, the authors of the research also ran an ex-ante simulation. Given the break-even nature of paying points, those who paid points should have been less mobile on average (e.g., slower terminations for non-rate-based reasons) than those who did not pay points. However, the research concluded that points-payers did not keep their mortgages a statistically different amount of time than non-points-payers.

So, when should you pay for a lower rate?

There are a few scenarios where it does make sense to pay out of pocket for points:

- You think it’s really unlikely that you will move or refinance for a very long time.

- Your projected income is going down in the future, meaning you would not be able to qualify for a similar mortgage.

- Your tax rate this year is much higher than what you expect in future years. You want to deduct as much as possible when your tax rate is high, and points are deductible against income in the year you get the mortgage.

Run your own scenario

In the end, whether to pay points or take credits is a complex question. Things you probably rarely consider (like your future marginal tax rate) affect whether you should pay points or take credits in your particular situation. To make it a bit easier, we’ve provided a calculator that will help you explore different scenarios and make your own determination.1

The projected break-even time will be your guide. If you are considering paying points, you should do so only if you have a high level of certainty that you’ll stay in the mortgage longer than that. You are confident you won’t move, sell your house, pre-pay your mortgage, refinance for a better rate, take cash out for renovations, etc.

If you think any of the above scenarios might happen sooner than that, taking credits is likely a better option.

Get a rate quote

You can get a personalized rate quote from Better Mortgage in minutes, without affecting your credit score.

Every rate quote will provide options for paying points and taking credits, including a no-cost option. Try it and see which option is best for you.

The calculator is provided for demonstrative purposes only. ↩