The first

AI-powered Mortgage

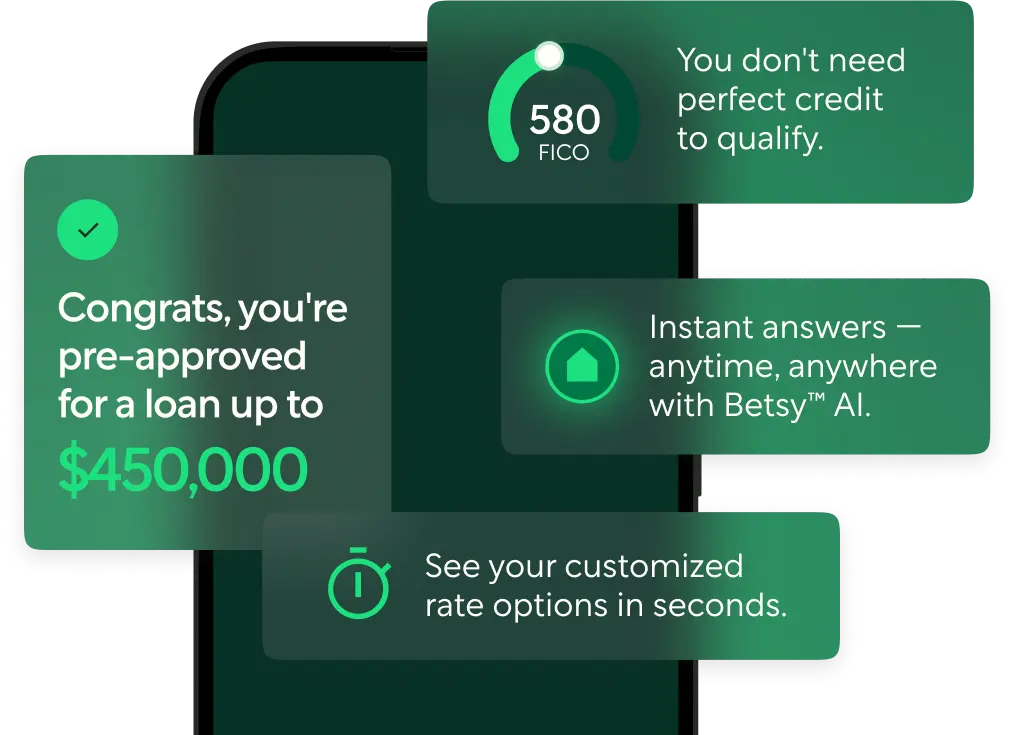

Our tech unlocks lower rates, higher chances of approval,

and a lightning‑fast process from approval to closing. Over $100 billion funded.

Start my pre-approval

3 min| No hard credit check

Got questions?

We've got answers

How AI Mortgage Lending is Transforming the Home Loan Process

One Day Mortgage1

Kick your home loan into hyperdrive. Going from locked rate to Commitment Letter takes weeks for traditional lenders. We do it in a single day. Traditional lenders deliver a Commitment Letter in a few weeks.1

Better HELOC

Introducing One Day HELOC™—your express lane to getting cash from your home with our Home Equity Line of Credit2. Access up to 90% of your home equity as cash in as little as 7 days.3

Insurance